Despite making new highs recently, U.S. equities were volatile over the summer and early fall, keeping investors guessing about the future direction of prices. Among the concerns breeding skepticism about the economy and the markets are on-again/off-again trade negotiations, disruption of supply chains, declines in manufacturing activity, and sluggish capital spending. On the other hand, based on the normal relationship of earnings multiples to interest rates, stocks are meaningfully undervalued relative to bonds and appear to be one of the few asset classes offering the prospect of inflation-beating returns.

As long-term investors, we aren’t overly concerned with market gyrations or the path of stock prices over the next few months. We’ve consistently reminded clients to keep enough cash and equivalents on hand so they won’t be forced to liquidate investments at inopportune times, should the markets pull back.

The more important issue, in our view, is whether recent signs point to some sort of structural change in the U.S. economy that may restrain the country's ability to grow at rates considered normal over the last several decades. In a word, is the United States at risk of “Japanification?” This term refers to the possibility that the U.S. could fall victim to long-term economic stagnation, similar to the fate that befell Japan starting in the 1990s. And is there enough concern over such a prospect to seriously undermine investor confidence?

THE “JAPANIFICATION” QUESTION

Investors who were active in the late 1980s will recall that asset prices in Japan reached extreme levels as money poured into the country from all over the world, propelled by extraordinary economic growth. Japan’s GDP had grown by an average of more than 5% per year from 1950 to 1989—a true post-War economic miracle. But as often is the case, the boom turned into a financial market bubble and the price/earnings ratio of the NRI 350 Index (a broad index of non-financial stocks) at the end of 1989 was over 50x, compared to the S&P 500® Industrial Index at 15x. One estimate of the value of the land under Tokyo’s Imperial Palace (a bit over three sq. km.) suggested that it was worth more than the entire state of California!

Much of Japan’s growth was driven by a rapid rise in bank debt, encouraged by loose-money policies at the Bank of Japan (BOJ, the country’s central bank). Once the bubble in asset prices started to burst, the leverage that had for years fueled growth then worked in reverse, quickly deflating prices. Rather than allow weak companies and institutions to fail, the banks kept them alive by injecting funds, but many (referred to as “zombie companies”) were virtually unable to function without bailouts. Having traditionally run surpluses, the government attempted to stimulate the economy by incurring large deficits, in part to help fund interest costs on the growing debt load. At the same time, slow population growth impacted the Japanese labor force as retirees started to outnumber new entrants. Japan’s economy has never really recovered, weighed down as it is by debt, an aging population and uncompetitive zombie companies. As a result, Japan’s GDP growth has averaged less than 1% over the last 30 years while wages have stagnated.

