Each year, we send a letter to clients to help guide year-end planning discussions and to offer ideas for them to consider with their other advisors. Our goal in year-end discussions is to ensure that client plans are updated as needed, based on changing external conditions as well as the client’s circumstances, so that we stay on track to deliver the long-term outcomes that each client seeks.

This year, two factors will be important considerations in our year-end planning work: 1) current market dynamics (specifically, ongoing market volatility, low interest rates and a flat yield curve), and 2) the 2017 tax overhaul and our ongoing integration of new tax rules into clients’ long-term plans.

As detailed in prior publications, the 2017 Tax Act changed important aspects of federal income, estate, gift, and generation-skipping transfer (GST) tax law. Many of the provisions that went into effect in 2018 automatically expire (or “sunset”) unless Congress proactively extends them. Because that sunset doesn’t occur until the end of 2025—six years from now—some clients may not feel an urgency to engage in significant planning right now, but there are a variety of planning actions related to the new tax law that merit attention in the near term, and in some cases before the end of the calendar year. While political guesswork plays no part in our planning efforts for clients, we think it is important for clients to understand how their plans may be impacted if the new tax law expires in 2025—or on a more rapid timetable if that law is changed or reversed.

Separately, we note that the past twelve months have been fairly volatile for equity markets. We also experienced a notable drop in interest rates and a meaningful inversion of the yield curve (as of October 31, the curve is not inverted but is still extremely flat—only 0.65% separates the yields of 30-day and 30-year U.S. Treasuries). These conditions present a variety of challenges for investors; more germane to our discussion in this letter, they also present a number of planning opportunities that may require near-term action.

Market conditions may be volatile, but our planning efforts are, as always, focused on stability and consistency. The market activity of the past year may present some near-term strategic planning opportunities, but in most cases, our clients’ long-term financial and estate plans remain on track, so we are looking at these opportunities as incremental steps to supplement plans that are already in place.

You can find our annual planning checklist at the end of this article. In it, we include a variety of actions that clients may want to consider each year; the checklist should be viewed as a starting guide for more tailored conversations between clients and their various advisors. Our primary objective with all of our year-end thinking is to take actions that ensure a firm, stable, long-term foundation for our clients’ plans.

YEAR-END ACTIONS SUGGESTED BY THE 2017 TAX ACT

Non-Taxable Gifts. The 2017 tax overhaul kept in place the gift tax annual exclusion, which is $10,000 indexed for inflation (currently, $15,000) per donor, per beneficiary. Each year’s gift tax annual exclusion expires at the end of that year; therefore clients who wish to use their 2019 exclusion amount should make annual exclusion gifts to all desired beneficiaries before December 31. Some clients may have such gifting on “autopilot,” using outdated exemption amounts, so we recommend that all clients review and update their annual gifting programs regularly.

Similarly excluded from gift tax, though not limited by amount, are direct payments of medical or tuition expenses. In an economy where more of our younger clients are classified as consultants or freelancers, and not “employees” in a legal sense, payment of medical premiums that may be higher than with a traditional employer plan is a meaningful gift. Additionally, such gifts may be an effective risk management strategy for those who may otherwise choose to be uninsured.

Bundling of Charitable Gifts. The 2017 tax act increased the standard deduction for personal income taxes to $24,000 for a married couple filing jointly, while limiting the deduction for state and local taxes (“SALT”) and mortgage interest. For some clients, therefore, the standard deduction now exceeds their itemized deductions for SALT and mortgage interest. In these cases, the clients may not get the full tax benefit from charitable deductions, because their first dollars donated will simply raise their aggregate itemized deductions up to the level of the standard deduction.

Therefore, clients with philanthropic interests may want to consider bunching multiple years’ worth of charitable gifts into a single year, to maximize the charitable deduction during that year and preserve the benefit of the standard deduction in non-gifting years. Family foundations or donor-advised funds at community foundations can be used to control the timing of the actual distribution of the charitable funds to the intended charities. Note that, because a taxpayer’s available charitable deduction is affected by a number of factors, significant charitable gifts should only be made after consultation with a tax advisor.

Opportunity Zone Investments. The tax overhaul authorized the creation of Opportunity Zone funds, which allow for tax-advantaged investments in geographies targeted for economic renewal. “OZ Funds” allow the deferral, and partial avoidance, of capital gains arising out of the sale of appreciated assets. Unlike Section 1031 tax-free exchanges (which are limited to “like-kind” exchanges of investment real estate), OZ funds are available for gains from the sale of any investment, including publicly-traded securities.

