Only Time Will Tell

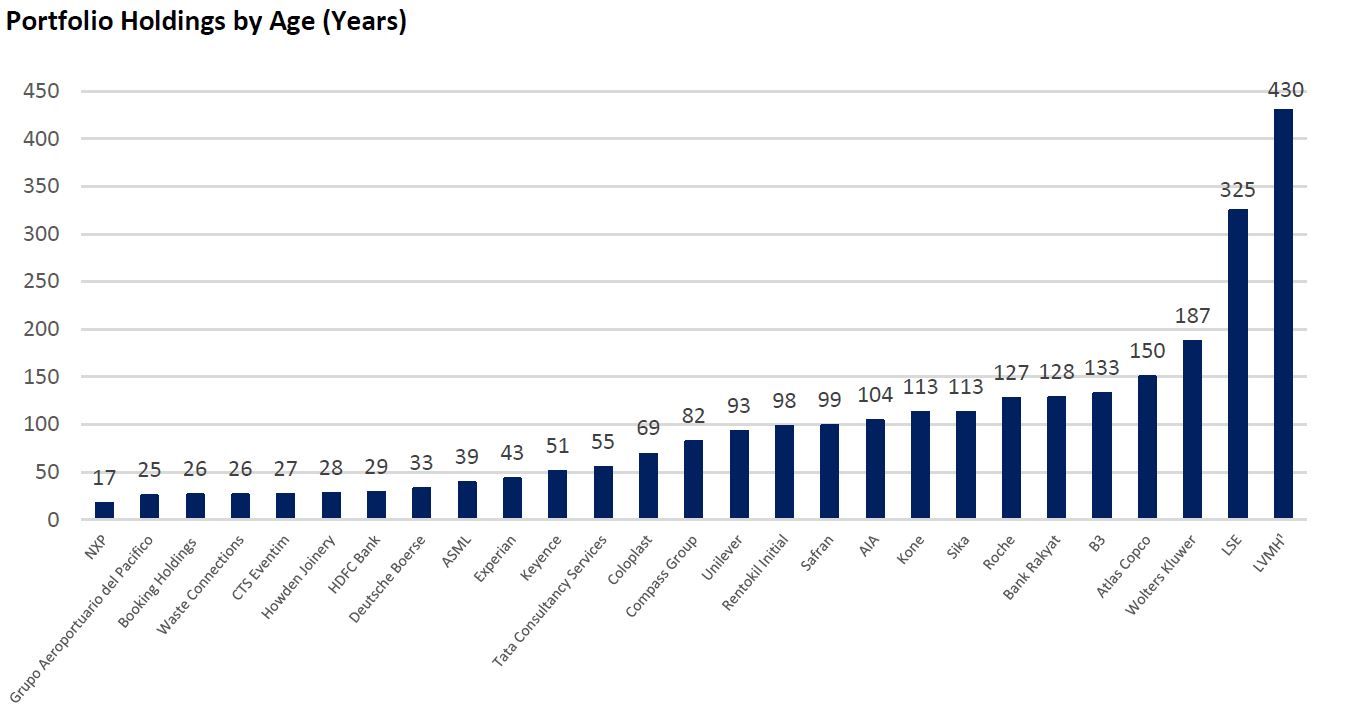

While the old adage “only time will tell” generally refers to a future outcome, it reflects our belief that a truly enduring investment must have proven to be resilient under a variety of macroeconomic circumstances. The Sustainable International Leaders (SIL) strategy views resilience as a crucial lens through which to analyze businesses and seeks to invest in companies that have withstood the test of time. Consequently, the median age of the portfolio is 69 years. The youngest company we own, Dutch semiconductor company NXP, is only 17 years old, while French luxury goods firm LVMH is by far the oldest, having incorporated at the end of the 16th Century (Figure 1).

Figure 1. Time is the ultimate measure of resilience: Over 95% of Sustainable International Leaders’ holdings have been in business for at least 25 years.

Source: FactSet as of 08/31/2023. 1Chateau d’Yquem is part of LVMH and was founded in 1593. Portfolio information is based on a representative Sustainable International Leaders account. Please see the end for important disclosures.

A fundamental premise of any business is that the company in question will be operational well into the future. But just how far into the future is where we pay close attention. Portfolio holdings such as Swiss pharma and diagnostic giant Roche Holding, Finnish elevator engineering company Kone, French luxury conglomerate LVMH, and Swedish industrial compressor company Atlas Copco are businesses where the founding families are still involved in the business, and that operate on a multi-generational timeframe, far beyond the investment horizon of most investors. We believe this is what allows them to create enduring businesses with sustainable competitive advantages and attractive capital deployment opportunities. All but one of Sustainable International Leaders’ holdings have been around for at least 25 years. This means that an overwhelming majority have withstood the early 2000s recession in developed markets, the 2008 to 2009 Global Financial Crisis, and the Covid-19 global pandemic. Indeed, these businesses have not only survived such events, but in most cases have emerged stronger and thrived in the period that followed, all while building and improving their competitive position.