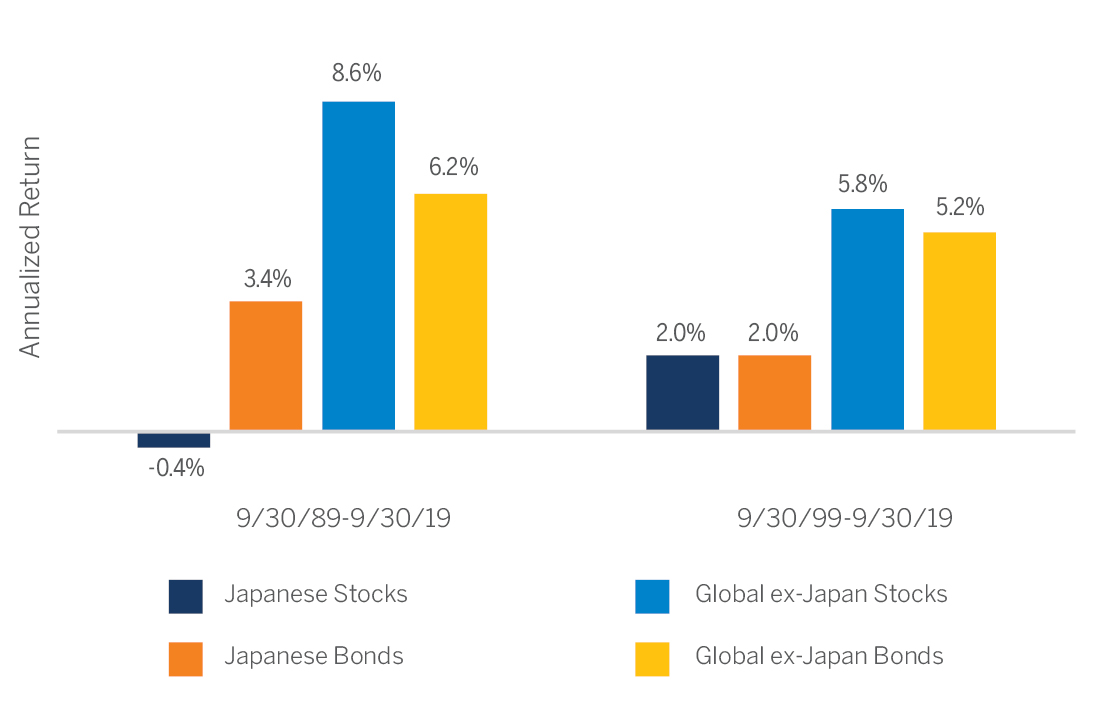

The impact on investors has been significant: In recent decades, Japanese equity and fixed income returns have dramatically trailed behind the rest of the world (see chart below). Therefore, Japanese investors generally have been unable to maintain even modest spend rates from their portfolios unless they were heavily invested outside the country or willing to spend down capital.

If this story sounds vaguely familiar, it could be that you’re reading newspaper accounts citing the parallels with America’s current situation. Among these are:

- Steady increases in the national debt. As a percentage of GDP, U.S. government debt is nearly 110%, compared to 82% ten years ago and 32% in 1981 (its modern-day low point). Today, Japan’s national debt is about 250% of GDP—easily the highest in the developed world.

- Low interest rates. Like Japan starting in the mid-1990s, the U.S. has maintained rates at historically low levels since the financial crisis of 2007-08, yet inflationary pressures remain at bay. The BOJ has been targeting rates at zero since 2016, in line with much of the developed world, but with little effect on demand.

- Aging population. Because of low fertility rates, greater longevity, and little to no immigration, Japan’s population is aging and is, in fact, projected to decline for at least the next 50 years. The U.S. population is not as old (16% over 65 years of age vs. Japan’s 28%, according to the Statistics Bureau of Japan) but it is aging, and fertility rates are low. The U.S. Census Bureau estimates that population growth in 2018 (0.6%) was the lowest since the 1930s.

CRUMBLING FOUNDATION

Japan’s slow GDP growth in recent decades has greatly dampened its market returns relative to the rest of the world.

Source: Bloomberg. Please see disclosure at the end of the article for a complete list of indexes and definitions used to represent Japanese and global asset classes in this chart.

While there may be similarities between Japan’s historical experience and the current situation in the U.S., there are also notable differences of degree. America’s national debt is much lower, its interest rates and inflation rates higher, and its population younger and not contracting. In terms of debt and interest rates, today’s levels in the U.S. are similar to Japan’s 20 years ago, but by then deflation had already set into the Japanese economy and growth was slowing, as we’ve said. As important, however, is the contrast in how the two countries have dealt with financial or economic crises. In retrospect, Japan failed to recognize the bad debt of its corporations (or allow them to go out of business), it was hesitant to fix its banks, and it did little to prevent asset prices from declining as the bubble burst. Using the financial crisis as a case in point, the U.S. response was swift and decisive. Bad debt was written off, the banks were saved and strengthened, and asset prices began to recover relatively quickly. In addition, the implementation of quantitative easing (in which the Federal Reserve bought up large amounts of U.S. Treasuries and certain other debt securities) proved to be an effective policy response. In the end, deflation in the U.S. was prevented.

WHERE THE U.S. GOES FROM HERE

Still, inflation remains low and economic growth is sluggish in the face of the Fed’s easy-money policy and the administration’s efforts to stimulate demand. The question that many investors are asking is whether there is sufficient “room” for the U.S. to respond effectively to the onset of a recession or, worse, to some sort of crisis.

From a fiscal perspective, the options would indeed seem limited, as the U.S. federal deficit is already over $1 trillion. While Congress has shown little inclination to control spending, there could be pushback to a deficit increase large enough to provide added stimulus. It’s also unclear whether political consensus could be reached on this score.

Monetary policy seems a more likely response. The current federal funds rate target of 1.50-1.75% admittedly doesn’t allow for rates to be lowered dramatically for purposes of demand stimulation, but compared to other developed nations, the U.S. has greater running room. (One has to wonder how countries with negative interest rates such as Japan and Germany will deal with recessionary pressures.) Further, the U.S. could again turn to quantitative easing practices. By purchasing debt securities of various maturities, the Fed could effectively cap interest rates along the spectrum of maturities while injecting meaningful amounts of cash into the money supply. This strategy worked during the last crisis and it would likely have a positive effect again. At the same time, the Fed’s balance sheet is still swollen by securities purchased during the Great Recession, so it’s not clear how much its capacity can be expanded.

In the end, economic growth and rising stock prices are largely a function of confidence. If consumers and business professionals feel good about the future, they buy more products and services and invest more aggressively in capital equipment. Inflation, too, results from higher levels of confidence, as demand tends to outstrip supply in a world where optimism prevails. To an extent, today’s low inflation and interest rates may reflect a general lack of confidence, or at least (to borrow a phrase from John Maynard Keynes) subdued “animal spirits.”