Accordingly, clients who incurred substantial capital gains in 2019 can consider whether an OZ investment is an effective way of minimizing their tax liability. Moreover, if a client has the ability to control the timing of gain recognition, and intends to roll the gain into an OZ investment, it may be advisable to recognize the gain, and make the OZ investment, in 2019 rather than 2020, in order to obtain the maximum tax benefit. The OZ legislation provides a 10% reduction in gain (through a basis adjustment process) for OZ investments held for at least five years, with an additional 5% reduction for investments held for seven years, but that benefit expires at the end of 2026. Accordingly, 2019 (which is seven years ahead of 2026) is the last tax year in which an OZ investment may qualify for the full 15% gain reduction.

Our approach to investing in Opportunity Zones focuses first on the merits of the underlying investment, both in terms of its financial prospects as well as its potential impact on the surrounding community. We believe proper due diligence is especially important for OZ funds given the illiquid nature of these investments. While tax benefits can help enhance returns, they will not make a good investment out of a poor one.

Expanded Estate Tax Exemptions. The 2017 Act doubled the size of the federal gift, estate, and GST tax exemptions, from $5 million to $10 million per person, indexed for inflation (currently, $11.4 million). However, the exemption reverts to its 2017 amount at the end of 2025, and there is a risk that a future Congress could reverse the law sooner. Clients, therefore, should not assume they have six more years to act, and those with substantial taxable estates may want to consider using the increased exemption by making gifts now, or at least begin the planning for such gifts.

In particular, it may be prudent to consider implementation during this year of certain complex gifting techniques that involve multiple transactions. In certain cases, the IRS may try to apply the “step transaction doctrine” and treat those several transactions as one concerted strategy, which may have the effect of negating the desired tax benefits. To avoid this problem, it may be advisable to put certain structures in place now, well in advance of a contemplated gift, and to separate subsequent planning steps into later tax years, so there are several years of breathing room between the initiation activities and the envisioned follow-up activities:

| NOW | LATER |

|---|---|

| Intra-spousal transfer, to provide one spouse with sufficient assets to fund… | …a Spousal Lifetime Access Trust (SLAT) for the benefit of the other spouse and the couple’s descendants |

| Creation, capitalization and operation of a family business entity (e.g., a family limited partnership or family limited liability company) | Intra-family gifts of ownership interests in those entities |

| Funding of generation-skipping dynasty trusts with seed gifts | Planned installment sales of family assets to those trusts |

| Upstream gifts to older family members with available estate/gift/GST exemptions | Creation of trusts by the older family members, to benefit younger generations |

YEAR-END ACTIONS SUGGESTED BY THIS YEAR’S MARKET CONDITIONS

General steps to maximize the utility of gains and losses: While the market has experienced notable volatility over the past year, it is at or near its all-time high. Clients can consider taking advantage of appreciated positions to raise cash opportunistically in the near-term to meet their projected cash needs for the next year or so. Additionally, pre-funding several years’ worth of charitable gifts now, using appreciated securities, can provide a hedge against the risk of future market reverses.

Market volatility may also have moved portfolio holdings of certain asset classes outside of desired ranges, which may require the trimming of appreciated positions. To ensure this rebalancing is done in as tax-efficient a manner as possible, clients should simultaneously look for opportunities to harvest tax losses to offset gains.

Trust-related strategies that benefit from volatility: If the price of a security declines meaningfully, but the client nonetheless views it as a good long-term investment, a grantor retained annuity trust (GRAT) or a charitable lead annuity trust (CLAT) could be used to transfer future appreciation of that investment to beneficiaries free of gift tax. Interest rates are currently low, which positively impacts the valuation of GRATs and CLATs and therefore creates a favorable environment for these strategies.

