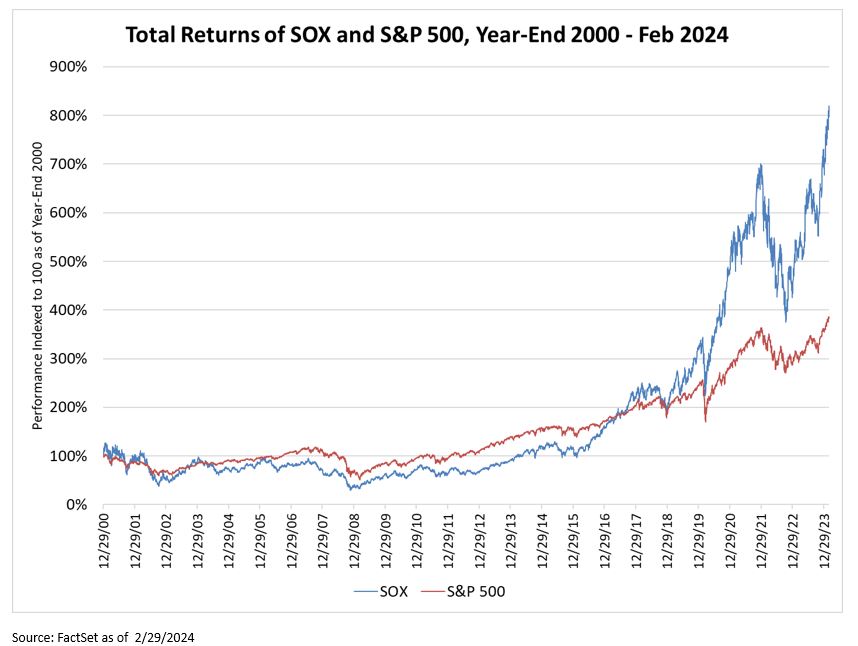

The semiconductor industry has long been viewed by investors as a highly cyclical subsector of the larger information technology sector. Driven primarily by consumer-oriented product cycles such as PCs, mobile phones and gaming, the PHLX Semiconductor Sector Index (SOX) struggled to outperform the broader market from the start of this century through the middle of the last decade due largely to the boom-and-bust nature of under-and-oversupply patterns. However, while still volatile, performance of the SOX has outshined that of other economic sectors since 2016, as many broad themes including industrial automation, electric vehicle penetration, cloud computing and artificial intelligence have diversified this industry’s end market focus. Meanwhile, the seemingly insatiable ramp of investment for accelerated compute supporting Generative AI capabilities has established a clear secular growth endorsement for many semi stocks – none more so than NVIDIA Corporation (NVDA), which has climbed a remarkable 1250% this decade1.

Writ large and about as well documented as Taylor and Travis’s celebrity romance, NVDA’s graphic processing chips (GPUs) and related equipment have brought Generative AI to life with vastly enhanced speed and computational/processing capabilities. Sharing the comments2 made by the largest consumers of GPUs this earnings season explains why NVDA is the best performing stock in the S&P 500 Index this year (up 60% in just the first two months of 2024)3.

Microsoft (MSFT):“Our research as well as external studies show as much as 70% improvement in productivity using Generative AI for specific work tasks…We expect capital expenditures to increase materially on a sequential basis, driven by investments in our cloud and AI infrastructure…Our commitment to scaling (these investments) is guided by customer demand and a substantial market opportunity.”

Amazon (AMZN): “Generative AI is and will continue to be an area of pervasive focus and investment across Amazon, primarily because there are few initiatives, if any, that give us the chance to reinvent so many of our customer experiences and processes and we believe it will ultimately drive billions of dollars of revenue for Amazon over the next several years.”

Meta Platforms (META):“We initially underbuilt our GPU clusters for Reels, and when we were going through that, I (CEO Mark Zuckerberg) decided that we should build enough capacity to support both Reels and another Reels-sized AI service…At the time the decision was somewhat controversial, and we faced a lot of questions about capex spending, but I’m really glad we did this.”

Alphabet Inc. (GOOG):“The step-up in capex reflects our outlook for the extraordinary applications of AI to deliver for users, advertisers, developers, cloud enterprise customers and governments globally and the long-term growth opportunities that offers. In 2024, we expect investment in capex will be notably higher than 2023.”