Investors can gain or lose confidence in many things, but it seems to us that three are particularly relevant in the current context:

- The economy’s ability to grow over time.

- The willingness and ability of government and other institutions to counteract the effects of recession or an economic shock

- Leadership of governmental institutions and corporations

Measuring the level of confidence in intangibles like these is challenging at best. Moreover, confidence and pessimism alike are contagious. As we see so often in the markets, confidence can build on itself and eventually lead to a bubble. Similarly, pessimism can accumulate, resulting in bear markets and even depression. It’s not at all clear where we are in the cycle of confidence, but it’s certainly worth monitoring and being positioned for a range of outcomes. ![]()

PORTFOLIO IMPLICATIONS

Confidence is a fragile and fuzzy notion. In many ways, America’s enduring sense of confidence and optimism has helped the U.S. economy, and by extension U.S. financial markets, to be a global leader for more than a century. We can’t, however, assume that this cycle of confidence, economic leadership and market strength will continue forever. It’s understandable for U.S. investors to look at Japan's struggles in recent decades, as well as the tepid scenario unfolding in much of the developed world, and wonder if a similar fate is in store for them at some point.

As suggested above, the U.S. economy faces some of the same structural factors as Japan did in the 1990s and 2000s, but the scale of the obstacles is lower for the U.S. given its younger and growing population and its relative breathing room with respect to interest rates and inflation. The U.S. does have policy options available to spur growth, but it is never easy to predict how policies may impact an economy’s long-term trajectory. For example, in the 1990s, Japan propped up its largest banks and corporations—enterprises that by all rights should have failed. These actions stunted the natural processes that recessions play in an economy. Specifically, Japan essentially prevented a healthy correction of misallocated capital and labor. Partly as a result, its economy never fully realigned. If U.S. policymakers become similarly fixated on preventing the next recession, there is a risk that their actions could have unintended consequences and create an even deeper long-term problem.

So how can we, as investors, navigate this complex and dynamic situation?

We can start with some broad thinking about long-term returns in the U.S. While nothing is certain, we believe that it’s healthy to plan for lower returns going forward than what we have seen in recent history. Today’s low interest rates make it likely that bond returns in the coming years will be lower than historical norms; we currently estimate long-term returns of 1.5%-3.0% for U.S. bonds, with some variation by specific asset class. At that return level, bonds would provide investors with a store of value and liquidity, and potentially outpace inflation, but it would be a much lower return than bond investors received in recent decades. Equity returns are less predictable, but we believe they are more likely than not to be lower going forward compared to the post-crisis period, given the outlook for modest GDP growth around the world alongside today’s elevated valuations. We estimate returns of 6-7% for U.S. equities (as measured by the S&P 500® Index) over the next decade, compared to ~10% over the past 50 years.

The key question for investors is how to respond to the prospect of lower returns, or as we described it in our 2018 Asset Allocation publication, the “risk of insufficient growth.” The macroeconomic and policy-oriented factors described above are largely out of our control and, for the most part, defy attempts at prediction. Concentrating on what we can control, there are three primary levers we can use to counter the possibility of lower broad-market returns:

Lever 1: Security selection. Despite macroeconomic headwinds in recent decades, many Japanese companies have still created value for investors. One example is Santen Pharmaceuticals, which outperformed global markets by taking advantage of the secular shift in Japan towards an aging demographic. Automaker Subaru also rewarded shareholders, thanks to strong product lineups that offered real value to car buyers and helped Subaru take market share from larger rivals such as GM and Toyota. In fact, Subaru has more than tripled its unit sales in the U.S. over the past decade.

We believe that in both good and bad economic times, bottom-up, fundamental research can uncover profitable investment opportunities. To this end, our research teams focus on identifying business models that are strong enough to survive and thrive in more difficult environments. In some cases like Santen, these companies benefit from structural tailwinds, such as e-commerce or mobility, that are strong enough to overcome slower GDP growth. In other cases, like Subaru, they may have a particularly strong industry position that propels their growth through market share gains.

Lever 2: Allocate to additional asset classes.* By looking beyond stocks and bonds, we can find numerous investment options that introduce new and different return drivers into portfolios. Real estate is a good example. While real estate is impacted by the same broad economic conditions that drive traditional portfolios, it is also driven by distinctive factors such as property supply, inflation and the local dynamics of individual markets. Additionally, opportunities within real estate differ from segment to segment; the return profiles of multi-family, office or industrial properties vary, and investments can range from income-focused ownership of established properties, to growth-focused opportunities in new construction.

