One of the most penetrating and recurring questions we receive from clients is, “what is a reasonable long-term expectation for U.S. stock market returns?” Since equities typically comprise the largest single component of a balanced portfolio, they are the greatest single determinant of overall returns for institutional and private clients alike. Changes in their assumed rate of return can impact decisions ranging from asset allocation to the spending level that a portfolio can rationally support. Thus, it’s important to have a view on this key question.

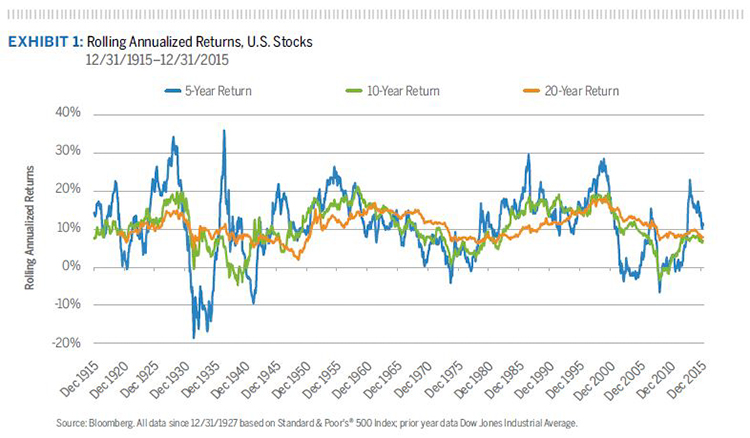

In this context, we are not referring to the outlook for stocks over the next quarter or even the next year or two. Instead, we’re looking 10, 20 or 30 years ahead—a long enough horizon to smooth out short-term fluctuations resulting from variables such as economic cycles, changes in interest rates and geopolitical events. Exhibit 1 on the next page illustrates that even periods of 10 or 20 years can produce widely varying returns, since the calculation depends in part on the exact beginning and ending dates. Still, investors need to incorporate a reasonable long-term assumption into their portfolio projections.

Endowment funds provide a useful window into this issue: Investment committees and boards of trustees with which we work recognize that the institutions they represent depend on a reasonably predictable level of cash flow to help fund their operating requirements. (Large, well-endowed institutions sometimes cover half or more of their operating costs by the draw from their endowments.) In order to preserve the purchasing power of the endowment, the annual draw must not exceed the long-term expected return on the portfolio return net of inflation (i.e., the “real” return). If spending is less than the real return, the purchasing power will grow for the future benefit of the institution, and the reverse will be true if spending exceeds the real return.

Private clients typically find themselves in a similar position, although they may not describe it in the same terms. If the long-term return on one’s investments is, say, 6% and inflation is 2%, then (ignoring taxes and expenses) a 4% annual draw would preserve the portfolio’s purchasing power for future generations. On the other hand, a 5% return, 2% inflation and a 4% draw would diminish the portfolio’s real value gradually over time, reducing its ability to fund one’s lifestyle and leaving less to heirs. With life expectancies continuing to rise, outspending the inflation-adjusted return by even a small amount can lead to a sizable difference in the true terminal value of a portfolio because the impact would be compounded over time.