The concept of gauging a business’ resilience largely by how long it has already been in existence might seem odd in an era when newer companies with more contemporary business models and product ideas often garner more investor attention than the overgrown dinosaur companies of yesteryear. However, in our view, it is the companies that have persevered through a multitude of cycles —market, business, geopolitical to name a few — that are more likely to exist in the years and decades ahead. This concept has been formalized through what is known as The Lindy Effect.1 In short, the theory holds that the future life expectancy of certain non-perishable phenomenon like a technology or an idea is proportional to their current age. Thus, every additional period of survival implies a longer remaining life expectancy.

Identifying Resilience

Our portfolio holdings’ resilience comes from several sources: the durability of their competitive advantages, structural growth tailwinds, and a history of strong execution. Additionally, we have found these businesses to face low risk of permanent loss of capital caused by excessive leverage, obsolescence, or exposure to significant risks and hidden liabilities. Our investments are not immune to macroeconomic fluctuations; we nonetheless think they have unique qualities that should help them outperform their peers over time.

Even when the best company fundamentals are combined with the most capable management teams, the success of such companies can be highly dependent upon industry structure. Thus, we place a strong emphasis on competitive positioning of companies within their sector.

In financial services, for example, we have steered clear of large, commoditized banks and instead sought to invest in companies that we believe have a differentiated positioning that is hard to replicate and which also benefit from secular tailwinds toward new financial market penetration, such as Hong Kong-based general insurance services company AIA Group, Ltd, Indonesian microlender Bank Rakyat, and India’s HDFC Bank.

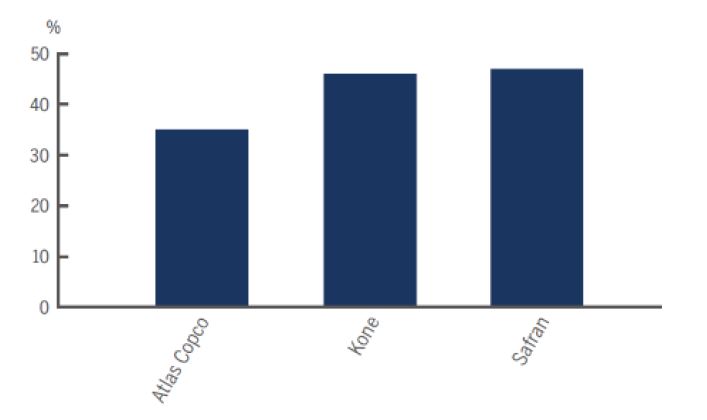

In the industrials space, we have refrained from investing in deeply cyclical commoditized businesses and see resilience in companies that typically benefit from a meaningful after-market component or subscription-like revenues from maintenance or service contracts, e.g. Atlas, French Aerospace manufacturer Safran Group, and Kone (Figure 2.) Others such as U.S. waste services company Waste Connections and British pest-control firm Rentokil Initial are traditionally defensive businesses that benefit from local economies of scale in distribution, which can be incredibly hard for smaller players to compete with.

With resilience as a key principle guiding Sustainable International Leaders’ portfolio construction, our focus inherently points toward high quality, free-cash-flow generative companies that we believe have strong potential to generate attractive throughout the cycle risk-adjusted returns.

Figure 2. Selling past the sale: cash flows from equipment servicing contracts

Original equipment revenues vs aftermarket revenues

Source: Company reports. Data as of 2021 and is most recent data available.

In the technology sector — which is a double-edged sword of huge capacity for innovation along with huge potential for disruption — our areas of focus are competitively advantaged businesses within consolidated, rational industries. While the semiconductor business has seen violent cycles in the past, the industry is more consolidated today and benefits from strong cyclical upturn with digitalization of the economy. We are able to gain exposure to companies with strong competitive positions in this sector via holdings such as Dutch semiconductor supplier ASML Holdings, and Dutch semiconductor manufacturer NXP Semiconductors. Other stocks we own in this space include providers of mission-critical solutions such as Wolters Kluwer, a Dutch provider of information solutions for professionals such as health care practitioners, lawyers and accountants that they would typically be loath to cut down on even in a downturn and Indian IT services provider Tata Consultancy Services, which derives a significant proportion of revenues from less discretionary maintenance spend by its customers.

Finally, our holdings in the consumer discretionary sector include businesses that have a history of not only rebounding quickly, such as the luxury conglomerate LVMH, online travel agent Booking.com, and Compass, Inc. While these businesses can be impacted by short-term cyclical headwinds from time to time, we think their long-term prospects remain attractive.

Navigating Macro Uncertainty via a Bottom-Up Approach

Looking beyond sector dynamics, another key source of resilience across our holdings is their ability to withstand the prevailing macro environment, especially the ongoing inflationary cycle and supply chain challenges. Indeed, while some portfolio holdings are managing well, others are able to capitalize and even benefit in the current environment.

