The abrupt stock market downturn in February was “officially” a market correction, according to the conventional definition (a market decline of more than 10%). It certainly created some anxious moments, but it also caused many investors to worry about the aging bull market and the potential for a more sustained pullback.

The word “corrections” conjures up all sorts of different images. Most are negative—from a teacher’s red marks on your final exam, to a grim institution purporting to improve the behavior of criminals. The term also refers to stock market declines of 10% or so—again, not a pleasant experience.

We heard the term used in its investment context quite a bit in February, and for the vast majority of investors, the correction we experienced last month (and may still be experiencing) led to some anxious moments. From an all-time high on Jan. 26, the S&P 500® Index dropped 10.2% in the space of just nine trading days, sending shivers through the ranks of professional traders and main-street investors alike. The steepness of the decline seemed particularly alarming. When the Dow Jones Industrial Average fell nearly 1,200 points on Feb. 5, it made front-page news, although at 4.6% the day’s decline would not even rank among the worst 50 days in its trading history.

Corrections are a normal part of market cycles, but they are still painful when they occur. One reason that investors were spooked this time around was that they had been lulled into complacency by the market’s pattern over the previous year and longer. Through January 2018, stocks had risen for 10 straight months, the longest consecutive monthly string since an 11-month streak in 1959. January itself was one of the best months for stocks in decades, as the Dow rose nearly 8%. Further, 2017 overall was extraordinary for its lack of market volatility; the S&P 500 Index rose steadily throughout the year without so much as a 3% pullback—a first in the Index’s long history. From a longer-term perspective, stocks rose from 2009 until this recent correction with only a few setbacks along the way. Even after recent record-setting gains, investors remained positive about the prospects for further profits. For example, the Investors Intelligence U.S. Advisors Sentiment Report registered 66.7% bullish on Jan. 17, its highest reading since 1986.

Causes of the Correction

At the risk of oversimplifying, it seems that four primary factors triggered the sudden initial sell-off in stocks in February and then caused it to accelerate.

- On Feb. 2, the U.S. Department of Labor reported a 2.9% increase in the average hourly wage rate, the fastest rise in that rate since 2009. (It was since revised to 2.8%.) Although the figure was only slightly higher than anticipated, it gave rise to fears that long-awaited labor-driven inflationary forces were beginning to emerge.

- Worries about inflation caused interest rates to creep up further. In the first two weeks of February, for example, the 10-year Treasury bond yield rose from 2.7% to 2.9%. Although the 10-year yield had already ticked upward from about 2.3% since mid-December, its potential for crossing the 3% threshold seemed to grab investor attention. Soon, some forecasters were predicting that the Federal Reserve would increase interest rates four times in 2018 rather than the two or three times most people had been assuming.

- As worries mounted with regard to higher inflation and interest rates, investors refocused on the stimulative influence of the Tax Cuts and Jobs Act. With the most recent economic data showing signs of acceleration, more observers began to question the wisdom of introducing fiscal stimulation at a time when the economy was already gaining momentum. The prospect of legislative agreement to significantly increase federal spending on defense and infrastructure only added fuel to the fire.

- Technical factors also contributed to the swift decline in stocks. The CBOE Volatility Index, known as the VIX, was a particular source of controversy. In essence, the VIX is a measure of the range of movement expected by investors in the S&P 500 Index over the next year. For most of 2017, the VIX was exceptionally depressed, signaling that investors expected very little volatility in prices. When the market suddenly sold off, the VIX rose as it typically does in response to fears of higher volatility. Investors who had sold the VIX short had to cover their positions at much higher prices, propelling the VIX upward and causing even greater anxiety in the markets.

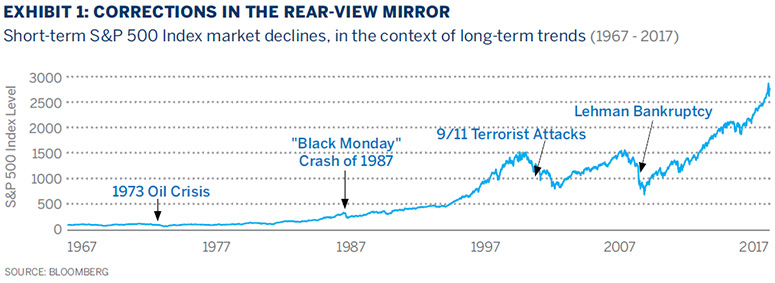

Corrections in Context

Unnerving as corrections can be, it’s important to keep them in perspective and focus on longer-term fundamentals. A few years from now, this winter’s correction will probably appear as only a minor squiggle on stock charts. The more important question is whether the general direction of the market will be up or down over the next few years. On that question, the economy is sending somewhat mixed signals. Let’s summarize some of the crosscurrents.

