Some Wal-Mart stores sell rifles, some Starbucks coffee shops sell alcohol and GE builds engines for jet fighters and bombers. While generating just a small part of their revenues from these products, these companies pose a dilemma to investors who want to purge their portfolios of connections with guns, alcohol or the military. Should they set a ban on involvement or merely a low-level limit?

The dilemma underscores how investors building a sustainable portfolio need to clarify the precise objectives of any effort to screen out industries that they deem to be undesirable. Before even beginning to vet companies, investors need to recognize the limitations and weaknesses of the screens available. This may mean screening out some methods of screening.

A selective approach to filtering helps investors avoid supporting companies that they believe have an impact on society or the environment that is not aligned with their values. Screening can also help investors to better know what they own, or gain a richer understanding of the components in their portfolio. Indeed, many fiduciaries and charities feel a duty to use screening to identify and track any potentially controversial companies.

However, screening can exact a cost, so we help clarify for clients the potential impact on risk and return. The California Public Employees’ Retirement System (CalPERS) said in April that it missed out on as much as $3 billion in gains between 2001, when it started to sell its tobacco stocks, until the end of 2014, when it completed the divestment. CalPERS is the largest defined-benefit pension plan in the U.S., with more than $291 billion in assets.

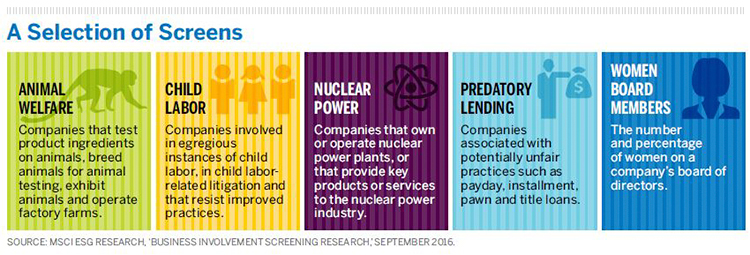

“Negative screening” is the most commonly used method among the many approaches to building a sustainable investment portfolio. By the end of 2014, institutional investors had invested more than $1.2 trillion using negative screening, according to US SIF Foundation, a Washington-based trade association promoting sustainable investing, of which Brown Advisory is a member. Screening can target myriad businesses beyond those already mentioned, including gambling, adult entertainment, nuclear power and faith-based concerns such as stem cell research.

The most common factor used in screening measures is the amount of revenue a company generates from a particular line of business. A cut-and-dried approach of zero tolerance is the simplest application of this method. Screening becomes more complex when investors are open to considering companies that generate revenue, up to a certain limit, from a line of business that they find undesirable. Screening grows especially complicated when an investor examines a company’s supply chain and related businesses.

Where There's Smoke

For example, an investor can easily determine the degree of their portfolio’s association with tobacco companies such as Altria, British American Tobacco or Phillip Morris. At first glance, the forbidden list would not include a company like Core-Mark Holdings, which distributes merchandise primarily to convenience stores in the U.S. Core-Mark, however, generates about 68% of its revenue distributing cigarettes and other tobacco products made by companies such as Philip Morris and R.J. Reynolds, according to MSCI, which provides data on companies’ environmental, social and governance (ESG) practices.

The same holds true with fossil fuel considerations. Investors can easily screen out oil, coal and other companies in the energy sector, but they may also want to exclude many chemical companies that own fossil fuel reserves but are not screened as fossil-based companies.

Investors can also gauge companies’ levels of carbon emissions, aiming to either identify those with high emissions or, through so-called positive screening, to find companies with a comparatively small carbon footprint. Investors should be aware that only 53 companies worldwide report 100% of their carbon emissions, according to a Bloomberg assessment of greenhouse gas emissions disclosure dated July 22, 2016. In addition, emissions reported by third parties are rough estimates, often based on a company’s industry and size. Such measures do not reflect the fact that companies within the same peer group can generate very different amounts of carbon dioxide.

In another example of positive screening, some 8,000 businesses have endorsed the U.N. Global Compact, which measures adherence to 10 internationally recognized principles for corporate behavior in human rights, treatment of workers, environmental stewardship and curbing corruption. ESG data providers such as MSCI apply these principles and grade companies as pass, fail or “on watch.” Investors can then use these broad measures for both positive and negative screening.

High Stakes

The filtering of companies involved in stem cell research and human cloning illustrates the nuance and ethical stakes that can come into play when building a sustainable portfolio. Some screening methods can be precise enough to rule out the use of stem cells from embryonic or fetal tissue but to not exclude companies engaged in research using adult stem cells.

The United States Conference of Catholic Bishops (USCCB) will not invest in companies engaged in human cloning and “in scientific research on human fetuses or embryos that 1) results in the end of pre-natal human life; 2) makes use of tissue derived from abortions or other life-ending activities; or 3) violates the dignity of a developing person.” The USCCB says new forms of research “will be evaluated on a caseby- case basis.”

MSCI screens out similar companies, along with businesses that produce technology that could be used in research involving human embryonic stem cells, fetal tissue or fetal cell lines. To date, MSCI has not identified any publicly traded companies engaged in human cloning.

In general, screening enables investors to know more about the companies they own and more closely monitor their holdings. This can be valuable for charities and foundations that want to ensure their holdings do not conflict with their mission.

One client we advise discovered from a screening exercise that 3.1% of its foundation’s portfolio was associated with fossil fuel reserves, weapons, tobacco and stem cell research—all of which contradicted the foundation’s objectives. Our clients determined that such a small percentage did not warrant immediate action but appreciated the deeper understanding of their foundation’s assets. Empowered by screening-based knowledge, the client and other investors can push forward with greater confidence in their long-term investment plans.

The views expressed are those of the authors and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. In addition, these views may not be relied upon as investment advice. The information provided in this material should not be considered a recommendation to buy or sell any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients or other clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients and is for informational purposes only. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication.

This communication and any accompanying documents are confidential and privileged. They are intended for the sole use of the addressee. Any accounting, business or tax advice contained in this communication, including attachments and enclosures, is not intended as a thorough, indepth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.