Last month’s sudden stock market “correction” serves as a vivid reminder that prices can move down at least as easily as they move up. While some investors were mystified by the severity of the pullback in the absence of meaningful incremental news, others argued that the pullback was long overdue, given the extended rally in what now has become the longest-running bull market in modern history.

Along with achieving strong long-term returns, protecting our clients’ capital is a critically important part of our challenge as investment advisors. Taken together, these two objectives involve finding the optimal combination of risk and return for each specific client situation. An important tool in this regard is diversification, or spreading risk across various asset classes and investment opportunities, each of which has a different return profile. Far from being a simple exercise, productive diversification requires a nuanced, analytical approach.

Multiple Risks

Stock prices, the skeptics say, have not reflected the reality of rising economic and political risks. While current economic conditions in the U.S. remain strong, interest rates are creeping slowly upward to reflect that strength, and the Federal Reserve seems intent on nudging rates gradually higher in order to dampen inflationary expectations. Deficit spending, resulting in part from the late 2017 tax reform legislation, is adding to the national debt at a rapid pace that will only worsen as interest rates climb. On the political front, trade wars have escalated, nuclear threats are not going away and domestic partisanship seems more severe than ever.

Optimists point to the economy’s robust growth in recent quarters and the likelihood of continued above average year-on-year gains in earnings. The stock market’s favorable performance in the face of rising external risks underscores the importance of profits as the primary driver of equities. Here, recent results have been attractive, and the near-term outlook appears good, but at some point, growth will likely slow, and a recession will set in.

The market’s recent action has heightened these and other concerns. As a result, many clients are asking how best to protect their portfolios against the inevitable downturn in stocks. In last summer’s Investment Perspectives, we discussed the merits of rebalancing, suggesting that bonds have become increasingly attractive relative to stocks as interest rates move up. Like any other asset class, of course, bonds carry risks that must be managed in line with client objectives. We also talked about the need to maintain adequate cash reserves—what we often call the “liquidity bucket”—to avoid the necessity of selling securities at inopportune times to meet the need for cash.

Diversification: An Enduring Strategy

Another common strategy to reduce risk is diversification—spreading one’s investments among various asset classes. On one level, this approach sounds simple: Own multiple asset classes or securities so that some perform favorably, while others may be under pressure. Given how difficult it is to predict when any particular one is likely to outperform others, our philosophy is to create a strategic asset allocation plan based on each client’s risk/return objectives. Based on this philosophy, we recommend that clients generally stay the course, making adjustments only at the margin when an asset class appears especially over- or undervalued. In practice, a number of factors need to be taken into account in order to produce the desired result.

Constructing an appropriately diversified portfolio involves a careful assessment of both the potential returns of various asset classes and their tendency to move together (or not). Typically, an array of benchmarks representing each asset class is used to gauge risk and return factors, and then managers or (in the case of passive management) ETFs or index funds are selected to populate the various parts of the portfolio.

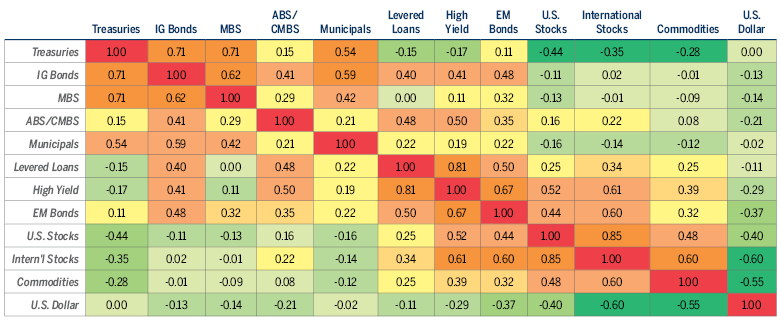

The chart below shows the degree to which various asset classes have been correlated with one another over the last 10 years. The closer a correlation value is to 1.00, the more likely the two asset classes are to move in the same direction at the same time. And if correlation is negative, they tend to move in opposite directions. Thus, if past patterns hold, one would expect that municipal bonds would be a better diversifier of U.S. stock holdings than, say, high-yield bonds.

PRUDENT DIVERSIFICATION CAN REDUCE OVERALL VOLATILITY

Correlations Among Asset Classes (Based on 10-Year Returns as of 9/30/2018)

Source: Bloomberg.

“Intelligent” Diversification

Indexes or benchmarks are one way to measure the performance of a particular asset class. From a fundamental perspective, the same macro themes that drive one part of an asset class tend to drive another. In the emerging markets, for example, demographic trends broadly favor the rise of the middle class, which is becoming a force for growth in consumption. In assessing the return potential of the asset class, this theme is the key driver affecting the growth of a number of emerging markets countries.

