When putting a plan in place, we believe it is critical for any mission-driven organization to develop an effective, long-term asset allocation strategy to manage its endowment assets. Given an institution’s long-term return objectives and risk tolerance, the Investment Committee (IC) should partner with its investment advisor to define an asset allocation approach that creates the greatest likelihood of achieving its financial goals. Beyond optimizing returns, a thoughtful asset allocation helps to provide a long-term road map to endure periods of market stress and rebalance during periods of market outperformance.

One of the perennial challenges for investors is the uncertainty caused by a host of contributors—from geopolitical factors to economic transitions to the intermittent fragility of market fundamentals. Addressing market uncertainty requires patience, balance and discipline, all of which we believe are best expressed through a long-term strategic asset allocation.

A MULTISTEP CLIENT-CENTRIC PROCESS

We believe that the first step in designing a long-term strategic asset allocation should always be taking the time to understand a client’s return objectives, risk tolerances and liquidity preferences. Helping an IC build consensus around these topics is necessary to frame the discussion around what long-term asset allocation is most appropriate for the organization. We also document those objectives and preferences in an investment policy statement (IPS) because they represent the cornerstones of an organization’s investment strategy.

Step two is developing capital market assumptions against which to model portfolios with different mixes of asset classes. We then collaborate with the client to clearly detail the trade-offs involved in taking various approaches to long-term allocations, focusing on factors like the use of alternative investments, drawdown risk and illiquidity risk.

In our experience, long-term asset allocations are optimally defined through asset class ranges rather than simple targets (e.g., 70–90% vs. 80%). The range-based approach acknowledges the uncertainty inherent with investing and provides greater flexibility to adjust the portfolio for changing market conditions. Ideally, the long-term asset allocation ranges should not change very much from year to year, but where exactly the allocation falls within each range may be adjusted to reflect different opportunities in the market.

Third, and to build a customized asset allocation for an organization, we also want to make sure to incorporate its preferences for sustainability and other environmental, social and governance (ESG) and diversity, equity and inclusion (DEI) mandates that embody its mission and values. We also work closely with the IC to manage other organizational restrictions, such as debt covenants, when necessary.

Finally, we document the agreed-upon long-term strategic asset allocation in the organization’s IPS. A well-crafted and comprehensive IPS enables both the advisor and client to programmatically revisit goals, objectives and risk tolerances, and to remove as much emotion as possible from the investment decision-making process.

RISK AND RETURN

The two critical considerations to weigh in crafting a long-term strategic asset allocation are the return potential of a given investment (or mix of investments) and the risk taken to achieve that return. Given that the typical nonprofit institution needs to generate an annualized return that meets or exceeds its spending rate and that its operating needs are sensitive to inflation, the investment portfolio must generate a real return in excess of spending to ensure the purchasing power of the corpus grows through perpetuity. By contrast, the risk tolerance of an organization is more variable and will depend entirely upon its unique needs and preferences.

LOOKING THROUGH THREE LENSES TO EVALUATE RISK

At Brown Advisory, we view risk through three lenses: insufficient long-term growth, drawdown in market value and illiquidity.

The problem of insufficient growth is simply stated: If a portfolio’s asset allocation is not designed to generate a return in excess of spending over the long term, its value will shrink over the long term.

We believe drawdowns, however, are the most serious medium-term risk for many nonprofit investors. Drawdowns can be highly unpredictable—there is really no way to know when they will occur, how long they will last or by how much values will decline. A significant drawdown to a portfolio can be devastating to its performance. The key is to avoid becoming a forced seller during any market environment. By staying invested, assets have time to recover in value following a market decline. Protecting against drawdowns requires a diversified approach to asset allocation to ensure sufficient investment in asset classes with the potential to hold or even rise in value when equity markets decline.

Allocating capital to illiquid strategies (i.e., those that cannot be easily turned to cash or redeemed) can enhance returns over the long term, but illiquid exposure always entails risk. We work closely with clients to understand their illiquidity tolerance, and we provide supporting analysis to explain the trade-offs involved in allocating capital to illiquid asset classes. In our experience, many clients seek more liquidity than they will require, which can lead to decisions that decrease long-term returns. At the same time, understanding how the portfolio behaves during different market conditions, and how much the percentage of assets locked up in illiquid managers may increase when public markets decline, is essential to managing portfolio liquidity. We conduct scenario analyses to model and understand portfolio liquidity during periods of public market stress.