Looking at the various components of gross domestic product, it appears that the underlying economy is still on an expansion track, and may even be accelerating a bit—a mixed blessing for stocks, which like economic growth but don’t like the inflation that often accompanies that growth. Our research contacts with a large number of companies in client portfolios tend to confirm that demand growth remains very much intact. Further, the rate of increase in wages has picked up, suggesting that consumer spending will continue to grow. Spending has been supported recently by a reduction in the personal savings rate in the U.S., which has declined from over 6% at the end of the financial crisis in 2010 to less than 2.5% at the end of last year. Consumption, therefore, will likely be more reliant on wage growth going forward.

The capital investment side of the economy is showing signs of life after a long period of relatively sluggish gains following the Great Recession. The prospect—and now the reality—of tax reform and deregulation seems to have given CEOs greater confidence in putting cash flow to work in new plants and equipment, and there are new tax incentives to do so.

Government spending, the other large component of the economy, may also pick up if infrastructure and defense measures are enacted as planned. Even without an acceleration in spending, the new tax legislation may act as a stimulus to the economy.

In addition to these signs of greater growth ahead, the weakening U.S. dollar may also add to inflation. Imported goods now cost more, providing room for prices on similar domestic items to be raised. In January, the Consumer Price Index rose 0.5% (somewhat more than forecast), and it has grown 2.1% over the last 12 months. Inflation in recent years had consistently fallen short of the Fed's 2% target, but it now appears to be nearing that target, giving the Fed cover to keep raising interest rates.

Moderating Factors

Offsetting these potentially inflationary forces are at least two moderating factors. First, productivity (defined as real output per hour worked) has accelerated recently and shows signs of continued improvement. In 2017, this vital Bureau of Labor Statistics indicator increased year over year by at least 1% in each quarter, its best showing in over two years. Some believe that the increased use of artificial intelligence in everyday applications is beginning to function as a kind of “next generation” of the industrial revolution. If labor market conditions tighten or even stay the same, many companies can be expected to devote increased attention to training their work forces and focus more capital spending on labor-saving devices, further driving productivity.

Second, labor force participation may start rising again, easing the upward pressure on wages. Over time, an economy can grow in real terms only as fast as the size of its labor force plus increases in productivity. Given the growth of the U.S. population and its age distribution, the labor force is estimated to grow at an annual rate of just 0.6% over the next eight years, according to the U.S. Bureau of Labor Statistics. This projection, however, assumes that participation, currently 63.0%, will continue its decline from its peak of 67.3%, reached in early 2000—a view that strikes many economists as overly conservative. If wages continue to improve at a time when unemployment is exceptionally low, the prospect of earning a paycheck may entice more people to enter the labor force. Additionally, there is ample evidence that most rising seniors are economically ill-prepared for retirement today, and many of them may need or choose to work beyond “normal” retirement age. Growth in the labor force could help offset inflationary forces and become a tailwind rather than a headwind for the economy.

We are not in the business of forecasting economic variables, but it appears that interest rates are likely to head upward for at least the next year or two. Deficits are rising in the U.S., and central banks around the world are shifting from quantitative easing to shrinking their balance sheets—albeit slowly—as the global economy emerges from a state of fragility to a more sustainable recovery.

The future course of interest rates is probably the greatest single concern for investors today, from both a fundamental and a valuation perspective. Rising rates eventually impact the cost of doing business in the corporate world, and given the enormous U.S. debt burden, higher interest expense will only add to the need for deficit spending. At the same time, it’s useful to remember that even a doubling of the yield on, say, the 10-year Treasury bond, would not cause it to reach the average yield seen in the 1990s. Viewed in that perspective, today’s slightly higher than average price/earnings ratios do not appear overly excessive. It must be recognized, though, that virtually all asset classes have been inflated by the long period of monetary easing, so we are careful not to overpay for individual securities.

