Fast Reading

- Health Care’s long-term outlook remains supported by durable tailwinds including an aging population, increasing clinical complexity, and ongoing innovation across the sector.

- Health Care’s 2025 performance was highly uneven, with early strength, a sharp mid-year selloff driven by policy uncertainty, and a late-year rebound as some overhangs began to ease.

- Biopharma and life science tools are deeply interconnected, making the health of biopharma research & development (R&D) spending a key driver for a large share of the broader Health Care sector.

- The team sees selective opportunities in pressured areas such as life science tools and managed care, where near-term challenges may be masking longer-term earnings power and recovery potential.

Looking Through the Noise in Health Care

Following a turbulent year for Health Care stocks, we believe Health Care’s long-term backdrop remains favorable despite recent volatility. In a live webinar, our panel of Health Care focused research analysts, Sung Park, CFA, Jay Kraska, CFA, and Jillian Reuter alongside moderator Emma Jewkes, outline this broad opportunity set.

Scope of Health Care Space

The Health Care sector currently makes up around 10% of the S&P 500® Index and can be broken down into five different subsectors: managed care, Health Care services, devices, life science tools and pharmaceuticals.

Within that, managed care and health insurers represent roughly 10% of the Health Care sector and are primarily responsible for managing the cost and delivery of care for large populations. Health Care services are also around 10% within Health Care and cover the diverse set of companies involved in the delivery of care and who support the day-to-day functioning of the health system, such as hospitals, laboratories and drug distributors.1

Medical devices, representing around 20% within Health Care, span the equipment and supplies that are primarily used by hospitals and health care providers, as well as the wearable Health Care devices used directly by consumers. Life sciences and tools represent the equipment and supplies used by research institutions and industry across the R&D process, encompassing another 10% of the overall sector. The remaining 50% is made up of biopharmaceuticals, the companies that research, manufacture, and commercialize drugs.2

These segments, particularly biopharma and life sciences and tools, are highly interconnected, driving demand for equipment and consumables purchases, as well as through R&D and clinical trial activity. That makes collectively 60% of the Health Care space that is dependent on the health of biopharma.3

