Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing. As professional investors have found it increasingly challenging to meet or exceed market benchmarks, many of their clients have grown disillusioned with active management. Instead, they’ve turned to indexing their portfolios to the S&P 500® Index or some other relevant benchmark, thereby accepting “average” performance rather than trying for something better. The rapid growth of exchange-traded funds (ETFs) has also helped fuel the demand for passive investing, since many such vehicles emulate broad market indexes or sub-segments thereof. Let’s look at the pros and cons of indexing, and then see where it makes sense to use this tool.

Academics have long maintained that, in the aggregate, the performance of all equity managers will approximately equal overall market returns so that the “average” manager can be expected to underperform the market by the amount of all fees that it charges. In recent years, however, active managers, as a group, have underperformed by a wider margin, giving rise to the growing popularity of passive management. According to Morningstar (which tracks mutual funds and their performance), more than 80% of all actively managed U.S. large-cap equity mutual funds underperformed their benchmarks over the five years ended Dec. 31, 2016. Citing this lack of performance, Morningstar calculates that $236 billion flowed into passively managed U.S. equity funds in 2016 alone.1

Assuring "Average"

Indexing assures that one’s investment returns will fall short of a true “average” (defined by the specific benchmark chosen for the purpose of indexing) by the amount of the fees charged by an index fund. Generally, index fund fees are low because management costs are minimal (investment judgment is not required to track an index) and administrative expenses are typically spread over a large asset base. Thus, in most cases, using an index fund produces performance that closely tracks the benchmark.

If the assurance of average results underlies indexing’s appeal, it’s also the reason that many investors resist it. The optimist in us fosters hope that we can achieve above average performance by selecting a superior manager or set of managers. In theory, the odds of choosing correctly should be 50% (ignoring fees), but, as we’ve said, more managers have underperformed lately than outperformed.

The term “alpha” was developed in the late 1960s to describe how an investment has performed after accounting for risk. For a portfolio with a risk profile similar to that of the overall market, alpha measures the amount by which that portfolio’s returns exceed those of the market. Thus, active managers have, as a group, delivered “negative alpha” over the last several years.

The academic thesis that equity managers as a whole will approximately equal overall market returns is followed by a corollary: Some managers will outperform for periods of time, but it is impossible to predict which manager will deliver favorable results, or when they will do so—in other words, outperformance (alpha) is random. This assertion is open to debate and in fact has been refuted by various studies, but it gives some investors pause when considering active managers for their portfolios.

Manager Characteristics

Still, enough managers have delivered above-average results over time that it’s worthwhile identifying the characteristics they tend to share. A white paper entitled "Active Alpha," published by Brown Advisory in 2014, highlights several factors, including:

- Independent thinking: Studies have shown that managers whose portfolios differ significantly from their benchmarks are more likely to outperform. The term “active share” measures the degree to which a portfolio’s holdings differ from those of its benchmark, taking into account the number of stocks in the portfolio but not in the index and the difference in weightings of those stocks held in common. Portfolios with greater active share could be said to reflect more independent thinking on the part of the managers.

- Investment process: Although it’s difficult to quantify any particular aspect of the decision process applied in managing a portfolio, a 2003 study by Klaas Baks2 concluded that positive performance is less a function of the individual fund manager than a function of his or her firm, thereby arguing against selecting funds on the basis of a “star” manager. A culture of collaboration and teamwork appear to be more important. Consistency is also a factor: While some managers change the risk profile of their portfolios from time to time, usually in an attempt to adapt to market conditions, the successful ones are generally less variable in this regard. High portfolio turnover can be an indicator of changing risk.

Other studies highlight additional factors that seem to characterize successful managers:

- Governance: Management structure and manager tenure are meaningfully related to performance. Clear lines of authority, well-defined roles and process, and incentives aligned with long-term investment results are features of successful firms.

- Cost: Fees inherently drag on performance, and managers need to be efficient in deploying resources, but low fees and efficiency do not necessarily go hand in hand. Scale can be an important source of efficiency, but it needs to be weighed against a fund’s ability to maneuver. That is, large funds typically carry lower overall fees, but they may be limited in their ability to move in and out of specific holdings without affecting the markets.

None of this is to say that all or even most managers who have these qualities will necessarily outperform. There are exceptions to every rule, so no foolproof formula exists for identifying good managers. Nonetheless, these factors are important, and our Investment Solutions Group spends considerable time analyzing them when it conducts due diligence on managers for our clients.