Historical benchmark returns, however, tell only part of the story. To gain a deeper appreciation for an asset class, it’s important to examine the benchmark in greater detail in order to analyze how its returns have been achieved. Again using the emerging markets—which have been under a cloud for most of the last two years—the majority of returns are driven by Asia, which currently dominates the MSCI Emerging Markets Index. Put another way, over- or underperformance in Asia currently has an outsized effect on how the Index is likely to behave. Depending on a number of factors, this may or may not be a positive for any particular portfolio, but in any case, it detracts from real diversification.

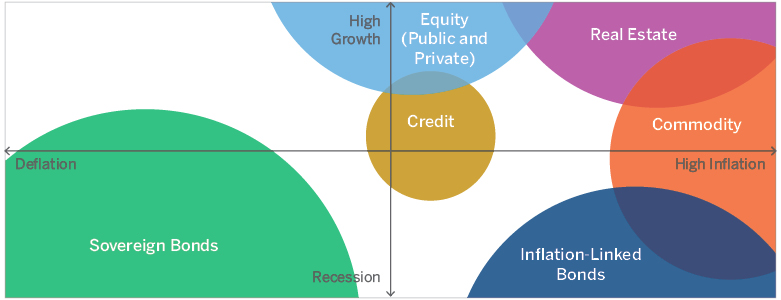

TRUE DOWNSIDE PROTECTION COMES FROM TRUE DIVERSIFICATION

Every asset class has its best- and worst-case economic scenarios. Equities thrive in a high-growth, moderate-inflation environment but falter in recessions. Commodities love inflation. Investment-grade bonds are often a portfolio's salvation during depressed periods but drag on performance during a booming market. Spreading portfolios across these asset classes is the best way to avoid overexposure to any one economic outcome.

Source: Brown Advisory.

Thus, it is important to understand the makeup of the Index in order to avoid unproductive concentration and achieve true diversification. Care must be taken to identify areas of opportunity within an asset class rather than simply engaging a manager whose geographic pattern of investments emulates an Index. By deviating from the Index a manager with the ability to identify profitable opportunities in a particular asset class may combine the best of both worlds: the diversification benefits offered by the asset class, along with “alpha,” or returns above the benchmark index.

A good example is provided by municipal bonds, which tend to be a very stable asset class. In fact, their very stability, combined with a slightly negative correlation with stocks, makes them an integral part of diversification strategies in balanced portfolios. As in other asset classes, deviation from a benchmark can enhance returns. In recent months, our bond team has used municipal floating rate bonds (which are not even a component of the Bloomberg Barclays 1-10 Year Municipal Bond Blend Index—the benchmark for our Tax-Exempt Bond strategy) to good effect. In August and September, the returns on short-term, fixed-rate bonds were particularly meager as investors poured money into them to protect against a possible rise in interest rates. Our concern was that the principal values of even short-duration bonds would be eroded if interest rates were to rise, so we allocated funds to variable-rate securities, which offered both better yield and principal stability. As it turned out, the quick rise in rates did result in principal erosion of fixed-rate bonds, causing the Index to post a loss for the quarter, while our position in variable-rate bonds produced a profit.

These examples illustrate the value of what might be called “intelligent” diversification. While investing in a range of asset classes will tend to reduce overall portfolio risk because of correlation attributes, the selection of specific managers or strategies can help avoid some of the unintended consequences (or risks) inherent in various indexes.

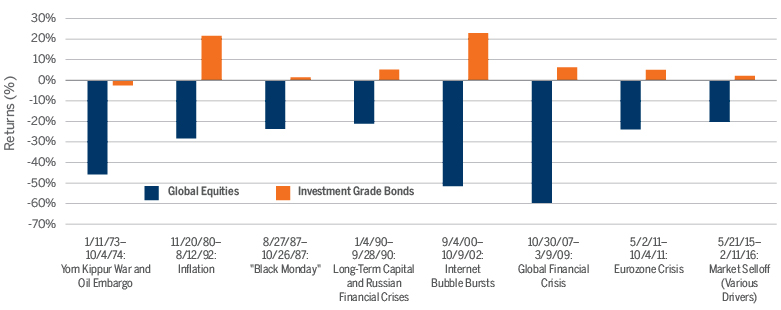

THE IMPACT OF DIVERSIFICATION DURING EQUITY DOWNTURNS (1973–PRESENT)

During notable periods of market turbulence over the past 40–50 years, investment grade bonds have consistently stood out and proven their value in diversified portfolios.

Source: Bloomberg.