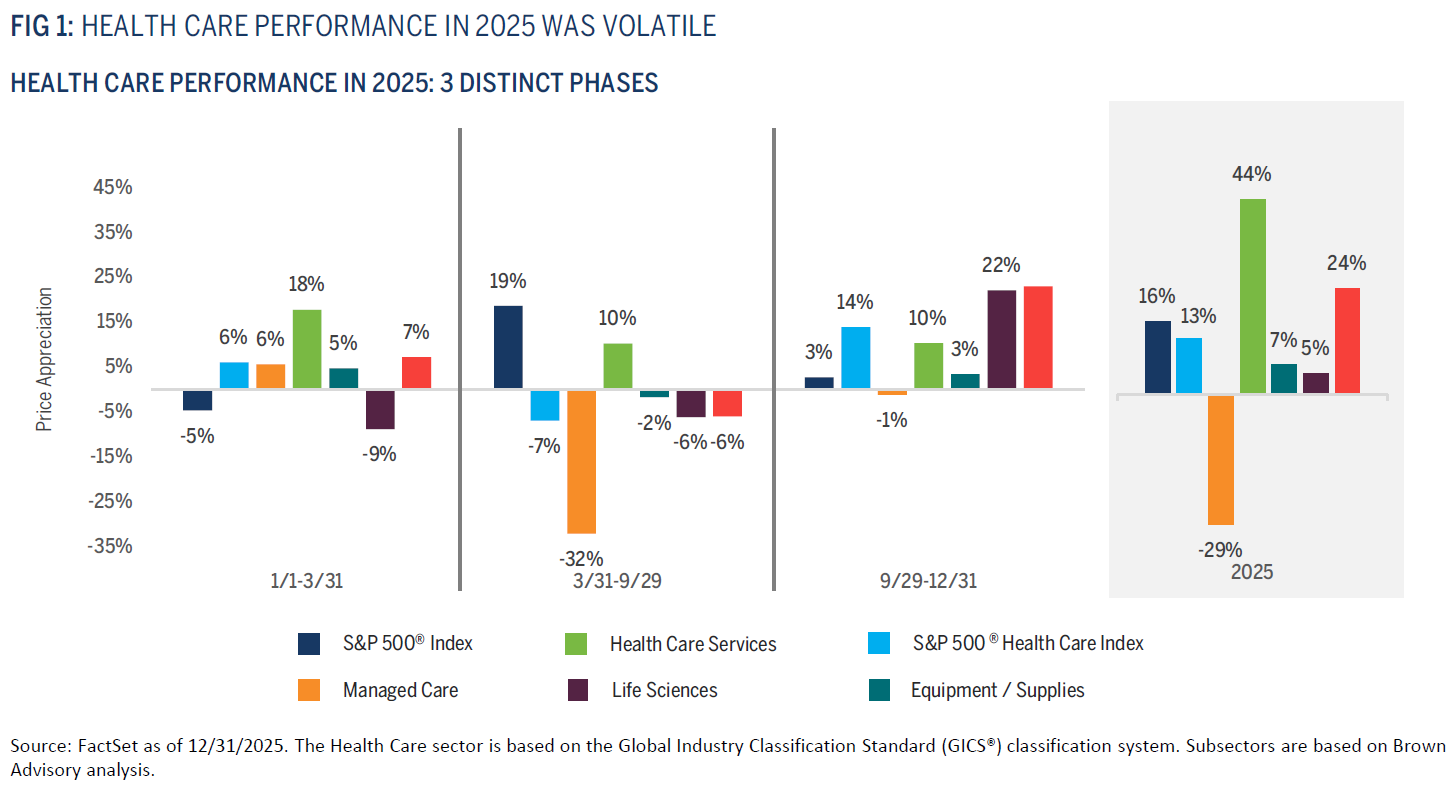

2025’s Rollercoaster Ride

The Health Care sector is supported by several structural, long-term tailwinds. However, this does not mean the sector is immune to periodic headwinds. The post-COVID-19 period has been a challenging time as the industry recovered from the COVID-19 vaccine testing boom/bust, a slowdown in biopharma spending, and reductions in government funding and policy changes. These challenges have meant that the traditionally non-cyclical sector has appeared highly cyclical, and 2025 was no exception.

At the start of 2025, investors rotated toward more defensive sectors like Health Care following two years of underperformance and more attractive valuations. This shift was also driven by increased caution amid uncertainty around the new political administration.

The second phase began in April with new tariff announcements and drug pricing rhetoric, which introduced significant uncertainty for the sector. As a result, biopharma and life sciences tools declined. Managed care stocks also declined as they faced increased margin pressure from a challenging underwriting cycle and elevated utilization. As a result, Health Care underperformed meaningfully during this period.

As policy overhangs eased late in the year, biopharma and life sciences rebounded strongly, driving Health Care outperformance in the final quarter. Overall, despite this volatility, Health Care finished 2025 slightly behind the broader market, returning 12.5% compared to 16.4% for the S&P 500® Index.4

Ultimately, we believe these headwinds have left sector valuations in an attractive position. It is not wise to try to determine the true bottom of the market, but a reset of earnings guidance and the aforementioned tailwinds mean we feel cautiously optimistic looking ahead.

Broad Spread of Opportunities For Growth

In our view, a series of positive macro and thematic drivers are generating strong tailwinds for the sector.