Key Factors

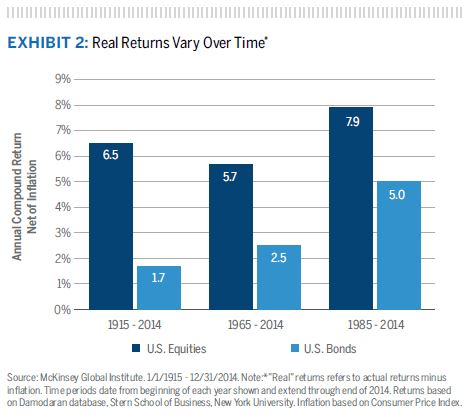

For these reasons, it’s important that the underlying assumptions about equity returns be reasonably accurate when constructing a portfolio. If the assumptions are too optimistic, the result can be financial pain. Let’s look at some of the variables. Assumptions about future returns are often made on the basis of long-term historical figures. A May 2016 report ominously entitled Diminishing Returns: Why Investors May Need to Lower Their Expectations, by the McKinsey Global Institute, addresses this issue. According to the report, annual inflation-adjusted U.S. stock returns (shown in Exhibit 2, page 3) were 6.5% over the last 100 years (1915–2014), but interestingly, they increased to 7.9% over the more recent 30-year period. Bond returns, too, were strong at 5% in real terms over the same period, about triple their 100-year figure. Looking back over the 30 years beginning in 1985, a number of factors contributed to the strong performance of equities. After an extended decline from their peak in 1973, U.S. stocks hit bottom in August 1982, rallied and then fell back in mid-1984 before resuming their long march upward. Thus, the January 1985 starting point for 30-year study was somewhat fortuitous for stocks. Timing aside, from a fundamental perspective, three key factors were primarily responsible for the strong performance of stocks during the period:

- First and foremost, interest rates have fallen to all-time lows. Ten-year yields on U.S. government bonds haven’t exceeded 2% for most of the past four years, compared to more than 11% in early 1985. While few economists predict a move back to high- or even mid-single digits any time in the next few years, it is difficult to imagine that they will go much lower unless deflation sets in—an unlikely prospect, in our view. Low rates are generally good for stocks, as they tend to drive investors into riskier asset classes with higher return potential. The Federal Reserve’s post-crisis program of buying bonds, known as quantitative easing, is credited with pushing down interest rates and spurring investment in equities.

- Corporate profits have grown dramatically during the past 30 years. In addition to lower borrowing costs, strong productivity gains—at least until recently—have fueled profit growth. McKinsey points out that the after-tax profit margin of publicly traded North American companies increased from 5.6% to 9.0% during the 30-year period, a gain of 60%. Margins have also benefited to a certain extent from the gradually changing mix of American business from manufacturing to higher-profit sectors, like services, media and software. While this shift is likely to continue, its effect probably won’t drive overall profit margins at the same rate as during recent decades.

- Also fueling stock returns are price/earnings ratios, which have increased from about 10 times (based on forward 12-months earnings per share) in the mid-1980s to about 15 times in 2014. One can argue that today’s low interest rates merit even higher valuations, but there’s no disputing that the increase in price/earnings ratios has been an important driver of stocks since the lows of the early 1980s. The market’s price/earnings ratio today is about in line with historical averages and, by some calculations, is in fact well above average, so we believe it would be unwise to assume that it will move significantly higher during the very long term.

Reversion to the Mean?

If the last 30 years have witnessed unusually strong capital markets in the context of their longer-term history, it would seem logical that the next 30 years could see a resumption of something closer to the long-term average, or even below the average. After all, returns can stay above their long-term average for only so long and presumably will revert to their mean at some point. If inflation-adjusted stock market returns averaged nearly 8% during the past 30 years, a figure closer to 6% would appear reasonable, based on the variables above. Bonds, too, will probably produce returns more like their 100-year average of 1.7% rather than the 5% that has prevailed since 1985.

Our Investment Solutions Group spends considerable time trying to gauge the long-term outlook for stocks since it is central to asset allocation decisions and recommendations. Using a multivariate regression analysis, the group recently estimated an expected 10-year return of 7% for stocks based on a combination of today’s equity valuations, projected growth in the economy and reasonable assumptions for interest rates. If inflation were to continue at its recent rate of about 1.5%, the 7% figure would translate into 5.5% in real terms—similar to the 6% projection above and slightly below the 100-year average of 6.5%. Let’s be clear, however: Projecting long-term returns is not an exact science, and we won’t know the results for another 20 or 30 years!

To many investors, a long-term inflation-adjusted return of 5.5% to 6% on stocks would seem more than acceptable. When combined with other, more stable but lower-returning asset classes, such a figure could result in an overall portfolio return of, say, 5% in real terms, depending on the asset mix. Thus, a draw of 5% (or perhaps more like 4%, after allowing for taxes and expenses) from the portfolio annually would allow the purchasing power of the assets to be preserved over time—again, depending on the asset mix and other factors specific to each particular situation. Of course, equity returns are never stable, so the dollar amount of the draw will vary as the portfolio rises and falls. The variability factor can be addressed by using an averaging approach, much as endowments typically do.

