For most investors, a primary objective is creating an optimal portfolio allocation that maximizes returns for a given level of risk. When designing portfolios, investors might consider various things such as allocating to mixed asset classes, different types of securities or geographies. Key considerations will likely include historical performance, correlation of returns, and volatility.

This article examines the argument for including an allocation to US small-cap companies in a balanced portfolio – a group that is often underrepresented but that can, if managed well, deliver diversification and positive returns over the long term.

Key Benefits of Small-Cap Investing:

- Diversification - lower correlation to large-caps improves overall portfolio efficiency.

- Growth potential - younger, faster growing companies earlier in life cycle.

- Sector/Industry breadth - wider array of sectors and industries compared to large-caps.

- Under researched - lack of coverage contributes to mispricing and opportunities.

- Active management – market inefficiencies allow skilled stock-pickers to add alpha.

- Expanded opportunity set - Vast universe of around 2,000 (in the US) small caps to select from.

Demystifying Small-Caps

Small-cap investing has a rich history that spans decades and reflects the evolution of financial markets and investment strategies. In the US, small-cap stocks typically represent companies with a total market capitalization ranging between $300 million and several billion dollars

The history of small-cap investing is blurry, but a significant moment came in the post-World War II era with the rise of mutual funds and the advent of portfolio diversification theories, such as Harry Markowitz’s Modern Portfolio Theory in the 1950s. This led to a greater appreciation for the role of small-cap stocks in achieving benefits derived from a diversified portfolio.

The introduction of the Russell 2000® Index in the 1980s marked a big step forward for small-cap companies and made it easier for investors to gain exposure. Since then, the increased availability of data and advancements in technology has made it possible for investors to conduct more thorough research and analysis.

The Small-Cap Opportunity

Put simply, the universe of small-cap companies covers a wide breadth of sectors, industries and factors compared to the relatively narrow large-cap market which is dwarfed by a few enormous organisations. Exploring these smaller companies could provide early access to the successful businesses that will likely make up the future mid and large-cap universe.

The host of opportunities in this space opens a range of complementary dimensions for investors. The advantages of carving out space for small-cap companies in a portfolio start to become obvious. For example:

1) The diversification boost – this seems straightforward. Why restrict a portfolio to large-cap stocks when the opportunities are far wider? It could even be argued that the lower correlation between small-and large-cap stocks improves overall portfolio efficiency. Put simply, small-cap companies behave differently (for example, they are often nimbler and can react faster to change), providing diversification.

2) Small-caps, big growth – smaller companies tend to grow revenues and earnings faster than their larger counterparts. Investing in these companies early in their life cycle could therefore provide more upside. In other words, the expansion opportunity is greater.

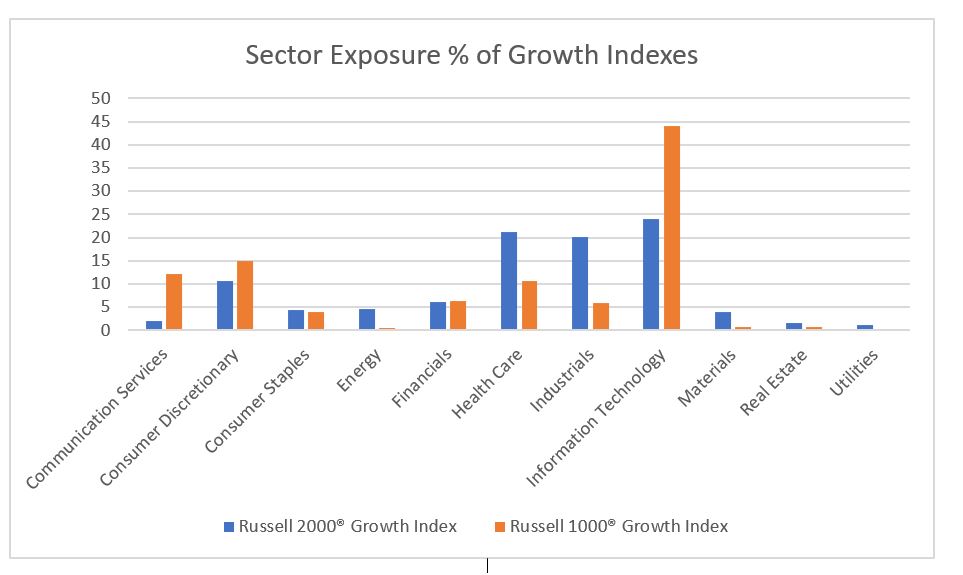

3) Spanning the economic landscape– we have already acknowledged the much larger number of companies available to invest in versus the large-cap space. Add to that fact that the breadth of sectors that small-cap companies span is wider than their large-cap counterparts who are typically concentrated in sectors like technology as the chart below demonstrates.

Source: Factset as of 03/31/2024. Sectors are based on the Global Industry Classification Standard (GICS) classification system.

Balancing the Risks and Rewards

Of course, with opportunity, comes risk and balancing the two takes expertise.

