The title of this piece may conjure up images of odd looking dogs or cats, or monkeys no longer able to dangle effectively from trees, but that’s not what we have in mind. Instead, we’re thinking of a phenomenon by the name of “kurtosis,” which may have implications for investing in today’s markets.

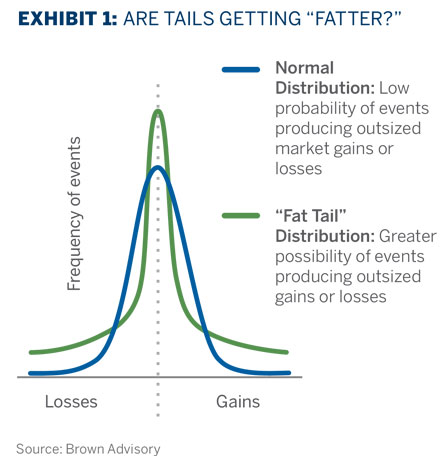

In simple terms, kurtosis is a measure of the risk of normally remote possibilities actually occurring. The chart below may be helpful in visualizing the concept. Statisticians depict the probability of events or outcomes as adhering to a bell-shaped curve, with the most likely outcomes tightly clustered around the middle of the curve while the least likely ones, with negligible probability of occurring, appear at the positive and negative extremities of the curve, called tails. A “normal distribution,” is said to occur when about 95% of the values lie within two standard deviations (a measure of dispersion) of the mean. Kurtosis happens when the probability of extreme outcomes rises, causing the tails on the bell curve to be elevated or “fattened.” Specifically, it measures the aggregate probability that outcomes in the two tails will occur. The greater the kurtosis, the more likely it is that extreme outcomes will come to pass.

Higher Kurtosis?

It strikes us that we may be in a period of elevated kurtosis. Just look at how two recent events unfolded relative to opinion poll predictions. Polls are supposed to measure consensus expectations of future events, but in the case of both Brexit and the U.S. Presidential election they clearly misjudged the situation, and seemingly low probability outcomes became reality. Who woulda thunk it?

The rally in stocks following the Brexit and U.S. Presidential votes suggests that investors quickly embraced the new, unexpected reality—also to the surprise of prognosticators. In the first instance, the markets apparently concluded that Britain’s exit from the European Union would not have a material negative impact on economic growth after all. In the second, investors seemed to focus on the prospects for tax cuts and deregulation that would boost corporate profits under the newly elected Trump administration.

Looking ahead, we would not be surprised by, well, further surprises. The inauguration of Donald Trump brought with it, at least for a time, an era of unpredictability in terms of policy agendas, executive actions and legislation. We say this without taking political sides—which we are always careful to avoid—but rather as an observation on the President’s particular communication style. And, of course, any new administration brings with it the uncertainty as to how it will prioritize and execute during its early days in power. Among the topics that might “fatten the tails” of possible outcomes, are:

- A nation divided: While Republicans control both houses of Congress, the White House and most state houses, Democrats are a vocal minority and making every effort to be heard, relying on their popular majority in the national election. Further, President Trump does not subscribe to conventional Republican ideology, and it appears that his views sometimes differ from those of his advisors. Thus, it’s difficult to predict what will happen on the political front and to identify which ideas will be put into action.

- International relations and trade: As the new administration moves away from multilateral trade agreements and toward bilateral ones seen as more advantageous to the U.S., it will be challenging to gauge the effect on trade generally and on the domestic economy specifically. Some argue that the balance of trade will swing in our favor, with a positive impact on manufacturing, while others point to the negative effect on U.S. inflation and overall growth. President Trump’s attempt to gain the upper hand in foreign relations with China, Russia, and the Middle East could also cause wider swings in investor sentiment.

- Populism in Europe: Election results in the U.S. and the December constitutional referendum in Italy, as well as the Brexit vote, raise the possibility of similar populist movements gaining traction in France and other parts of Europe, further threatening the sustainability of the European Union. The prospect of upsetting the “old” order introduces another layer of uncertainty on the investment horizon.

- Corporate profits: While Mr. Trump’s election raised animal spirits and caused some to raise earnings estimates, the range of forecasts for corporate profits this year is now unusually wide. Part of the reason is that analysts cannot be sure what tax rate to apply to pre-tax earnings and how to account for various deductions since new legislation has not been introduced, much less enacted. Again, the range of possible outcomes seems large.

Investment Positioning

If the current environment is susceptible to greater tail risk, how should one think about being positioned from an investment perspective? In theory, one might try to weight portfolios to favor those sectors or securities that would presumably benefit from low-probability factors on the positive side but not be hurt by similarly remote but negative possibilities. The problem with this approach is that remote possibilities are just that—remote—and often they are completely unforeseeable. Further, it is always challenging to know what outcomes are already factored into a stock or other security’s price.

