When we ask ourselves whether a company is a good investment, we are really asking ourselves a multitude of apparently simple yet complex questions: is this a good business, is it run by excellent operators and is it available to us at an attractive valuation? Focusing for a moment on the question of valuation: it is an obvious point but, as investors, we make money when there is a mismatch between price paid and intrinsic value. The Sustainable International Leaders strategy values a company based on a fundamental in-depth understanding of its key business drivers.

Our framework for valuing businesses

We believe that a robust foundation for valuation can protect us against the costly mistake of overpaying for even the most outstanding business. It can also point us to the most compelling opportunities for potential returns, all other things being equal.

I was first introduced to the work of John Burr Williams during my time at Columbia Business School’s Value Investing program. He laid the groundwork for modern valuation techniques in his 1938 text The Theory of Investment Value. Contrary to the valuation theories prevalent at the time, he argued that the intrinsic value of a company is the present value of all future income. In doing so, he recognized the importance of cash flows and discount rates, two key inputs into valuing any financial instrument. While his ideas have been expanded upon over time, these core concepts have revolutionized the way investors think about the value of securities.

Our work on valuation focuses on the long-term view, which is aligned with our investment horizon. Over a holding period of five-plus years, we believe the value of a business is tethered to the cash flows that it generates1. We aim to assess the true worth or intrinsic value of a business by analyzing its growth prospects, competitive position, and financial health. We want to get as accurate a picture of a business as we can with conservative, yet realistic assumptions on revenue growth, margins, and free cash flows (FCF). To bring the value of future cash flows into today’s terms, we need to estimate the right cost of capital. It’s not about the flavor of the month but rather the long-term cost of capital that can be defended in a variety of different macroeconomic environments. Our goal is to be roughly right rather than to seek false precision.

Sustainable International Leaders employs a discounted-cash-flow based valuation approach over a 10-year time horizon and a standardized weighted average cost of capital or WACC of 10% for developed markets and a higher rate for developing markets to compute the intrinsic value of a business. Our assumptions for cost of capital are based on our best long-term estimates keeping in mind historical long-term interest rates and equity returns.

In order to compete effectively against the benchmarks that reside on the other side of the net, our research team is able to play to its strengths and aim well inside the lines by investing in quality companies, maintaining a multi-year time horizon, and constructing concentrated portfolios that only contain our highest conviction ideas. All the while, it is essential to carry an awareness of the macro, as it establishes the conditions in which we compete. After all, I might adjust my strategy against Pierre’s hard-hitting students depending on wind direction, sun placement, and surface.

Combining all these elements, we can work out the implied FCF multiple2 at which a company should trade over the next five years. Our expected returns are the sum of (i) the price we pay (the 1-year forward FCF yield), (ii) the long-term expected FCF growth, and (iii) what we call ‘multiple compression’ (that’s basically the change in how much investors are willing to pay for that business over time). Whilst by no means perfect, this framework allows us to maintain a disciplined approach to valuing businesses, helping us steer clear of narratives and focus on the fundamentals.

Where our approach works best

When assessing a business, we not only employ a robust framework for valuation but also critically evaluate whether the nature of the business is such that we can ascertain its valuation with a high degree of confidence. Our most accurate assessments of valuation have been in relatively mature industries with well-defined competitive advantages. The majority of the portfolio would be invested in these enduring types of businesses, ranging from financial markets infrastructure companies such as London Stock Exchange and Deutsche Boerse, consumer franchises such as luxury conglomerate LVMH and the leading global alcoholic beverages company Diageo, business services companies like Wolters Kluwer, Rentokil and Compass Group and industrials such as Swedish industrial compressor maker Atlas Copco and Swiss specialty chemicals business Sika. The inherent predictability in these business models provides a solid foundation for assessing valuations over a five-to-ten-year timeframe.

Is the US equity market therefore overvalued? Not necessarily. Beyond the discount rate, one should consider both return on equity (ROE) and the expected earnings per share (EPS) growth rate of the S&P 500 Index, factors that are positively correlated with P/E. If ROE and EPS growth are accelerating they can offset the higher discount rate, supporting a higher market valuation.

On the other side of the spectrum, certain sectors are marked by rapid change and unpredictability, making the task of valuation significantly more challenging. In dynamic industries - where technology evolves at breakneck speed and consumer preferences shift like sand dunes - the future is less a clear horizon and more a mirage that constantly shifts and reshapes. Attempting to peg down a firm valuation in such fluid conditions often feels like trying to nail jelly to the wall, and the risk of miscalculation is high. Early-stage companies exemplify this valuation conundrum. Take the example of the e-commerce platform provider Shopify, a former portfolio holding where we believe our initial estimate of valuation was inaccurate. In general, the value is harder to pin down because their economic moats may not be fully formed or tested. With a future that hinges on a multitude of variables, from market adoption to regulatory changes, their growth and profitability trajectories can vary wildly. Industry evolution can dramatically alter the landscape in which these companies operate, rendering early valuations potentially obsolete as the business matures. In such cases, we proceed with caution, recognizing our limited ability to have a high degree of confidence in our valuations.