In this case, the smaller size of these firms compared to their large-cap counterparts introduces higher idiosyncratic risk, or the risk associated with the individual investment in a company. Examples might include the impact of a management team’s decisions, the culture of an organisation, new competitors, or a change in a legal framework.

Liquidity risk is another key area to consider. Low trading volumes can lead to wider bid-ask spreads and difficulties exiting positions. Other issues like crowded trades can exacerbate liquidity challenges and result in higher share price volatility.

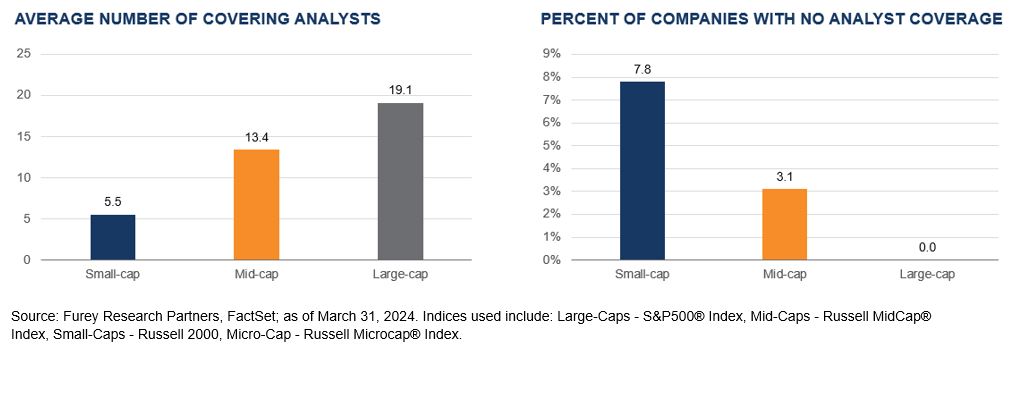

Finally, due to a lack of analyst lack coverage, there is generally less availability of information than might typically be seen in larger cap companies.

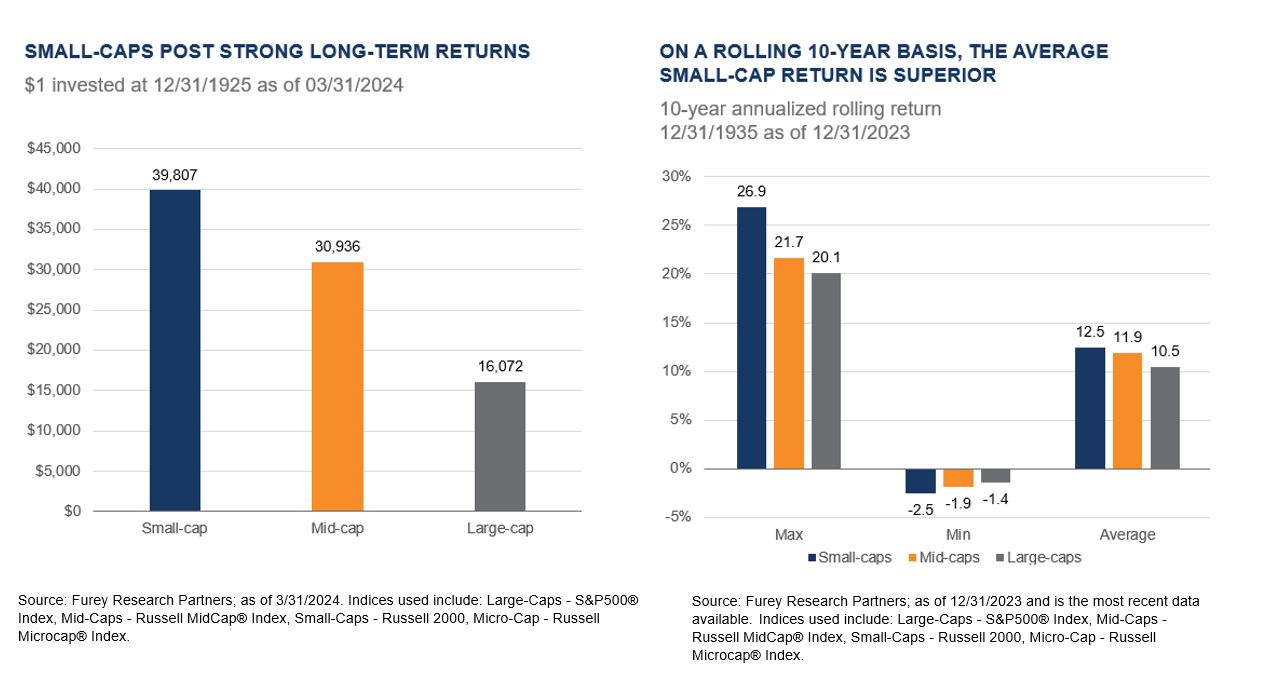

All of this can result in higher volatility and requires a higher appetite for risk. But for patient investors, the results could be worth waiting for as the charts highlight below. To achieve this, active managers, supported by specialist research teams are key to mitigating the risks, selecting the best opportunities and taking advantage of any volatility for an attractive entry point. Implementation requires diligent security selection and risk management – an important reason for a rigorous investment philosophy and process.