Another possible answer is to invest in lower-volatility asset classes that tend to react less violently in the face of negative news. A good example is bonds, which we note are more attractively priced than they have been in several years, thanks in part to the run-up in interest rates since last fall. Rising rates have, in some sectors, been accompanied by wider yield spreads relative to Treasury bonds, boosting yields still further. Municipal bonds, for example, have seen rates nearly double, and BBB-rated bonds with four or five-year maturities now yield around 4%.

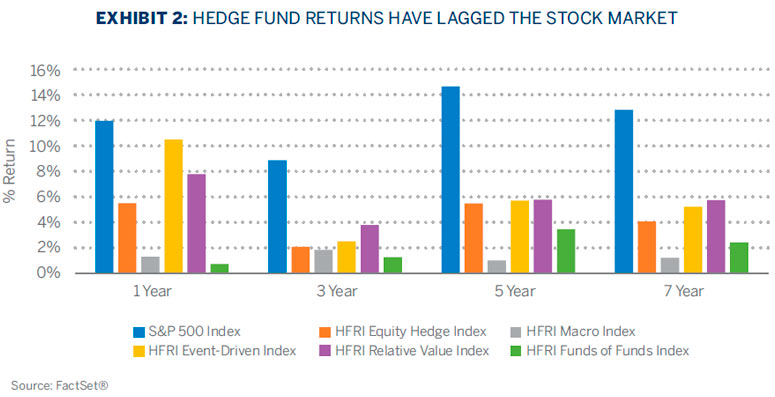

Hedge funds* provide another means to dampen the volatility that could result from fatter tails, but the case for them is more nuanced. Many investors, including some of the largest pension funds in the world, have withdrawn huge sums from hedge funds in the last couple of years, citing poor returns, high fees and lack of transparency. In July of last year alone, over $26 billion was withdrawn according to Bloomberg. Returns have indeed been lackluster for most funds. The widely followed HFRI Asset-Weighted Composite Index has returned 4.5% annually compared to 12.8% for the Standard & Poor’s 500® Index over the eight-year period ended December 31, 2016.

A Deeper Look

These figures deserve more careful scrutiny, however. First, hedge fund returns are reported net of fund fees, so no matter how burdensome the fees may seem they are subtracted out of final results. Second, it’s normal for hedge funds to lag stock market indices during periods of sharply rising prices. Funds typically maintain long and short positions, so unless the manager is extraordinarily successful in selecting individual securities, the presence of a short book will at least partially offset appreciation in the long portfolio. Thus, returns should be viewed in a risk adjusted context. Over the period mentioned above, the standard deviation (volatility) of the HFRI Index was just 4.1% while that of the S&P 500 was 12.7%. Adjusted for this risk factor, the hedge fund index actually outperformed the S&P Index—a record lost on many investors. Further, the correlation of hedge fund returns to those of stocks has remained low, so funds continue to serve as a useful diversifier in balanced portfolios.

Of course, the figures cited above represent averages across a large number of hedge funds and are therefore not representative of any single fund. Hedge funds pursue a wide variety of strategies, and returns vary tremendously depending on the strategy as well as individual managers. Moreover, some hedge funds are known for taking substantial risk in the form of outsized positions or the aggressive use of leverage.

The hedge fund industry has become increasingly “institutionalized” in recent years. Some of the consequences of this trend have been a growing emphasis on asset growth, an increasing reluctance to take risk, and higher overlap of individual holdings among managers. By focusing on managers that limit their asset growth, it is possible to invest in funds that, because of their smaller size, are able to access a broader range of securities and concentrate portfolios in their best ideas. Allocation to smaller managers also reduces the potential for overlap in holdings and high correlations between the managers (most large institutional managers are forced to invest in only the largest, most liquid securities). Concentration, however, comes with increased volatility of returns and requires a thoughtful approach to diversifying one’s allocation.

On the positive side, the institutionalization of hedge funds has led to both increased visibility into what securities managers own and downward pressure on fees. For those willing to do the research necessary to making multi-year commitments, many hedge funds are willing to offer meaningful discounts to their typical fees in return for the resulting increased stability of their asset bases. Over many years, these discounts can make the difference between a successful investment in the industry and one that fails to meet expectations.

As a result, we believe that clients are best served by owning a basket or portfolio of hedge funds to help reduce overall risk and volatility. Hedge “funds of funds” can be expensive, however. Management fees and carried interests are typically charged at the fund-of-funds level, thereby reducing the returns on the underlying funds. We also find that most partnerships of this type include a large number of funds (often 30 or more), bordering on over-diversification and dilution of the returns of the better managers. To address the need for risk reduction, our particular approach is to create partnerships consisting of fewer than 15 underlying funds with somewhat complementary styles and relatively little use of leverage. We do not charge a performance fee at the partnership level.