MODELING AS A TOOL

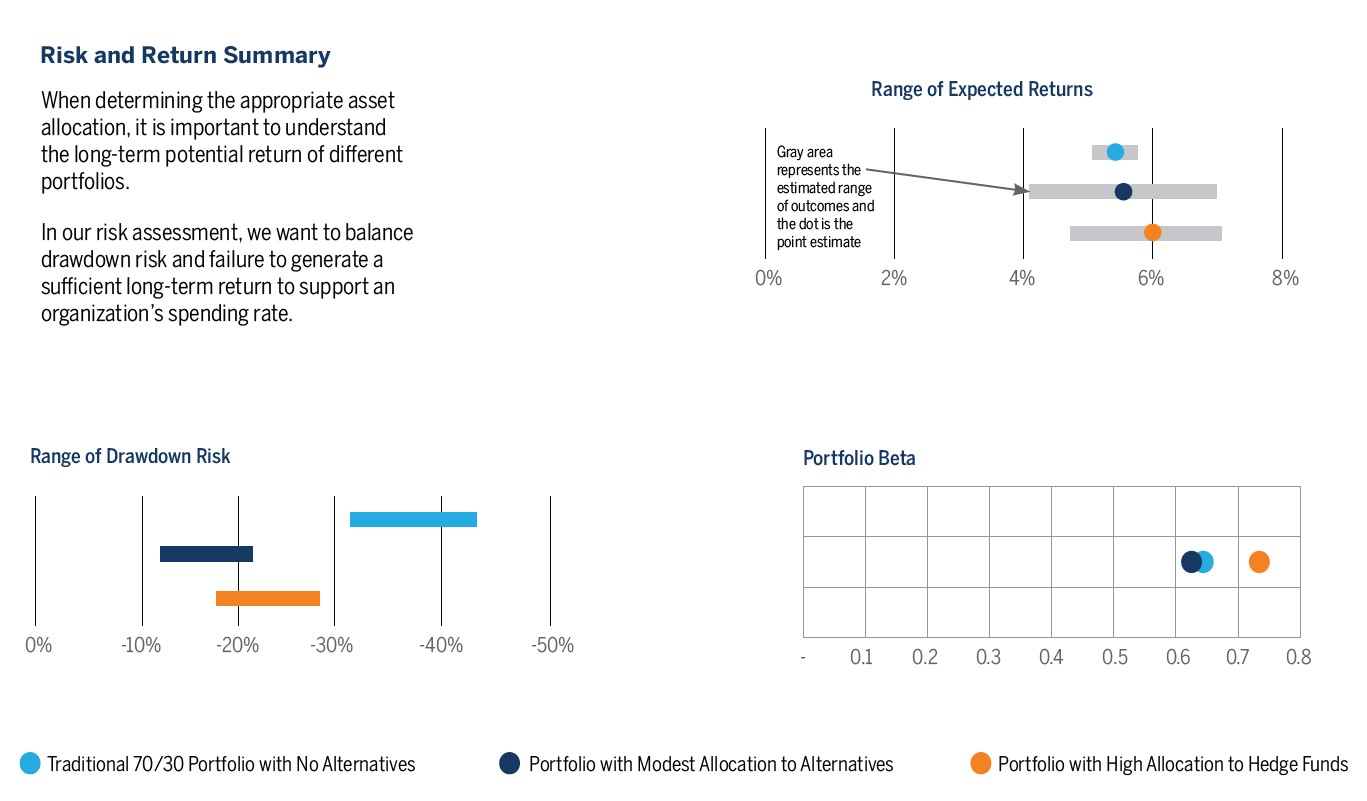

Beyond market stress analysis, we also model each client’s portfolio for its return potential, volatility and drawdown risks on the basis of capital market assumptions. We recognize that our assumptions and data will not be perfect, and we acknowledge that investing is often more art than science. For this reason, we do not take a prescriptive approach to asset allocation modeling and portfolio optimization, as some advisors do. Rather than relying solely on the model’s output to determine a client’s asset allocation, we view the model as a tool that produces potential outcomes to evaluate and interpret based on experience and on each client’s specific circumstances.

The charts below help to illustrate the output that our modeling process generates. Given the uncertainty in forecasting future performance, we present ranges for return potential and drawdown risk when evaluating different asset allocation strategies. This helps to facilitate a discussion with clients and allows us to explain key trade-offs when considering different mixes of asset classes.

Source: Brown Advisory Analysis. The information provided above illustrates hypothetical portfolios that are not necessarily representative of any current portfolios and are for illustrative purposes only. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy. Asset allocations could change depending on risk tolerance, investment objective and assets available for investment. Alternative investments may be available for qualified purchasers and accredited investors only.