Valuation discipline

Before getting into details of what we do, I thought I should mention what we don’t do. We view ourselves as investors – not speculators – and do not subscribe to the greater fool theory of valuation3. Furthermore, we don’t fixate on near-term valuation metrics that can make companies look optically cheap or expensive on a very short time frame. In our view, this would not lead to optimal decision-making over a longer time period.

Our first step, as with every aspect of investing, is always to consider the downside — while higher expected returns are enticing, they often come hand-in-hand with greater uncertainty around valuation and ultimately, greater risk of permanent loss of capital. Our experience with businesses that have tenuous competitive positions or operate in rapidly changing business environments makes us wary of veering into areas where we do not have strong confidence in our estimate of intrinsic value.

Instead, we are on the lookout for opportunities where higher expected returns are due to temporary market concerns, such as economic cycles, which may present us with favorable investment prospects. This particular headwind has been a source of opportunity for us when we made our investments in the Indian IT services provider Tata Consultancy Services, UK alcoholic beverages company Diageo and Japanese bicycle component maker Shimano. In these well-run businesses with a long runway for compounding free cash flows, we have been happy to make the trade-off between near-term economic uncertainty and long-term durability of attractive cash flows. As an example, we recently invested in Diageo when near-term macroeconomic headwinds and persistent post-Covid supply chain challenges coincided with a new incoming CEO to create a buying opportunity. We view these concerns as temporary. Diageo owns a portfolio of best-in-class brands such as Johnnie Walker, Guinness and Don Julio and has an unparalleled distribution network globally. We expect the company to grow topline ahead of the market and gain share in its key categories and markets, which when combined with its high incremental returns and strong cash flow generation will lead to attractive returns for investors over the foreseeable future.

The biggest question to be answered as we enter yet another earnings season is whether current expectations for massive EPS growth acceleration for the next several quarters can hold. Our research team will continue to observe these broader trends while focusing on long-term high-quality company fundamentals in an effort to play to our strengths and aim well inside the lines. As for my tennis game, my goals are somewhat less ambitious – if I make it through the upcoming season without injury, it’s a win!

In other cases, near-term shorthand multiples can be misleading in the case of exceptional businesses that continue to improve over time. This has been the case for Dutch information solutions provider Wolters Kluwer which has consistently accelerated its organic growth over a long period of time or for Waste Connections, where value accretive bolt-on M&A has allowed the company to grow its cash flows in the teens over the last decade in a relative low growth, mature North American solid waste industry. The market may not be willing to give credit to Wolters’ accelerated organic growth or to Waste’s savvy M&A strategy and hence, these companies always look optically expensive. These successes, however, don’t guarantee permanence and we follow them closely to assess whether our valuation work and position sizing continues to be backed up by sound analysis.

Our objective is to own excellent businesses that have the potential to increase their intrinsic value on average by 10% annually. While we are willing to live with valuations at the higher end of our estimates for businesses that are executing well on our investment thesis, we will not hesitate to sell on valuation if required. For instance, we parted ways with businesses such as Japanese cosmetics manufacturer Shiseido and the Tokyo Disneyland parks operator Oriental Land when their prices seemed to anticipate perfect execution. Typically, stocks with loftier valuations carry a smaller weight in the portfolio to mitigate exposure to the risk of overvaluation.