Still, studies show that there is significant “tail risk” even in highly diversified funds of funds. Interestingly, the primary factor behind this risk has less to do with investment considerations than with the lack of transparency in some funds. Despite recent consolidation, the hedge fund industry continues to attract new entrants (and retain existing ones) that in many cases lack operational expertise or simply do not commit the resources necessary to invest in best practices. When liquidity dries up, say in a financial crisis, these weaknesses are exposed and some funds are forced to close. For these reasons, it’s critically important to conduct in-depth operational due diligence on each fund being considered for a portfolio. If management is not open and transparent in responding to this type of research, it makes no sense to take the extra tail risk.

Research: Better Micro than Macro

Within the hedge fund universe, there is a category called “global macro,” in which managers base investment selections on their views of overall economic or political trends—i.e., big-picture factors rather than company- or industry-specific fundamentals. The Brexit vote was a good example, as managers expecting a “leave” outcome sold the equities of companies dependent on trade with the EU and bought those representing a play on domestic demand, only to find the outcome was the opposite of what they expected.

In the last few years, there have been numerous opportunities to make bets on the markets’ reaction to macro events, including several key elections, actions by the Federal Reserve, currency movements, and many others. Interestingly, however, global macro has been the worst performing segment of the hedge fund world (see Exhibit 2), suggesting that it is extremely challenging to forecast big events accurately. (To be fair, low interest rates and excess cash have also impeded performance.) Two implications come to mind:

- A sufficient number of macro outcomes are hidden deep in the “tails” of normal distributions so as to be unforecastable even to the keenest observer. Or, they have such a low probability of occurring that investors would not typically invest in them.

- Rather than attempting to forecast such global or macro events as the direction of interest rates or currency values, research is more productively used to focus on things that one has a better chance of getting right—like company specific fundamentals. Partly for this reason, most of our hedge fund investments are in long/short equity-oriented funds.

Taken together, these factors help define our internal research philosophy. We assiduously avoid forecasting events, market trends and other eventualities that are beyond our control, and instead concentrate our resources on matters that we believe lend themselves more readily to careful analysis. No doubt, research conclusions on stocks are often wrong, but if a particular analyst or manager is right even slightly more than 50% of the time he or she is ahead of the game. If tails are becoming fatter, this fundamental philosophy should serve our clients well.

*Private investments including Hedge Funds mentioned in this article may only be available for qualified purchasers and/or accredited investors.

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

The HFRI Event-Driven Index represents investment managers who maintain positions in companies currently or prospectively involved in corporate transactions of a wide variety including but not limited to mergers, restructurings, financial distress, tender offers, shareholder buybacks, debt exchanges, security issuance or other capital structure adjustments. Security types can range from most senior in the capital structure to most junior or subordinated, and frequently involve additional derivative securities. Event Driven exposure includes a combination of sensitivities to equity markets, credit markets and idiosyncratic, company specific developments. The HFRI Equity Hedge Index represents investment managers who maintain positions both long and short in primarily equity and equity derivative securities. The HFRI Relative Value Index represents investment managers who maintain positions in which the investment thesis is predicated on realization of a valuation discrepancy in the relationship between multiple securities. Managers employ a variety of fundamental and quantitative techniques to establish investment theses, and security types range broadly across equity, fixed income, derivative or other security types.The HFRI Macro Index represents investment managers which trade a broad range of strategies in which the investment process is predicated on movements in underlying economic variables and the impact these have on equity, fixed income, hard currency and commodity markets. The HFRI Fund of Funds Index invest with multiple managers through funds or managed accounts. The strategy designs a diversified portfolio of managers with the objective of significantly lowering the risk (volatility) of investing with an individual manager. The Fund of Funds manager has discretion in choosing which strategies to invest in for the portfolio. A manager may allocate funds to numerous managers within a single strategy, or with numerous managers in multiple strategies. The minimum investment in a Fund of Funds may be lower than an investment in an individual hedge fund or managed account.

The S&P 500® Index represents the large-cap segment of the U.S. equity markets and consists of approximately 500 leading companies in leading industries of the U.S. economy. Criteria evaluated include market capitalization, financial viability, liquidity, public float, sector representation and corporate structure. An index constituent must also be considered a U.S. company.

Bloomberg Barclays Indices are trademarks of Bloomberg or its licensors, including Barclays Bank PLC.

FactSet® is a registered trademark of FactSet Research Systems, Inc.

The HFRI Indexes are being used under license from Hedge Fund Research, Inc., www.hedgefundresearch.com, which does not approve of or endorse any of the products discussed in the contents of this presentation. HFR Index returns are subject to change without notice.

HFR®, HFRI®, HFRX®, HFRQ®, HFRU®, HFRL™, WWW.HEDGEFUNDRESEARCH.COM® and HEDGE FUND RESEARCH™ are the trademarks of Hedge Fund Research, Inc. Standard & Poor’s, S&P, and S&P 500 are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a subsidiary of S&P Global Inc.