Fast Reading

- Asset protection planning is most effective when approached proactively and in layers, combining insurance, asset titling, and structures, such as entities and trusts, to reduce exposure and preserve flexibility before a claim arises.

- Liability can emerge from multiple sources, including personal, professional, contractual, family, property, tax, and digital risks. Relying on any single strategy can leave families exposed to unintended gaps.

- Effective asset protection is about protecting optionality rather than chasing perfection, with early planning and regular updates helping families maintain resilience as assets, responsibilities, and external risks evolve.

Risk tends to arrive quietly and emerge unbidden in unpredictable ways: a visitor has an accident on your property; a teenage driver makes one mistake; a business dispute escalates into litigation; a divorce proceeding’s scope broadens to include legacy assets in determining a financial settlement; a storm damages a home or a boat; a board role brings unexpected scrutiny; and increasingly, digital life creates openings for identity theft and cyber-enabled fraud.

Asset protection planning is how we bring structure to that uncertainty. Not by chasing worst-case scenarios or trying to “solve” risk once and for all, but by building resilience through a coordinated set of choices around insurance, ownership, and asset holding structures. In other words: thoughtful preparation that helps keep you in a strong negotiating position if a claim ever arises.

The core truth: there is no silver bullet in asset protection. The objective is to reduce exposure and increase options before you need them.

What follows is a practical framework we use to help clients translate complexity into clarity and turn “vague worry” into actionable plans.

Name the Risks Without Letting Them Run the Show

Every asset protection conversation starts the same way: what are the realistic ways a third party could make a claim against you or against something you own?

For most families, exposure clusters into a few familiar categories:

- Contractual disputes: business arrangements, lending relationships, partnership fallouts, employment matters.

- Property risk: hurricanes, floods, wildfire, theft, and damage to valuables like art and jewelry.

- Family risk: marital claims in separation and divorce, especially when inheritances and family gifts are involved.

- Digital risk: cyber intrusion and identity theft that can create direct loss or require a long, expensive unwind.

- Tax & regulatory risk (often overlooked in “asset protection” conversations): unpaid tax liabilities can trigger scrutiny from tax authorities (e.g., IRS collection activity, including liens and levies); and regulatory investigations can create parallel exposure.

- Personal liability (tort claims): injuries on property, auto accidents, defamation/libel, wrongful death claims, or allegations tied to volunteer and board service.

- Professional exposure: malpractice or other profession-based claims (often heightened in medicine, law, finance, and governance roles).

When we understand the shape of the risk, we can match it with the right tools, without adding complexity and cost where it won’t matter.