Other asset classes offer low correlation to equities and fixed income because they are, for lack of a better term, “process-driven” rather than “market-driven.” These include activist strategies, which are propelled by a lead investor’s ability to drive strategic improvements in a company, or event-driven strategies, which capitalize on catalysts like merger and acquisition activity, restructuring, or regulatory shifts. (Our colleagues Sid Ahl and Jordan Wruble discussed these opportunities and others in their recent article, "Five Sources of Alpha in an Aging Market Cycle.") Each of these avenues comes with its own set of risks, but we believe that judicious selection can provide diversification and an opportunity to improve one’s long-term return outlook without increasing overall risk.

Lever 3: Prepare with good defense. Given the many unknowns in today’s environment, we believe that a moderately defensive asset allocation that provides ample liquidity is prudent. As Bill noted earlier, we generally advise our clients set aside a reserve of cash and equivalents apart from their core investment portfolio. This can help them to remain invested consistently over the long term, in alignment with long-term objectives, and make it less likely that they will feel the need or temptation to liquidate assets at depressed valuations. A core allocation to high-grade bonds can play a similar role. For clients with allocations in private equity, real estate or other investments that involve partnership structures with long-term capital commitments, liquidity reserves are especially important to ensure that clients can comfortably respond to near-term changes in circumstances.

As a final note, investors have the additional option of reaching further out along the risk spectrum (e.g., riskier stocks, or high-yield bonds) in an effort to maintain the same return profile to which they’ve grown accustomed, but we consider this option as somewhat perilous. Valuations across equity and credit markets are elevated relative to history, geopolitical risks are numerous and a variety of economic warning signs suggest that we are in the later innings of the current market cycle. Investors adding to risk now could jeopardize their ability to achieve long-term objectives if a recession were to occur in the next few years.

In summary, investors today face a financial landscape that looks very different from 25 years ago, as both interest rates and economic growth appear to have become structurally lower. The optimal portfolio approach for any given client will vary, but we believe that a plan that draws from the three options outlined above can help us position portfolios effectively for what comes next. ![]()

The views expressed are those of Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested.

The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

*Specific strategies discussed in this section, such as real estate, activist and event-driven strategies, are generally available to qualified purchasers and accredited investors only.

Price/earnings ratio is defined as the current share price of a company's stock, divided by its annual earnings per share.

The S&P 500® Index represents the large-cap segment of the U.S. equity markets and consists of approximately 500 leading companies in leading industries of the U.S. economy. Criteria evaluated include: market capitalization, financial viability, liquidity, public float, sector representation, and corporate structure. An index constituent must also be considered a U.S. company. The S&P 500® Industrials Index comprises those companies included in the S&P 500 Index that are classified as members of the industrials sector. Standard & Poor’s, S&P®, and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a subsidiary of S&P Global Inc. The NRI 350 Index is an broad index of Japanese stocks that excludes firms in the financial sector. Indexes used to represent asset classes in the chart displayed in this article: Japanese stocks are represented by the MSCI Japan Index, an index designed to measure the performance of the large and mid cap segments of the Japanese market. With 323 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in Japan. Global ex-Japan stocks are represented by the MSCI ACWI ex-Japan Index, an index that captures large and mid cap representation across 22 of 23 Developed Markets (DM) countries (excluding Japan) and 26 Emerging Markets (EM) countries. With 2,529 constituents, the index covers approximately 85% of the global equity opportunity set outside Japan. All MSCI indexes and products are trademarks and service marks of MSCI or its subsidiaries. Japanese bonds are represented by two indexes over time (due to availability of data at the start of the measured time period). From 1989-1996, this asset class is represented by the BofA/ML Japan Gov't. Bond Index, which tracks the performance of government debt issued publicly in Japan; from 1996-present, this asset class is represented by the BofA/ML Japan Broad Market Bond Index, which tracks the performance of investment-grade debt issued publicly in Japan. Global ex-Japan bonds are similarly represented by two different indexes over time. From 1989-1996, this asset class is represented by a market-cap-weighted blend of the BofA/ML U.S. Broad Market Index (which tracks the performance of investment-grade debt issued in the U.S.) and the BofA/ML Pan-European Gov't Bond Index (which tracks the performance of sovereign debt issued publicly across Europe). From 1996-present, this asset class is represented by the BofA/ML Global Broad Market Ex-JPY Index, which tracks the performance of investment-grade debt issued globally, excluding debt issued in Japan. BofA Merrill Lynch Indexes are service marks of BofA Merrill Lynch.

It is not possible for an investor to invest directly into an index.

BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS,BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG BONDTRADER, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS, BLOOMBERG.COM and BLOOMBERG LAW are trademarks and service marks of Bloomberg Finance L.P., a Delaware limited partnership, or its subsidiaries.