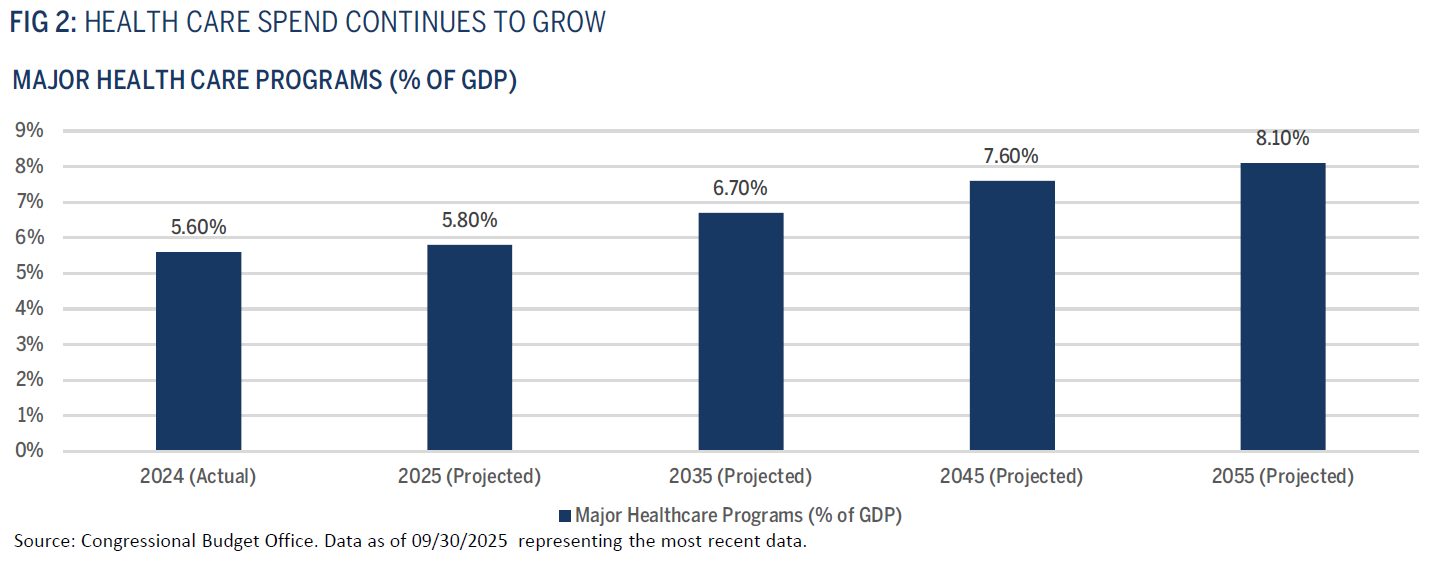

From a structural perspective, we believe Health Care is positioned to benefit from an increasingly aging global population, whose health needs will generally be more clinically complex. As a result, aggregate Health Care spending will need to grow faster than GDP. In the U.S., we believe the bulk of that spend will flow through health insurance systems, funded by employees, employers and the state, and these managed care providers will have to manage those costs effectively and efficiently.

We believe the sector’s ability to address this challenge will be underpinned by two key tenets: improving clinical outcomes and lowering costs through efficiencies. We are already witnessing an acceleration in the pace of innovation across biopharma, services, and devices. Moreover, developments in artificial intelligence (AI) are also driving developments in both clinical outcomes and improving efficiencies.

Drug discovery is a significant area of focus for AI. Only roughly around 20% of the world’s recognized diseases have FDA-approved treatments.5 With its ability to absorb and analyze huge data sets, we believe AI has the potential to transform drug development by improving the hit rate of drug development, narrowing down pipelines and identifying only the most optimal candidates for expensive lab trials.

AI also has the potential to unlock value from a patient perspective, in our view, by improving diagnostics and clinical decision-making. AI can analyze scans, translating them into standardized measurements and improving consistency among doctors, potentially enabling earlier disease detection and enhancing patient outcomes. AI could also integrate that scan information within broader patient records, considering prior lab results, imaging and medical history to support a more efficient and accurate diagnosis process. Health Care is a labor-intensive sector, and we believe it stands to benefit from AI-driven efficiency.

Risks Can Be Balanced By Defensive Qualities

Health Care has traditionally been viewed as a more defensive sector. Most Health Care spending is non-discretionary and predictable. Medicines need to be refilled, and many medical procedures cannot be deferred. Moreover, an upcoming cliff of patent expirations will have to be offset by pharmaceutical companies, placing greater emphasis on R&D expenditure or industry consolidation.

The launch of transformative drugs can also disrupt industry patterns. The enormous success of GLP-1 weight-loss drugs has created fears of downstream demand destruction within diabetes treatments, bariatric surgery and the treatment of other obesity-related conditions. While it is too early to fully determine whether GLP-1s will deliver lasting change in Health Care utilization, we can take assurance that successful prior drug releases, such as the positive impact of statins on cardiovascular outcomes, failed to dent the overall Health Care demand trajectory over time. Even so, as investors, we believe it is necessary to be vigilant in our monitoring of new developments and the associated implications across the rest of Health Care.