IDENTIFYING THE RIGHT STRATEGIC MIX OF ASSET CLASSES

In building a portfolio, finding the right strategic mix of asset classes provides the foundation for balancing the portfolio’s risk and return over the long term. In order to determine the appropriate strategic mix, we prefer to be guided more by bottom-up considerations about each asset class than by top-down macroeconomic views, factors or concerns. We examine three key characteristics for every asset class:

- The asset class’s estimated long-term baseline return expectation: Capital market assumptions are developed by evaluating historical returns through our view of the current market conditions.

- Its potential drawdown risk: Some asset classes are more volatile than others—while upside volatility can drive outperformance, understanding and managing downside volatility are essential to preserving value.

- Its alpha opportunity: The extent to which adept management within the asset class can improve risk-adjusted returns.

We combine this asset class analysis with a fundamental view of a given investment’s price relative to its inherent value and risks to establish a long-term baseline return. This investment-specific analysis is essential to our asset allocation work and of particular import when examining alternative options, such as private equity, venture capital, real estate and hedge funds, where managers can add considerable value through highly differentiated strategies.

We believe it is essential to bear in mind that alpha opportunity is never consistent across asset classes because some markets are more efficient than others. For example, large-cap U.S. equity tends to be highly efficient, making it difficult for even the most effective managers to generate excess return. By comparison, emerging markets and small-cap equities tend to be less efficient markets, allowing skilled managers to outperform their index and generate alpha.

After determining the strategic asset class mix that is right for a client, we select investment managers who can support their return objectives while adhering to the client’s risk tolerance and liquidity guidelines. We believe that with intense research, we can do a good job of separating exceptional managers from mediocre managers. In selecting managers, we are always mindful that the alpha opportunity (and consequently the range of returns) is greater for private investments (private, equity, venture capital, real estate, etc.) and hedge funds. Simply allocating capital to these alternative asset classes, however, does not guarantee success. Manager selection across alternatives is essential—partnering with the right managers is often the difference between success and failure.

Finally, we integrate our asset allocation and manager selection research, which helps us extract valuable information from our managers and target our client’s capital effectively.

BALANCING TACTICAL AND STRATEGIC GOALS

In practice, many of the portfolios we manage may differ from the long-term targets identified in the IPS. For example, we take a disciplined approach to investing in private markets and may not reach a targeted asset allocation range in private markets for five years or more. While we slowly build toward ranges in a client IPS, we will often invest capital in similar, liquid investment offering, so we might take capital that will eventually be called by venture capital managers and invest it in segments of the public equity market that approximate a venture fund’s risk/return profile.

At times, we may also tilt portfolios away from long-term targets to take advantage of market dislocations or mispricings. Such tactical shifts reflect a one- to five-year outlook based on scenario analysis, which helps us identify asymmetric risk/reward opportunities.

We tend to make gradual and incremental shifts in our portfolios, since we know that even the best investors are only right slightly more often than they are wrong. We manage portfolios in a balanced approach, and we study our results, improve our processes and seek to make better decisions every year. Above all else, we recognize that designing a strategic asset allocation is not a static exercise. It is an ongoing process that requires patience, balance and discipline.

BROWN ADVISORY CAN HELP

We have decades of experience serving many different types of nonprofits, including educational endowments, private foundations, hospital systems and cultural organizations, in a highly collaborative way. These range from local organizations with portfolios valued at $5 million to national organizations with more than $2 billion in investments.

We strive to foster a culture that results in low team turnover and seeks to serve every aspect of your long-term strategy. We customize our services to each client, providing a “bespoke” experience tailored to your evolving needs, and we strive to learn from every client as we help navigate the evolving investment landscape. And when an organization experiences turnover in board membership, especially in its IC or among key staff members, we are there to serve as your vault of institutional knowledge. ![]()

The views expressed are those of Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested.

The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

Alternative investments may be available for qualified purchasers and accredited investors only. Certain strategies intend to invest in companies with measurable ESG outcomes, as determined by Brown Advisory, and seek to screen out particular companies and industries. Brown Advisory relies on third parties to provide data and screening tools. There is no assurance that this information will be accurate or complete or that it will properly exclude all applicable securities. Investments selected using these tools may perform differently than as forecasted due to the factors incorporated into the screening process, changes from historical trends, and issues in the construction and implementation of the screens (including, but not limited to, software issues and other technological issues). There is no guarantee that Brown Advisory’s use of these tools will result in effective investment decisions.

ESG considerations are one of multiple informational inputs into the investment process, alongside data on traditional financial factors, and so are not the sole driver of decision-making. ESG analysis may not be performed for every holding in the strategy.