In summary, we remain positive on the long-term outlook for equities. And the long term is what really matters, in our view. Short-term corrections may come and go, but in the end they are not the primary driver of returns. Still, it’s incumbent upon us to position client portfolios to endure periods of volatility like the present one. Favorable long-term returns are far more difficult to achieve if capital needs to be raised when prices are temporarily depressed. Without making a call on the near-term direction of the markets, we continue to stress the importance of maintaining liquidity and safety as a critical component of asset allocation. Diversification strategies, including exposure to non-U.S. developed markets, emerging markets, real estate, credit instruments and other private investments, also help to dampen overall portfolio volatility.*

A Role for Private Investments

Many of the world’s greatest fortunes have been created in assets whose values are not quoted daily or perhaps even at all—and therefore not subject to the kinds of price corrections that often rattle equity investors. Examples include energy, real estate, certain debt instruments, venture capital, leveraged buyouts, art and other illiquid assets. The lack of marketability typically means that prospective returns should be superior to comparable investments in the public markets—hence, the so-called illiquidity premium investors theoretically demand for owning a less-marketable asset. In fact, the inability to sell can be seen as an advantage of investing in these vehicles, as owners are forced to take a long-term view rather than succumbing to the emotional impact of short-term market movements.

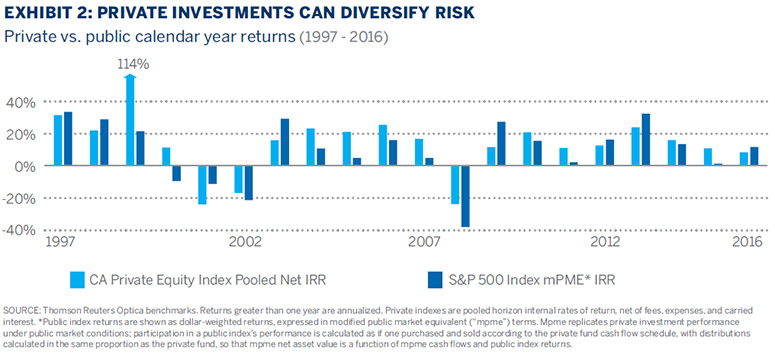

Partly for these reasons, we believe that private investments can play a useful role in portfolios if the client is comfortable giving up a degree of liquidity. What may not be as well-appreciated is that private investments can also be a source of diversification in a balanced portfolio. In some cases, this is a function of a particular partnership’s focus on certain subsectors of real estate, energy or other asset classes that behave differently from overall public market debt and equities. Private partnerships also have the ability to access specific investments or types of securities not typically accessible in the public markets. Exhibit 2 shows how the returns on private equity, as an example, have exhibited a surprisingly low correlation with those of public equities.

The process of marking the value of nontraded assets to “market” (an approximation at best) can cause returns to deviate from those of public securities. While most partnerships owning these assets revalue them each quarter, the lack of exact comparables on which to base changes in value makes this a challenging exercise. Moreover, in their desire to show steadier gains over time, many partnerships prefer to be conservative in valuing their assets until they experience a realization—and then the gains tend to be greater. And, of course, the timing of realizations may or may not coincide with public market peaks since transactions are usually done for strategic reasons rather than simply reacting to the vagaries of the markets. All of these factors caused the difference between public and private market returns to be especially pronounced in 2017.

None of this is to say that private investments are an easy way to avoid the effect of corrections in the market. Just because a private partnership interest isn’t quoted regularly doesn’t mean its value is immune to some degree of change. Their slowness to adjust does, however, remind us that short-term price movements in the public markets don’t necessarily represent a change in the most important thing: fundamentals. ![]()

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested.

The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client. It is not possible for an investor to invest directly into an index.

The S&P 500® Index represents the large-cap segment of the U.S. equity markets and consists of approximately 500 leading companies in leading industries of the U.S. economy. Criteria evaluated include market capitalization, financial viability, liquidity, public float, sector representation and corporate structure. An index constituent must also be considered a U.S. company. Standard & Poor’s, S&P®, and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a subsidiary of S&P Global Inc. The CBOE Volatility Index shows the market's expectation of 30-day volatility. It is constructed using the implied volatilities of a wide range of S&P 500 index options. This volatility is meant to be forward looking, is calculated from both calls and puts, and is a widely used measure of market risk, often referred to as the "investor fear gauge." Read more: VIX (CBOE Volatility Index): https://www.investopedia.com/terms/v/vix.asp#ixzz595cM5Po3. Investors Intelligence U.S. Advisors Sentiment Report: https://www.investorsintelligence.com/x/us_advisors_sentiment.html. The Cambridge Associates LLC US Private Equity Index is a horizon calculation based on data compiled from 1,421 US private equity funds (buyout, growth equity, private equity energy and subordinated capital funds), including fully liquidated partnerships, formed between 1986 and 2017.

*Alternative investments may only be available to Qualified Purchasers or Accredited Investors.