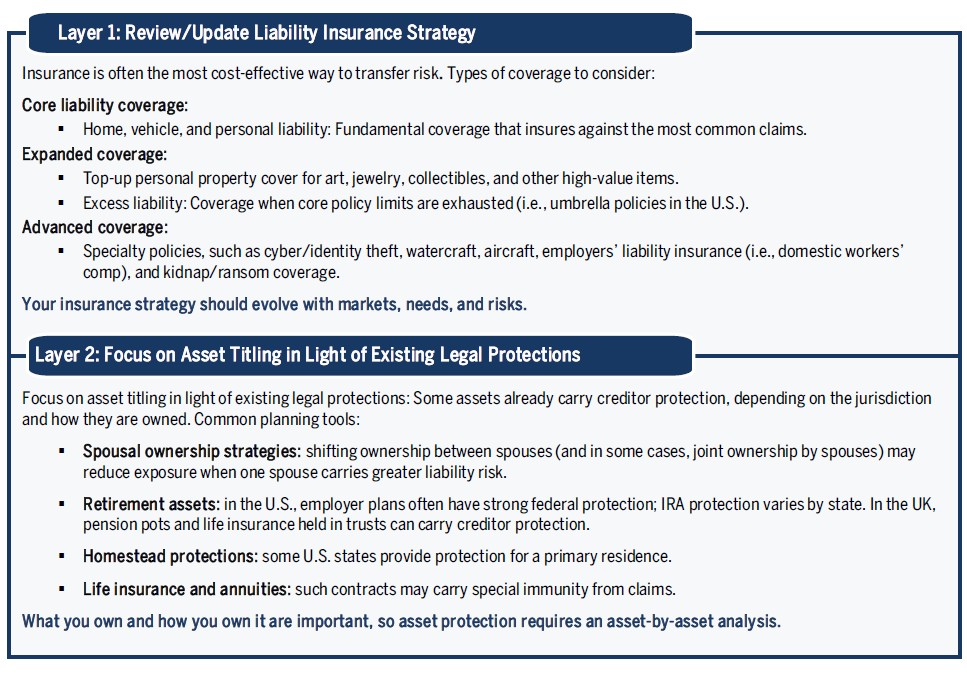

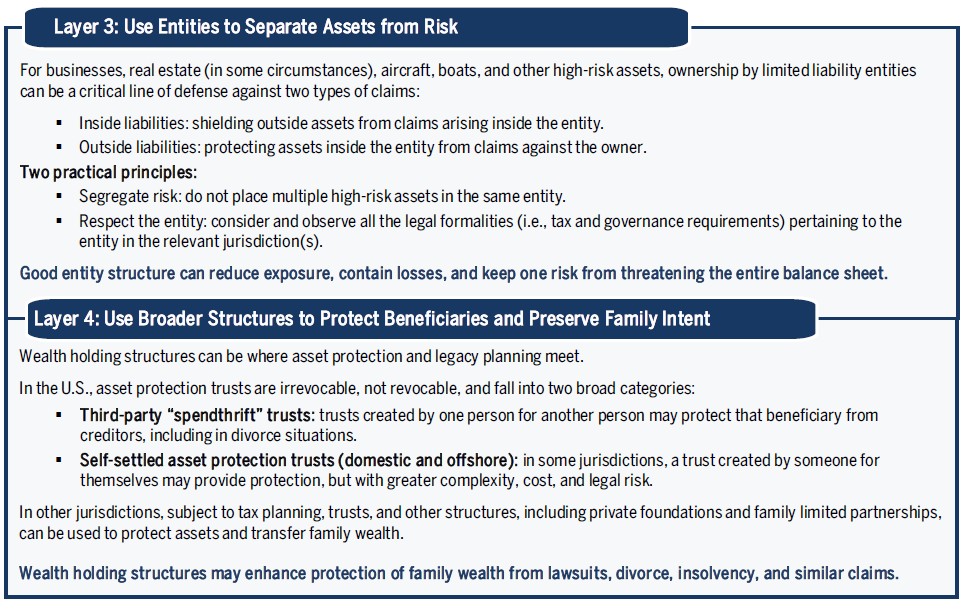

Think in Layers, Not Products

The most durable asset protection plans aren’t built on one strategy. They’re built on layers, with each doing a specific job and each reinforcing the others. The following details the layers we think are most critical:

The Principles That Keep Asset Protection Planning Effective

The best plans are the ones that families can maintain, understand, and update. A few maxims we return to:

Don’t exaggerate the risk. Over-engineering can create expense, friction, and unintended tax outcomes.

Insure where you can. Insurance is often the simplest and most efficient way to mitigate risk.

Don’t ignore fiscal obligations. Transfers between individuals, entities, and trusts can trigger taxes and/or filings in relevant jurisdictions. In the U.S., transfers to trusts can trigger gift/GST reporting (Form 709), trust administration can trigger fiduciary income tax filing (Form 1041), and foreign trust activity can trigger Forms 3520/3520-A, with penalties for noncompliance. In the UK, trust creation, transfers, and administration may give rise to inheritance tax, capital gains tax, and income tax consequences, as well as trust registration and reporting obligations.

Keep it current. Risks change as families buy homes, start businesses, add board roles, hire employees, and see children become adults, while technology, geopolitics, regulation, and other external forces continue to shift the broader landscape.

Plan early. Many strategies are strongest when implemented well before any specific threat is on the horizon.

A Practical “Asset Protection Check-In” for the Year Ahead

If you want a simple way to start (or refresh) the conversation, these questions help surface the most common opportunities:

- Have we reviewed liability limits in the last 12–18 months?

- Do home/vehicle policies match today’s replacement costs and real-world usage?

- Are high-risk assets (rental properties, boats, aircraft) held appropriately?

- Are entities being administered properly, including banking, contracts, records, and insurance alignment?

- Are inheritances and family gifts structured to optimize protection in divorce scenarios?

- Are retirement and exempt assets coordinated with the broader balance sheet?

- Do we have specialty coverage for valuables, cyber risk, and domestic employees where relevant?

- If you are a director of a nonprofit or for-profit organization, have you reviewed the policies and coverages carried by the organization?

- If a claim arose tomorrow, do we know who would do what, including your lawyer, insurer, accountant, and advisor?

Closing Thought: Protect Optionality, Not Perfection

Asset protection is rarely about winning in court. It’s about reducing the likelihood of a devastating outcome, improving your negotiating posture and preserving the flexibility to keep living your life without letting risk dictate every decision.

In our experience, the most confident families aren’t the ones who believe they’ve eliminated risk. They’re the ones who’ve built a coherent system that is layered, coordinated and regularly revisited, so that if the unexpected happens, they’re prepared. That discipline is especially important today, as technological innovation, geopolitical uncertainty, regulatory shifts, and other evolving risks continue to reshape the landscape. In that kind of environment, asset protection is not static; it requires ongoing attention to ensure your strategy remains aligned with both your circumstances and the world around you.

As always, the Strategic Advisory team is here to talk through this complex issue and help make sense of the most effective way to plan given your specific circumstances. If you have questions, do not hesitate to contact us. ![]()

The views expressed are those of Brown Advisory as of the date referenced and are subject to change at any time. This material is provided for informational purposes only and is not individually tailored to, or directed at, any particular client or prospective client.

Any accounting, business or tax discussion contained in this communication is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties. Brown Advisory does not render legal or tax advice. Prior to making an investment decision, a prospective investor should consult with their own legal, tax, accounting, and other advisors to determine the potential benefits, burdens, and other consequences of such investment.