Folks, time has not been kind to my mid-section. Whether due to slowing metabolism, a weakness for office snacks or my genetic makeup, I’m currently among the 40+% of American adults who are considered obese. Despite attempting low-carb diets, intermittent fasting and increased exercise I have struggled to maintain a healthy weight.

I’m well-read enough to know that the health complications associated with obesity, particularly as one ages are not good. More than 80% of Type 2 diabetes cases can be attributed to obesity. There are heightened cardiovascular and cancer-related risks as well. Thus, consider my excitement at the prospect of a wonder drug that could help me lose 25% of my body weight!

I’m referring to the latest class of glucagon-like peptide drugs (GLP-1s) that were designed to allow diabetics to absorb glucose after a meal. However, more recently, these drugs – specifically Wegovy/Ozempic (Novo Nordisk - NVO) and Mounjaro (Eli Lilly - LLY) have demonstrated other substantial and favorable benefits, including material weight loss and a reduction in major adverse cardiovascular events.

While these drugs are rarely covered by insurance for weight loss today – and some, like Mounjaro are not yet FDA approved for weight loss (they are used off-label) - the advantages of lowering the risk of heart attack and stroke suggest it may only be a matter of time before payers are unable to deny coverage. That would bring the $1,000/month cost today down to a more palatable level for potentially the 70% of American adults who are either obese or overweight. Peak industry revenue projections for GLP-1s have climbed upwards of $100 billion; in 2022, GLP-1 revenue was just a fraction of that amount.

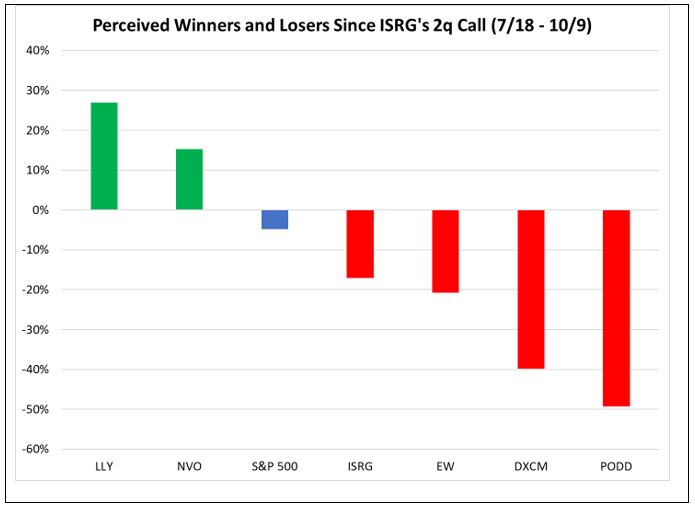

This explains why LLY and NVO have nearly doubled over the past year in a sector that’s seen muted performance over the same time horizon. The perceived winners of the proliferation of GLP-1s have been few and far between relative to the perceived losers. On July 18, robotic surgery leader Intuitive Surgical (ISRG) sent a warning shot to investors that it was starting to see a slowing rate of growth for bariatric surgeries due to increased use of GLP-1s. While bariatric surgery only accounts for 4% of company procedures, ISRG is down more than 15% since its earnings call. LLY is up more than 25% since then; NVO is up 15%.

Source: FactSet. Data as 10/9/2023. Please see the end of this report for company names and important disclosures.

ISRG isn’t alone in being perceived as a victim of LLY and NVO’s success. Dexcom (DXCM) – a leader in continuous glucose monitoring (CGM) systems has seen 40% of its market value evaporate in less than three months on concerns that a thinner future population would be less at risk for Type 2 diabetes, and thus its total addressable market (TAM) will shrink. Similarly, Insulet (PODD), a leader in insulin pump therapy, is down nearly 50% on heightened concerns of a smaller TAM. ResMed (RMD), which makes CPAP machines for sleep apnea, has lost more than a third of its value in recent months. Edwards Lifesciences (EW), a leader in aortic, mitral and tricuspid heart valve replacement has declined more than 20% – despite stating that valve stenosis is an age-related disease, not obesity-related.

Many companies have in fact tried to defend themselves; Dexcom recently presented a study by United Healthcare showing that CGM systems have been complementary to GLP-1s to date, with CGM attachment rates in the GLP-1 patient base increasing – even for those patients not on insulin. PODD stated that while GLP-1s are effective at glucose control, they haven’t demonstrated the ability to reverse the natural progression of diabetes itself for Type 2 patients – a population that has been completely written off as a potential growth opportunity for PODD according to our team’s analysis. Our conversations with endocrinologists support the view that Type 2 patients should not be uniformly removed from PODD’s TAM. Like so many aspects of this phenomenon, it is much more nuanced than the market’s knee-jerk interpretation.

Our equity strategies have been closely evaluating some of the perceived losers in recent weeks and months, given the market’s extreme extrapolation of early data points. It will likely take time for any of these companies to disprove the current sentiment of a shrinking TAM, while according to our health care analysts, most investors remain very short-term oriented. We can use this temporal differentiation to our advantage, although considerable uncertainty remains surrounding the eventual use and impact of these drugs not just on the health care sector, but the broader economy. Here are just a few creative second or third derivative factors to consider:

- Medical device/hospitals: a less obese population may experience fewer joint replacements. That said, the population may become more active, which in turn may counterintuitively increase the TAM for sports-related surgeries.

- Clothing/retail: a GLP-1 saturated population may need to purchase an entire new wardrobe of clothing, reaccelerating growth for some apparel companies.

- Online dating: single people may be more likely to take their new wardrobes and waistlines to sites like Tinder or Hinge (as MTCH shareholders, this would be a welcome benefit).

- Airlines: fuel accounts for nearly a quarter of airline operating expenses. Imagine what a 25% reduction in average body weight for 40+% of the customer base would do for profit margins?

- Restaurants: With muted appetites, will this portion of the population meaningfully cut back on dining experiences? Even Pepsi was asked about the impact of GLPs on its earnings call on October 10th (impact thus far is negligible).

In conclusion, our take on this breakthrough pharmaceutical innovation is that it is way too early to draw conclusions on the direct and indirect consequences of the proliferation of GLP-1s. Where the market seemingly draws definitive conclusions from very early-stage information, we will attempt to invest opportunistically in the other direction, doing so with a tremendous amount of humility for what is still to be learned.

Thanks for reading, and remember to never skip a Beat - Eric

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

Factset® is a registered trademark of Factset Research Systems, Inc

Global Industry Classification Standard (GICS) and “GICS” are service makers/trademarks of MSCI and Standard & Poor’s.

Figures shown on sector diversification and quarterly attribution by detail slides may not total due to rounding.

Terms and Definitions:

Listed stocks:

Novo Nordisk (NVO), Eli Lilly (LLY), Intuitive Surgical, Inc. (ISRG), Edwards Lifesciences Corp. (EW), DexCom, Inc. (DXCM), Insulet Corporation (PODD), ResMed, Inc. (RMD). Match Group Inc. (MTCH), PepsiCo, Inc., (Pep)