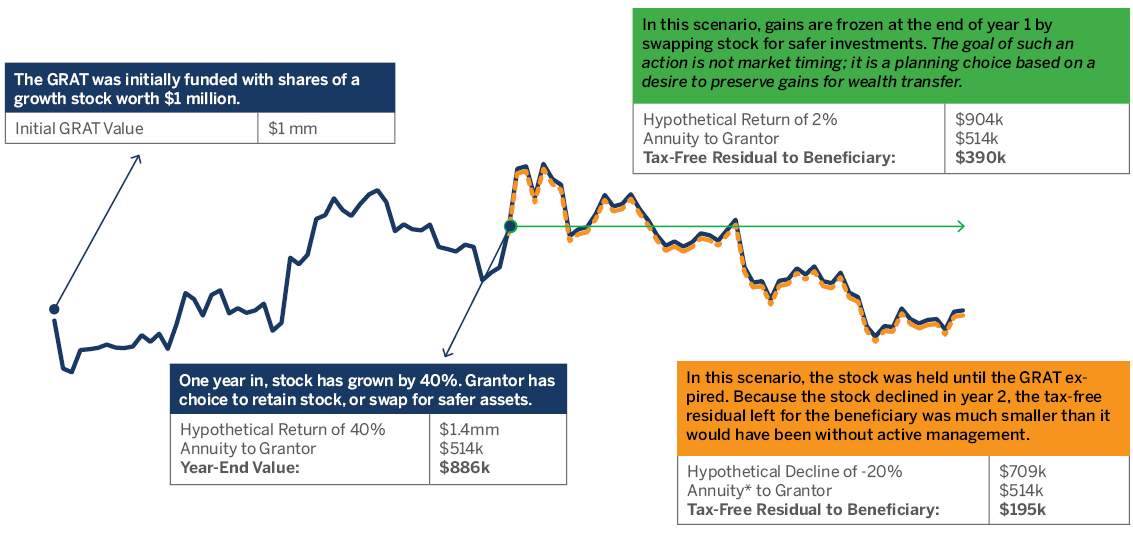

For those who have already implemented a GRAT strategy, now is a good time to evaluate steps to reduce volatility inside of the GRAT and “lock in” an implied gift. Volatility can be reduced by changing the investments that have appreciated inside the trust, by selling the assets, exchanging the assets with others from outside the trust or purchasing the assets from the trust for a promissory note. The illustration below demonstrates the potential benefit of actively managing a GRAT.

GRATs: A USEFUL OPTION IN VOLATILE MARKETS

GRATs can be powerful tools in a wealth transfer plan, and active management of a GRAT can add additional value. The illustration below shows how a two-year GRAT funded at the end of 2016 with a hypothetical growth stock (depicted in the background below for illustrative purposes only) could have locked in gains earned in 2017 by swapping out its growth assets for safer investments. Alternatively, if the growth stock had instead declined during the first year, the grantor could have simply terminated the GRAT early and created a new one.

Source: Brown Advisory calculations. *Annual required annuity payment based on principal plus an IRS-required rate of return based on interest rates at the time of trust creation (the “7520 rate”). The December 2016 7520 rate of 1.8% was used for this illustration. All figures, including the price trend of the underlying assets, are entirely hypothetical and provided for illustrative purposes only.

Taking advantage of current interest rates: Market uncertainty is reflected in the flattened and inverted yield curve we have seen this year. Long-term rates have been lower than short-term rates for a good portion of 2019, and this development is reflected in the applicable federal rates (AFRs) that govern the minimum interest rates required for intra-family loans and other transactions. Given that the long-term AFR is barely above the short-term AFR at present (1.94% vs. 1.68%, per the rates prescribed by the IRS for November 2019), clients have an opportunity now to lock in low rates for decades under certain strategies, including promissory notes from intra-family loans or installment sales of assets to a “grantor trust” for the benefit of younger family members. Where such debt obligations already exist from prior transactions, clients should consider whether the debt may be refinanced at lower rates for a longer term. These strategies may allow senior generations to lend growth capital to future generations, while essentially creating a fixed income asset in their own estate, so that the benefit of future asset appreciation accrues primarily to younger family members.

ADDITIONAL TOPICS FOR CONSIDERATION

Our focus in this letter has been on planning actions suggested by new tax laws or recent market volatility, but there are many other topics we intend to address with clients as the year draws to a close. Examples of these include spend-rate planning (relevant for all clients, and especially for certain endowments and foundations whose operations are funded by their portfolios), sustainable or mission-aligned investing, or cross-border planning for expatriate clients (or clients considering an extended residency in another country). None of these issues has a specific calendar-year deadline, but in each case, the actions and decisions that clients make now may have a lasting impact on long-term results.

CONCLUSION

It is important to evaluate near- and long- term planning options annually—each year can bring different opportunities. Excluding any changes in specific client circumstances, we believe our long-term financial and estate plans for clients remain secure, so the solutions we have discussed for opportunistic planning in 2019 focus on near-term market volatility, low interest rates and changes to the tax laws that are not permanent.