Similarly, the rapid emergence of new drugs from China is also generating concerns. China is certainly investing heavily in its biopharma program, and its drugs are seeing approvals and adoption in a number of overseas markets. In our view, innovation can come from many sources; therefore, multinational biopharma manufacturers need to be opportunistic in how they can partner with these competitors to best leverage each other’s relative strengths. We believe the rise in new treatments, wherever they are developed, can only serve to improve health outcomes and reduce costs for the broader world.

Collaborative Research Process

Macro and sector themes may be expanding the opportunity set for Health Care, but from an investment perspective, our approach is firmly based on stock selection. We do not make stock decisions based on macro themes alone. Instead, our bottom-up stock picking process evaluates every company on a case-by-case basis.

Health Care is a uniquely coordinated ecosystem where one player’s action can drive a reaction and a financial impact on others. Therefore, our research process is designed to provide a deep and detailed understanding of companies and Health Care systems, using both primary and secondary sources. In our view, a key strength of our approach is that no detail is too small. We will consider any data point, factor, strategy, or market condition that helps us to better understand the material challenges and opportunities facing individual businesses or the Health Care segment.

For instance, we conduct intense, holistic research into specific topics if we believe this will enable us to conduct more well-rounded analyses. We not only want to know how a business is performing today, but also what could reshape its opportunity and risk profile going forward as long-term investors.

One example of this is ethylene oxide (EtO), which is a carcinogenic gas. Each year, EtO is used to sterilize 20 billion medical devices, or 50% of all U.S. medical devices.6 While it is mission-critical to reduce the risk of infections for patients, concerns about EtO emissions are a potential source of evolving regulatory risk. As part of our analysis, we evaluated how companies are innovating to minimize these emissions, mitigate potential litigation exposure, and strengthen partnerships with key regulators. This analysis also allowed us to roughly project the magnitude of future potential regulatory costs relative to topline growth.

As a team, while we have our individual areas of specialization, we do not operate in silos. We continually conduct iterative conversations to challenge assumptions. This collaborative sounding board is underpinned by one common goal: to identify the best stocks that will hopefully drive outperformance and deliver the best outcomes for our clients.

An Optimistic Path Forward

We believe the Health Care sector offers an attractive combination of defensive characteristics that are supported by predictable long-term growth drivers. This is further supplemented by innovation that can create pockets of secular upside.

Despite a challenging period for the industry, we believe these recently overlooked businesses have made material progress. In our view, the valuations for Health Care stocks sit at historically attractive levels.

As long-term investors, we feel optimistic about the path forward for Health Care stocks.

U.S. Institutional Sales & Service (443) 873-5252 [email protected]

International Institutional Sales +44 (0) 20-3301-8130 [email protected]

1 Source: FactSet, as of 12/31/2025.

2 Source: FactSet, as of 12/31/2025.

3 Source: FactSet, as of 12/31/2025.

4 Source: FactSet, as of 12/31/2025.

5 Source: Every Cure, as of 2025; The Problem - Every Cure.

6 Source: United States Environmental Protection Agency, as of 03/31/2026; Ethylene Oxide (EtO) | US EPA.

Past performance is not a guarantee of future performance and you may not get back the amount invested.

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

FactSet® is a registered trademark of FactSet Research Systems, Inc.

All investments involve risk. The value of the investment and the income from it will vary. There is no guarantee that the initial investment will be returned.

Global Industry Classification Standard (GICS®) and “GICS” are service makers/trademarks of MSCI and Standard & Poor’s. FactSet® is a registered trademark of FactSet Research Systems, Inc. APX® is a trademark of Advent Software Systems.

The S&P 500 Index is a capitalization-weighted index of 500 stocks that is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. Index returns assume reinvestment of dividends and do not reflect any fees or expenses. An investor cannot invest directly into an index. Benchmark returns are not covered by the report of the independent verifiers. Standard & Poor’s, S&P®, and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a subsidiary of S&P Global Inc.

The S&P 500® Health Care Index comprises those companies included in the S&P 500 that are classified as members of the GICS® health care sector.