Putting it all together

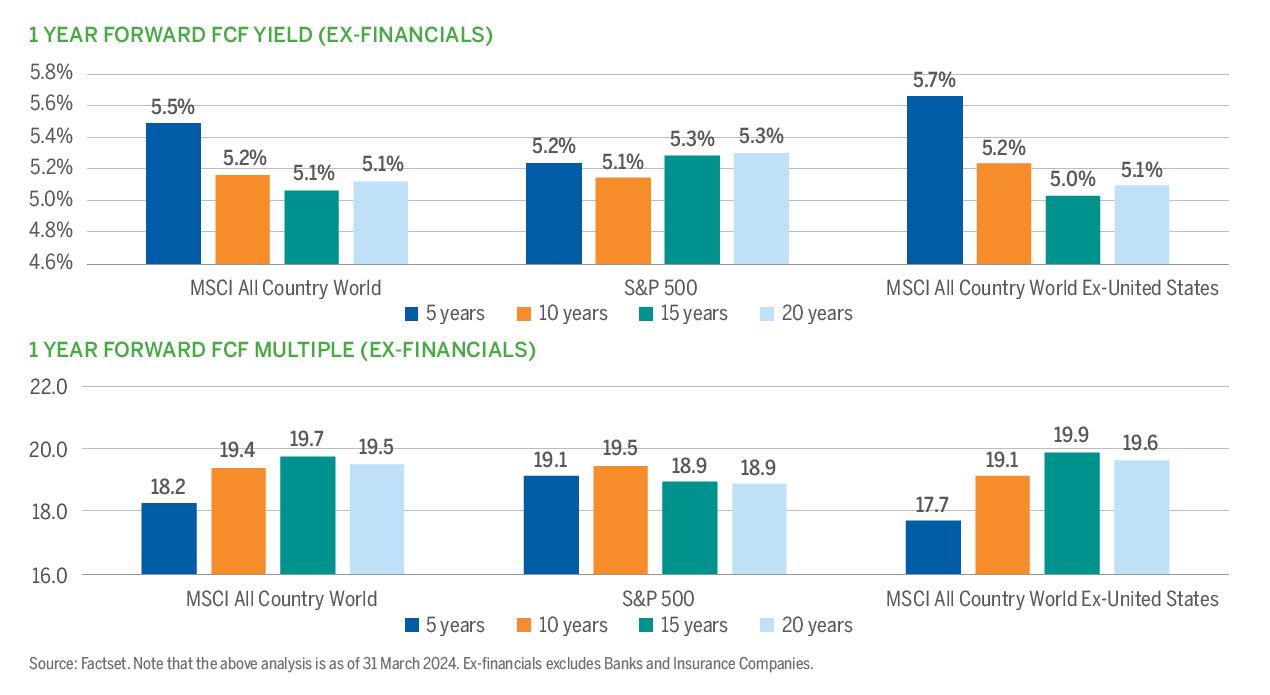

We expect our portfolio to generate a FCF CAGR of 11% (excluding banks and insurance companies4) over the medium term. With a starting one-year forward free cash flow yield of 4% and considering a 33% contraction in valuation multiples – from ~25x to ~16.7x5 – we aim for at least a double digit expected return. We believe that our assumptions6 err on the side of caution – even beyond our explicit forecast period, it is not unfathomable for our companies to remain competitively advantaged and to continue to compound their cash flows in the high single digit range. In that scenario, a free cash flow yield of 6% would prove conservative, in light of the long-term valuations of the average company listed in the stock market (please refer to the charts below).

In summary, there are three key aspects that influence our valuation methodology:

- Free cash flow based valuation: Long-term cash flow based analysis to determine a company’s intrinsic value, focusing on its financial health and market position.

- Structured approach: Disciplined framework with realistic assumptions on financial metrics and a standardized cost of capital to calculate intrinsic value.

- Long-term focus: Less attention to short-term metrics and more to long term drivers of value creation.

- Benjamin Graham famously said, “In the short run, the market is a voting machine, but in the long run, it is a weighing machine.” – Berkshire 1987 letter: https://www.berkshirehathaway.com/letters/1987.html

- We refer here to the unlevered 1-year forward free cash flow multiple for the enterprise.

- This is a social theory that rests of the belief that one can make money on an overpriced asset by selling it to someone else at a higher price – this buyer is referred to as the “greater fool”.

- This excludes AIA, HDFC Bank and Bank Rakyat which typically range between 10-12% of the portfolio. We estimate that these three businesses will grow earnings and book value at a 10%+ rate annually.

- Note that 6% 1-year free cash flow yield equates to a 1-year forward free cash flow multiple of 17x. A multiple compression from 25x to 16.7x equates to a change in FCF yield from 4% to 6% over five years.

- This analysis assumes that portfolio weights, including cash, remains unchanged over time.

Disclosures

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions.

The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

All investments involve risk. The value of the investment and the income from it will vary. There is no guarantee that the initial investment will be returned.

Sustainable investment considerations are one of multiple informational inputs into the investment process, alongside data on traditional financial factors, and so are not the sole driver of decision-making. Sustainable investment analysis may not be performed for every holding in the strategy. Sustainable investment considerations that are material will vary by investment style, sector/industry, market trends and client objectives. The Strategy seeks to identify companies that it believes may be desirable based on our analysis of sustainable investment related risks and opportunities, but investors may differ in their views. As a result, the Strategy may invest in companies that do not reflect the beliefs and values of any particular investor. The Strategy may also invest in companies that would otherwise be excluded from other funds that focus on sustainable investment risks. Security selection will be impacted by the combined focus on sustainable investment research assessments and fundamental research assessments including the return forecasts. The Strategy incorporates data from third parties in its research process but does not make investment decisions based on third-party data alone.

Terms and Definitions:

Free Cash Flow (FCF) yieldis a measure of financial performance calculated as operating cash flow minus capital expenditures. FCF yield calculations presented use the median NTM (Next Twelve Months) and exclude Banks and Insurance companies.

Free Cash Flow (FCF)is a measure of financial performance calculated as operating cash flow minus capital expenditures. Free cash flow (FCF) represents the cash that a company is able to generate after laying out the money required to maintain or expand its asset base. Free cash flow is important because it allows a company to pursue opportunities that enhance shareholder value. Without cash, it’s tough to develop new products, make acquisitions, pay dividends and reduce debt.

Free Cash Flow (FCF) multiple is a ratio between a company’s equity value and free cash flow.