Due to a combination of strong structural growth tailwinds in their sectors and supply chain shortages, our semiconductor holdings such as ASML and NXP are benefitting from strong pricing power, versus the price deflation that we have historically seen in this sector. Meanwhile, Deutsche Boerse has benefitted from strong cyclical growth across their asset classes and the impact from inflation has been limited: revenues grew 18% in H1 23 vs operating costs up 10%. Despite inflation, they continue to manage the cost base well on the back of strong cyclical and secular top line growth.2 Others that have been able to pass on inflation or have even benefitted from it include luxury conglomerate LVMH, outsourced food services provider Compass, pest control business Rentokil, and information solutions company Wolters Kluwer, which have all been able to fully offset the impact of inflation. At the same time, we believe it is reassuring to see that pricing actions have been taken with integrity and none of these companies mentioned here are looking to exploit what is no doubt a tough operating environment for their customers.

Others have been able to largely absorb the immediate impact of inflation and have only seen modest margin compression, such as British consumer goods producer Unilever, Atlas Copco and Kone. Over time, we think these companies should be able to more than offset inflation through mix-driven innovation in the case of Unilever and Atlas or improved pricing in the aftermarket for Kone.

Today’s Environment is an Attractive Entry Point for Long- Term Investors

The soundness of our investment strategy is not predicated on a narrow range of projections of the future. We believe that these businesses represent good long-term sustainable investments, but the current market environment of global uncertainty offers an attractive entry point. Going forward, we see meaningful long-term potential and attractive portfolio characteristics that are reflected in 20.0% ROIC, 7.11% three-year sales growth and a 4.2% free-cash-flow yield as of August 31, 2023.3

1 article in The New Republic. The idea has since been refined more quantitatively, first by Benoit Mandelbrot in his 1982 book, The Fractal Geometry, and more recently by Nassim Nicolas Taleb in his 2007 book, The Black Swan: The Impact of the Highly Improbable, and then again in his 2012 book, Antifragile: Things That Gain from Disorder.

2 Source: Deutsche Boerse’s second quarter of 2023 company earnings call.

3 Source: FactSet® and Brown Advisory calculations. Portfolio information is based on a representative Sustainable International Leaders account. Portfolio attributes and performance characteristics exclude cash and cash equivalents which is 2.9% as of 08/31/2023 and are subject to change. Financial measures for the representative portfolio were calculated as the median values, in order to reduce the effect of significant outliers and provide a representative view of the average returns of the portfolio. ROIC is a measure of determining a company’s financial performance. It is calculated as NOPAT/IC; where NOPAT (net operating profit after tax) is (EBIT + Operating Leases Due 1-Yr)* (1-Cash Tax Rate) and IC (invested capital) is Total Debt + Total Equity + Total Unfunded Pension + (Operating Leases Due 1-Yr * 8) – Excess Cash. ROIC calculations presented use LFY (last fiscal year) and exclude financial services. Free Cash Flow

(FCF) is a measure of financial performance calculated as operating cash flow minus capital expenditures. FCF yield is a measure of financial performance calculated as operating cash flow minus capital expenditures. FCF yield calculations presented use NTM and exclude financial services. Sales growth rate is based on reported company revenue for the past three years at the end of the current quarter, provided as a historical average.

Portfolio level information is based on a representative account as of 8/31/2023.

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested.

The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timelines s o r accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

Multiple informational inputs are considered as part of the investment process, alongside data on traditional financial factors. The strategy intends to invest in companies with measurable sustainable outcomes, as determined by Brown Advisory, and seeks to screen out particular companies and industries. Brown Advisory relies on third parties to provide data and screening tools. There is no assurance that this information will be accurate or complete or that it will properly exclude all applicable securities. Investments selected using these tools may perform differently than as forecasted due to the factors incorporated into the screening process, changes from historical trends, and issues in the construction and implementation of the screens (including, but not limited to, software issues and other technological issues). There is no guarantee that Brown Advisory’s use of these tools will result in effective investment decisions. The strategy intends to invest in companies with measurable sustainable outcomes, as determined by Brown Advisory, and seeks to screen out particular companies and industries. Brown Advisory relies on third parties to provide data and screening tools. There is no assurance that this information will be accurate or complete or that it will properly exclude all applicable securities. Investments selected using these tools may perform differently than as forecasted due to the factors incorporated into the screening process, changes from historical trends, and issues in the construction and implementation of the screens (including, but not limited to, software issues and other technological issues). There is no guarantee that Brown Advisory’s use of these tools will result in effective investment decisions.

Sectors are based on the Global Industry Classification Standard (GICS) classification system. The Global Industry Classification Standard (GICS) was developed by and is the exclusive property of MSCI and Standard & Poor’s. “Global Industry Classification Standard (GICS), and “GICS” are service marks of Standard & Poor’s and MSCI. “GICS” is a trademark of MSCI and Standard & Poor’s.

FactSet® is a registered trademark of FactSet Research Systems, Inc.

All investments involve risk. The value of the investment and the income from it will vary. There is no guarantee that the initial investment will be returned.