The Role of Passive

Recognizing that it is challenging to find active managers who can consistently deliver alpha, let’s return to the question of whether passive investing has a legitimate role in client portfolios. As active managers ourselves, we might be expected to take a strong stance against indexing, but that is not the case. In our view, it’s not a question of whether, but under what circumstances.

The two primary factors to consider with regard to indexing are timing (i.e., are there better or worse moments in time to enact an indexing strategy) and choice of asset class (i.e., are certain segments of the market better targets for indexing than others).

First, let’s look at whether certain points in the market cycle are more opportune than others to use passive strategies. To be clear, we do not subscribe to “market timing” as a valid investment strategy. Attempting to buy and sell securities based on predictions of when the overall market for stocks or bonds will rise or fall is generally a hazardous and unproductive exercise. That said, it’s clear that the extended bull market has given rise to the increased use of indexing in recent years, raising the question of whether this is a good time to initiate a passive strategy.

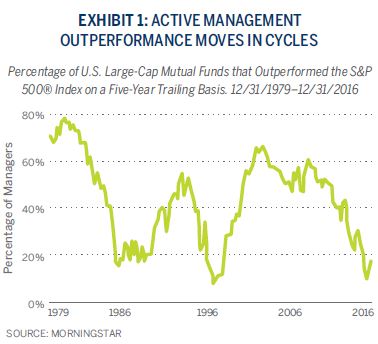

Times in the Cycle

Various studies suggest that active managers as a group tend to outperform their benchmarks during periods when the markets are weak and underperform when markets are stronger. Exhibit 1 at right illustrates this pattern; for example, it shows clearly how the relative performance of active managers has slipped during the bull market that started in 2009. Reasons for this tendency are varied. On the upside, active managers are often reluctant to overweight or “chase” the leading stocks in the market because those stocks typically sell at premium valuations. Looking back on Brown Advisory’s results in 1999 and early 2000, just before the technology bubble popped, our equity portfolios lagged the market, reflecting our discomfort with many of the high-flying “dot-com” stocks of the day. When the market then declined, we were relatively well-positioned by not being overcommitted to what turned out to be the higher-risk stocks.

When markets are falling, active managers often adopt a more conservative posture by increasing their cash positions (in some cases to meet anticipated redemptions) or switching to stocks with less aggressive valuations. As the current bull market ages and rolls over, it’s possible that the appeal of indexing may diminish as its results become less compelling on a relative basis.

In a similar vein, active strategies appear to perform better when markets are volatile and when the dispersion of returns for individual stocks is high. The most popular measure of market volatility is an index called the Chicago Board Options Exchange Volatility Index. Known as the VIX, this index indicates the market’s expectations of 30-day volatility based on S&P 500 Index options. In recent months the VIX has remained at exceptionally low levels, creating something of a headwind for active managers. Until lately, dispersion had also been low, with stocks tending to move together, leaving fewer opportunities for active managers. The recent rise in dispersion may portend a better environment for active managers.

Finally, it appears that active management results are stronger when measured over longer-term periods. A number of studies over the years have shown how certain investment managers have exhibited a higher likelihood of outperforming over longer periods of time than over shorter periods. Brown Advisory’s Flexible Equity strategy, the longest-running portfolio we manage, similarly has produced strong results over its 30-year history, despite several periods during those 30 years when the portfolio underperformed its benchmark. It underperformed primarily during very strong markets, as might be expected given its discipline with regard to valuations. These results should not be surprising, as it often takes years—not months or quarters—for an investment thesis to play out. This tendency is particularly true of “contrarian” investment strategies that deliberately go against the prevailing view on a stock, expecting that at some future point the consensus view will change.

Less Efficient Asset Classes

Turning to the question of whether some asset classes lend themselves more favorably to indexing than others, certain differences among them can be explained by the concept of market “efficiency.” This concept has its roots in academic studies from the 1960s and 1970s concerning the “efficient market hypothesis,” which held that a stock’s price reflected all relevant, currently known information. According to the hypothesis, there would be little point in trading on the basis of such information since it is only future (unknowable) information that will change the price. The efficient market hypothesis naturally gave rise to indexing.

In general, markets tend to be more “efficient” when more participants reflect a greater amount of information. Trading volume is then higher, reducing the spread between bid and ask prices, and contributing to liquidity. As a practical matter, the largest and most liquid stocks attract more research coverage from Wall Street brokerage firms because their institutional shareholders represent a large audience for analysts’ research opinions and their higher trading volume offers an opportunity to generate commission income. Despite the reduction of commission rates over the last 40 years, those stocks with the largest market capitalizations continue to attract research coverage from a great many firms and their analysts. Therefore, the market for U.S. large-cap stocks is highly efficient. With so many capable professionals covering the same stocks, gaining an information advantage that would lead to superior results is extremely difficult. Regulations governing inside information also level the playing field among market participants.