If the long-term real return does, in fact, decline from the roughly 8% level of “recent” history, many investors will need to adjust their expectations— and probably their spending rate—to the new reality. This adjustment doesn’t take place overnight but instead is a gradual process, and one that in many respects is already well underway. During the past 10 years ended May 31, the Standard & Poor’s 500® Index has returned 7.4% annualized, or just under 6% net of inflation as measured by the Consumer Price Index. The gain for the past two years has been about 6%, or roughly 5% after inflation is deducted. Perhaps this reflects a beginning of reversion to the mean. Following the 2007–2008 financial crisis, some observers began referring to the “new normal.” Although stocks performed very well during the first few years after the crisis, the sluggish economic recovery has seemingly dampened investor expectations—perhaps even for the long term.

Adjusting to the "New Normal"

Many investors, then, have lowered their sights with regard to equity returns for the next several years, if not the next 30. In making this adjustment, some have increased allocations to alternatives like venture capital, buyout funds, hedge funds and real estate in an effort to maintain portfolio performance.* We at Brown Advisory are believers in alternatives as a means of portfolio diversification and enhanced returns, but it is important to recognize that they involve giving up liquidity. And keep in mind that the returns available in alternatives are linked to equities, particularly in the case of private equity and hedge funds which, after all, are dependent on the stock market in one way or another. So returns in the alternative world may, like equities, be less robust than they have been for the last three decades. Certainly, that has been the case in hedge funds, whose heyday was in the 1990s. Since then, they have attracted much more capital and competition.

In the “new normal” world of lower prospective returns, it may be tempting to turn to indexing, or “passive” investing, as a possible strategy. The primary advantage of indexing is its lower cost versus active management since computers essentially do the work of assembling a portfolio that emulates a broad market index or sector of the market. Little or no human judgment is involved. Depending on the fund, expense ratios can be below one-tenth of a percentage point annually. That is a small fraction of the total expense for active management, which varies by specific manager and the size of the assets involved. Saving on fees can be appealing when overall returns are modest.

Owning an entire index—whether it’s the S&P 500, one of the broader Russell® indices or any other market benchmark—also has the appeal of being less volatile than a more concentrated portfolio. The same is true for exchange-traded funds (ETFs), which generally own large numbers of stocks in a portfolio designed to mimic a market index or sector, such as financials.

Although we are active managers ourselves—and therefore believe that solid fundamental research coupled with good judgment will produce attractive long-term results—we recognize that passive investing can have a valid role in portfolios. In general, we will not hesitate to use a passive approach if we think that it is likely to yield better overall results than an active manager in a specific asset class. An example is real estate investment trusts (REITs), in which most active managers own somewhat similar portfolios (and consequently tend to deliver average results) because of the limited number of publicly traded securities available. There are, however, a few caveats to keep in mind:

- Passive investing is most effective in highly “efficient” asset classes—i.e., those characterized by large numbers of research intensive market participants where gaining an information edge to beat the index is particularly challenging. For this reason, large-cap U.S. equities lend themselves to indexing better than small-cap stocks or bonds.

- Certain types of passive investment vehicles, such as ETFs, may trade at a very slight discount to their “net asset value” (the actual value of the underlying securities in the portfolio). Such discounts are less likely to occur when the holdings consist of highly liquid securities because such securities offer market participants the opportunity to arbitrage away the discounts.

- Passive investing in bonds is not especially productive for the reasons cited above. Moreover, they often offer lower-than-market yields because of the need to own the largest and most liquid bonds in order to track an index. These factors tend to limit the number of passive vehicles available to fill specific niches in a portfolio. In contrast, investors can choose from hundreds of different passively managed equity funds.

While indexing may be an efficient way to participate in the markets, by definition, it produces average results, so it may not meet an investor’s long-term expectations or needs. We cannot be sure whether stocks will in fact produce lower returns than those to which most investors have become accustomed, but we believe it would be imprudent to assume otherwise. At the same time, our job as investment advisors is to find client-specific solutions that address this challenge, whether through active management, indexing, alternatives or advising on appropriate levels of spending in light of real returns.

* May only be available for qualified purchasers or accredited investors.

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

S&P 500® Index represents the large-cap segment of the U.S. equity markets and consists of approximately 500 leading companies in leading industries of the U.S. economy. Criteria evaluated include: market capitalization, financial viability, liquidity, public float, sector representation and corporate structure. An index constituent must also be considered a U.S. company.

S&P® and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC.

Russell® when related to the Russell indexes is a trademark of the London Stock Exchange Group of companies.