We want to counsel clients and their families to avoid letting near-term stability in tax laws lull them into inaction. Where it makes sense, clients should take advantage of market volatility and lower long-term applicable federal rates to advance important estate-planning and philanthropic goals. Foundations and endowments can similarly take advantage of the strong markets of the past few years to review distribution spend rates and consider broader changes in portfolio investment policies.

Finally, we advise clients to consider all of the ideas in this letter in the context of lifetime or multigenerational goals already being pursued on an ongoing basis. As we have said in prior letters, just because you can do something does not mean you should do something. Each planning option we discuss with clients at year’s end offers benefits and tradeoffs, and the overriding factor in moving forward on any of them should be whether they help increase the probability of achieving the client’s ultimate aims. ![]()

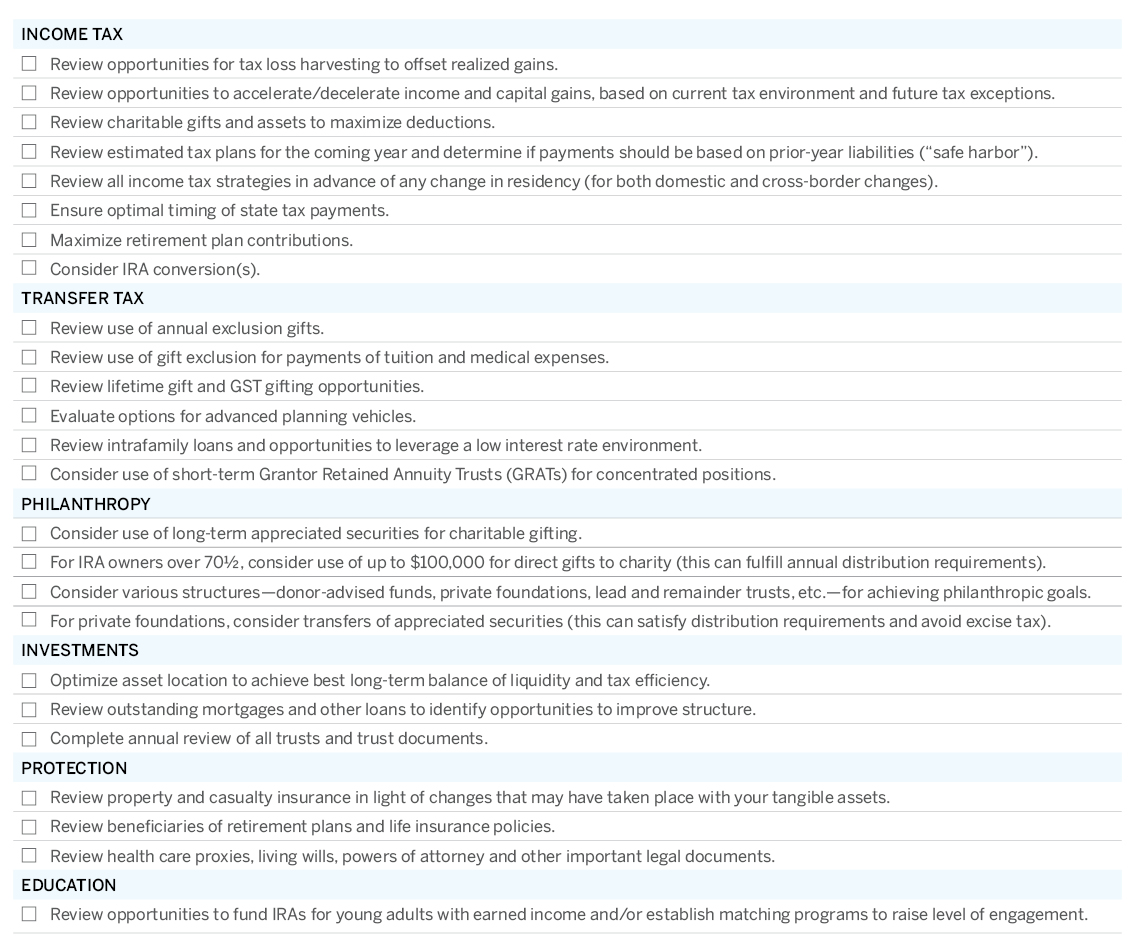

Annual Planning Checklist

The views expressed are those of Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested.

The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

Any accounting, business or tax advice contained in this communication, including attachments and enclosures, is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.