Small-cap stocks, in contrast, trade in lower volumes and attract far less Wall Street research coverage. According to FactSet®, 914 of the names in the Russell 2000® Index of small-cap stocks have fewer than five analysts covering them, while only eight of the companies in the S&P 500 Index have such meager sponsorship. Reflecting this pattern, Brown Advisory’s U.S. small-cap growth and value portfolios contain many stocks with only one or two Wall Street analysts providing coverage; this gives us the opportunity to gain an edge through our proprietary research. Along the same lines, international equities may offer a better opportunity for above-average returns than U.S. large-cap stocks.

With regard to bonds, the notion of efficiency is not as significant, but other factors have helped active managers outperform the indices. Bond benchmarks (like the Bloomberg Barclays Aggregate Bond Index) reflect the market weightings of various sectors that may be less relevant to active managers. In reaction to the financial crisis, for example, the U.S. government added substantially to its debt, so its fixed income obligations increased as a percentage of the broad benchmarks. At the same time, the corporate sector began cleaning up its balance sheet, improving credit quality. Most active managers took advantage of the spread between the low interest rates on Treasuries and higher corporate rates by overweighting corporates, thereby outperforming the indices. At other times in the cycle, active managers use different tools, such as high-yield bonds, credit research, etc., to adopt portfolio weightings that are far different from the indices.

With these factors in mind (and given recent results from active managers, shown in Exhibit 2 below, some investors prefer to “index the core” (using passive strategies in more efficient asset classes) and deploy active management where it is more likely to achieve superior results. We understand and appreciate this approach, which is particularly common among endowments, foundations and retirement plans for which tax considerations are not relevant. Over longer periods, we think active management can add alpha, even in more efficient asset classes.

Of course, certain illiquid asset classes, such as venture capital, buyouts and real estate, do not lend themselves to passive management, so it must be recognized that indexing has its limitations in terms of providing exposure across the investment spectrum. In short, indexing should be seen as part of the toolkit available for addressing a range of client objectives.

Specific Objectives

In discussing the role of passive management in portfolios, it’s important not to lose sight of the most critical consideration: client objectives. For many clients, the performance of their portfolio relative to a broad market index is not the most critical factor. Instead, they may be more concerned with yield, cash flow, volatility reduction, tracking error (how closely a portfolio tracks its benchmark) or other goals. Accordingly, we use our research process to create concentrated, customized portfolios specifically designed to meet these types of objectives. Stock-specific fundamental research from our equity research teams, along with input on asset allocation from our Investment Solutions Group, can be supplemented by customized portfolio analytics to achieve client-defined outcomes.

In short, every situation is different. Passive investing can play a key role under certain circumstances, but each one must be evaluated in the context of achieving well-defined objectives. ![]()

1https://corporate.morningstar.com/US/documents/ AssetFlows/AssetFlowsJan2017.pdf

2On the Performance of Mutual Fund Managers," Baks, Emory University, June 2003.

*Private investments including hedge funds mentioned in this article may only be available for qualified purchasers and/or accredited investors.

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

The S&P 500® Index represents the large-cap segment of the U.S. equity markets and consists of approximately 500 leading companies in leading industries of the U.S. economy. Criteria evaluated include market capitalization, financial viability, liquidity, public float, sector representation and corporate structure. An index constituent must also be considered a U.S. company.

The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 is a subset of the Russell 3000®Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000 Index is constructed to provide a comprehensive and unbiased small-cap barometer and is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set.

The MSCI ACWI Ex U.S. Index is a market-capitalization-weighted index maintained by Morgan Stanley Capital International (MSCI) and designed to provide a broad measure of stock performance throughout the world, with the exception of U.S.-based companies. The MSCI All Country World Index Ex-U.S. includes both developed and emerging markets.

The Bloomberg Barclays Aggregate Bond Index is an unmanaged, market-value weighted index composed of taxable U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate, asset-backed and mortgage-backed securities between one and 10 years.

Standard & Poor’s, S&P, and S&P 500 are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a subsidiary of S&P Global Inc.

“FTSE®”, “Russell®”, “MTS®”, “FTSE TMX®” and “FTSE Russell” and other service marks and trademarks related to the FTSE or Russell indexes are trademarks of the London Stock Exchange Group companies.

All MSCI indexes and products are trademarks and service marks of MSCI or its subsidiaries.

Bloomberg Barclays Indices are trademarks of Bloomberg or its licensors, including Barclays Bank PLC.