Vertical Diversification

So far, this discussion has focused primarily on horizontal diversification—that is, across asset classes—while recognizing the need to understand the makeup of each one in order to achieve specific objectives. Investors should also pay attention to vertical diversification, or spreading risk within an asset class. A quick glance at the Forbes 400 list makes it clear that the largest fortunes have been made by concentrating on a single asset class or even a single security (Jeff Bezos in Amazon, Warren Buffett in Berkshire Hathaway, etc.)—living proof of the maxim that the most money is made by putting all your eggs in one basket and watching it very carefully. On the other hand, very little is published about the many failures resulting from this strategy, and, given the risks involved, it’s not something we can prudently recommend. In fact, since the vast majority of our clients have already created their wealth by the time they engage us, our responsibility involves protecting their wealth as well as growing it, finding the optimal combination of risk and return.

In our view, the best approach is to incur a degree of risk by limiting vertical diversification (i.e., owning relatively concentrated portfolios within each asset class) but control overall portfolio risk by investing horizontally across asset classes. Along these lines, mutual funds with investment strategies similar to ours typically contain two or three times as many securities as we own. Depending on the number of asset classes or styles in which a portfolio is invested, this level of vertical diversification could result in owning literally thousands of securities—making the impact of each one almost meaningless. To a large extent, our philosophy reflects a bias toward fundamental investing. Each investment we make is subject to a careful analysis of its business strategy, competitive position, management, financial resources and other variables. In the process, we either develop a high level of conviction in the likelihood of success or we pass on the opportunity. Our fundamental conviction with respect to each investment gives us confidence to hold fewer securities in each particular portfolio.

Taken to its logical extreme, this approach could lead to owning one stock (or bond, etc.) in each asset class, but in recognition that even a rigorous research process can be fallible, we hold a sufficient number of securities to diversify risk and dampen volatility. Large-cap U.S. equity portfolios typically own 30–50 stocks. It should also be pointed out that, unlike Mr. Bezos or Mr. Buffett, we have no control over the destiny of our company holdings, so our ability to “watch our basket” is much more limited.

A similar approach applies to our investments in alternative investments.* In private equity, for example, we recommend that clients diversify their investments in this asset class by both investment type and vintage year. Essentially two avenues exist for this type of investment. Clients with a high tolerance for risk may select from a variety of partnerships that we have researched and can gain access to in a particular year. In these instances, a client might invest in, say, an early-stage venture fund and an energy partnership this year because he or she likes the funds’ record and specific investment strategy, but next year his or her selections might be different. Because the spread in returns between top- and bottom-quartile performing partnerships is generally far greater than in the public markets, this approach can lead to vastly different results over time.

The second approach is to invest in so-called funds-of-funds, or partnerships that own large numbers of underlying venture, buyout, energy or other types of private equity funds. Because of overdiversification, many funds-of-funds produce results in line with overall private equity averages. In an effort to achieve above-average returns, our Private Equity Partners program limits the number of underlying funds to four to seven at a time. Since a new partnership is created every year or so, investors participating in the program over time can achieve diversification by “vintage year”—an important aspect considering that private equity returns are in part a function of the time in the market cycle that a new fund is launched. Similar to our belief in high-conviction public market portfolios, our philosophy in private equity is to make a relatively small number of well-researched investments.

How much diversification is enough? The answer depends primarily on two factors. Most important is the client’s specific situation, including return objectives, tolerance for risk and volatility, and need for liquidity. While short-term outcomes are unpredictable, long-term results should align with these client goals. The second factor revolves around the type of diversification employed. Depending on the mix of horizontal and vertical diversification—range of asset classes and the degree of concentration within each—significantly different levels of risk and return can be obtained. Every case is unique but must involve a clear and mutual understanding of objectives and the characteristics of each type of investment. ![]()

The views expressed are those of Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested.

The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client. It is not possible for an investor to invest directly into an index.

The Bloomberg Barclays 1-10 Year Municipal Bond Blend Index is a market value-weighted index which covers the short and intermediate components of the Barclays Municipal Bond Index—an unmanaged, market value-weighted index which covers the U.S. investment-grade tax-exempt bond market. The 1-10 Year Municipal Blend Index tracks tax-exempt municipal General Obligation, Revenue, Insured, and Pre-refunded bonds with a minimum $5 million par amount outstanding, issued as part of a transaction of at least $50 million, and with a remaining maturity from 1 up to (but not including) 12 years. The Index includes reinvestment of income.

Bloomberg Barclays Indices are trademarks of Bloomberg or its licensors, including Barclays Bank PLC. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS,BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG BONDTRADER, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS, BLOOMBERG.COM and BLOOMBERG LAW are trademarks and service marks of Bloomberg Finance L.P., a Delaware limited partnership, or its subsidiaries.

The MSCI Emerging Markets® Index captures large and mid cap representation across 23 Emerging Markets countries. With 834 constituents, the Index covers approximately 85% of the free float-adjusted market capitalization in each country. All MSCI indexes and products are trademarks and service marks of MSCI or its subsidiaries.

*Alternative investments may only be available to qualified purchasers or accredited investors.