While NVDA has established a substantial advantage regarding its market position within Generative AI, many other semi companies have benefitted from an attach to NVDA products. For example4, Monolithic Power (MPWR), which solves complex power management challenges across multiple end market applications, saw revenue from its enterprise data segment (less than 20% of total 2023 revenue) climb more than 30% sequentially in 4q driven by hyperscale application strength. All other end markets – including storage, automotive, industrial, communications and consumer – experienced sequential revenue decline. The stock climbed nearly 15% on this result5.

Commentary from several semi companies this earnings season suggests that demand for chips in the auto and industrial sectors are likely to bottom during the first half of 2024. NXP Semiconductors (NXPI) sees a turning point by mid-year following a period of inventory digestion at customers. Lattice Semiconductor (LSCC) described weakness in auto/industrial as well as communications end markets, leading to a 1q revenue guide nearly 20% below consensus expectations6. Yet, LSCC stock climbed on the news, perhaps because it characterized for the first time its AI-related revenue over the long-term.

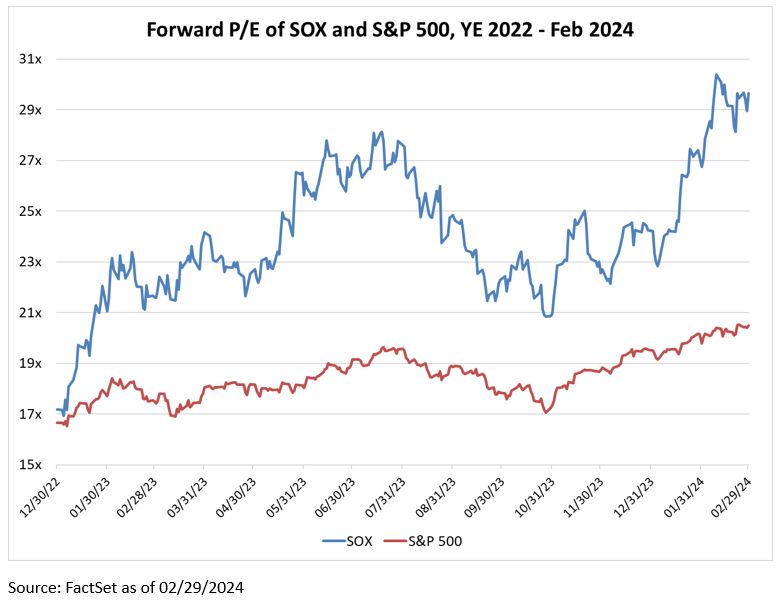

Typically, a cyclical sector would experience multiple expansion during a recessionary period and multiple contraction during a period of prosperity, with the expectation that conditions will simply shift from boom to bust, and back again. The current valuation backdrop for the semi subsector (SOX trades at 30x P/E versus S&P 500 Index at 20x) likely suggests an expectation of not only a cyclical recovery in non-AI related markets but strong secular growth in AI-related revenue for many years to come.

Our semiconductor analyst, John Bond, explains the sub-sector’s current valuation level this way: “While the fundamental cyclicality of the industry has not diminished, perhaps investors are seeing it for what it is: a cyclical industry with a fundamental secular growth backdrop. That is how we have approached our investments in this area. We try to be nimble and are very cognizant of entry points, but fundamentally we own what we think are the best assets in the sector which we anticipate will provide higher highs and higher lows on a through-cycle basis.”

Whether or not one believes the run in the SOX is due for a short-term breather, investors can agree that semiconductor companies (and stocks) have come a long way from behaving as proxies for computer and mobile device product cycles.

Thanks for reading, and remember to never skip a Beat Eric

1FactSet

2Comments used are quotes from company Q4 2023 Earnings Calls (MSFT, GOOG, META, AMZN)

3FactSet

4Monolithic Power

5FactSet

6LSCC Earnings Call

The PHLX Semiconductor Sector IndexSM (SOXSM) is a modified market capitalization-weighted index composed of companies primarily involved in the design, distribution, manufacture, and sale of semiconductors.

The S&P 500 Index, an unmanaged index, consists of 500 stocks chosen for market size, liquidity, and industry group representation. It is a market-value weighted index (stock price times number of shares outstanding), with each stock's weight in the Index proportionate to its market value.

Standard & Poor’s, S&P®, and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a subsidiary of S&P Global Inc.

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

Terms and Definitions:

Forward P/E Ratio: The Forward P/E Ratio is determined by dividing the price of the stock by the company's forecasted earnings per share.