The Active Advantage

Skilled active small-cap managers can add alpha by exploiting their experience, their deep research and sticking to their investment process in different market environments. There are various opportunities that investors can exploit to generate alpha in this space:

- Inefficiency – the small-cap universe is typically far less thoroughly researched than large-caps as illustrated in the charts below. The relative lack of analyst coverage can contribute to mispricing that creates potential opportunities – that is, without experts actively evaluating a stock, shares can diverge from their fair value.

- The power of stock-picking– with over 2,000 companies to choose from in the US alone, active managers can dig deep to identify promising growth stories or undervalued opportunities that may be overlooked by the broader market.

- Specialization – managers and research analysts who focus on this area develop the expertise needed to uncover specific sectors, industries or geographic niches that may be under-represented in small-cap indexes. For example, an analyst might specialize in software companies or emerging biotechs. This can help identify promising opportunities that others may overlook or misunderstand.

America’s Small-Cap Advantage

A dedicated US small-cap mandate with high active share, focused on high-quality companies and mitigating downside risks, may enable investors to capitalize on the long-term potential found in US small-cap equities.

- US-based smaller companies include an exciting and dynamic group of growing businesses that typically demonstrate high innovation and strong entrepreneurial cultures.

- Over half of global smaller companies – more than 2,000 companies – are listed in the US, creating a huge opportunity.

- US smaller companies offer a deep and liquid market but are typically not as well covered by sell-side research analysts as their larger counterparts, creating inefficiencies and missed opportunities that can be exploited.

- A US stock market listing means there are high governance hurdles relative to their global peers, considerably reducing the risk profile of US smaller companies.

Levering Experience and Expertise

Brown Advisory has been investing in small, medium and large-sized companies in the US for over 25 years. Across its range of small-cap strategies, it manages approximately $9.6bn on behalf of institutional and intermediary clients as well as high net worth individuals. Clients benefit from Brown Advisory’s extensive research capabilities with a large team who cover the entire US market – analysing different sized companies (as they grow) and how they interact with one another across the spectrum. Alongside this, the firm benefits from an extensive network of venture capital, private equity and corporate relationships . Understanding the full spectrum of private and public companies is of fundamental importance to not only have a full picture of the competitive landscape but also to have access to the companies that might be likely to float in the future.

Brown Advisory believes that disciplined, bottom-up research, coupled with collaborative teamwork and the free exchange of ideas amongst colleagues, are the keys to achieving long-term outperformance. The combination of its investment philosophy and its client-first culture helps to make Brown Advisory a compelling portfolio manager.

In Summary

Offering diversification, growth potential, and a breadth of opportunities, in our view, small-caps deserve serious portfolio consideration - while individually small, collectively they account for nearly 3/4 of all U.S. listed companies across a diverse mix of sectors . Though sometimes neglected, this niche allows skilled active managers to unlock overlooked value. Despite higher risks, a modest small-cap allocation can enhance portfolio efficiency for patient, long-term investors aiming to boost returns.

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

1 Factset. Data as of 03/31/2024.

2Data as of 03/31/2024. Client assets are held in the following entities: Brown Advisory LLC, Brown Investment Advisory & Trust Company, Brown Advisory Ltd., Brown Advisory Trust Company of Delaware, LLC Brown Advisory Investment Solutions Group LLC, NextGen Venture Partners LLC and Signature Financial Management, Inc.

3Alternative investments may be available for Qualified Purchasers and Accredited Investors only.

4Source: Factset. Data as of 03/31/2024.

Factset® is a registered trademark of Factset Research Systems, Inc

The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values.

The Russell 2000® Growth Index measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000 companies with higher price-to-value ratios and higher forecasted growth values.

The Russell Microcap® Index measures the performance of the microcap segment of the U.S. equity market. It makes up less than 3% of the U.S. equity market. It includes 1,000 of the smallest securities in the Russell 2000 Index based on a combination of their market cap and current index membership and it also includes up to the next 1,000 stocks.

The Russell MidCap Growth Index Index is an unmanaged index that measures the performance of those Russell Midcap companies with higher price-to-book ratios and higher forecasted growth values. It is not possible to invest directly in an index.

Russell® and other service marks and trademarks related to the Russell indexes are trademarks of the London Stock Exchange Group Companies

Russell® and other service marks and trademarks related to the Russell indexes are trademarks of the London Stock Exchange Group Companies.

The S&P 500 Index, an unmanaged index, consists of 500 stocks chosen for market size, liquidity, and industry group representation. It is a market-value weighted index (stock price times number of shares outstanding), with each stock's weight in the Index proportionate to its market value.

Standard & Poor’s, S&P®, and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a subsidiary of S&P Global Inc

Global Industry Classification Standard (GICS) and “GICS” are service makers/trademarks of MSCI and Standard & Poor’s.