Every quarter, a not-insignificant number of retail companies report their financial results after the more traditional earnings season concludes. This group has a fiscal year that ends in late January rather than the more common Gregorian calendar that ends in December. Since the holiday season tends to be so busy for retailers, it makes sense to delay the year-end accounting process of closing the books by a month. The favorable outcome of this quirk of the calendar is that we can continue to keep close tabs on the health of the consumer beyond traditional earnings season.

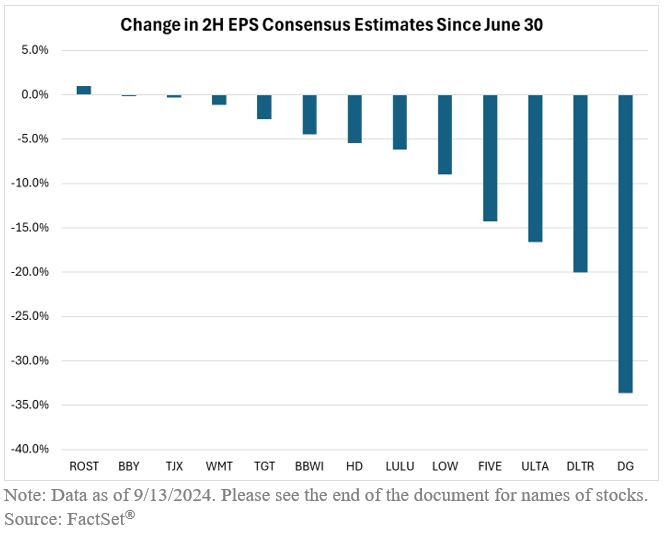

As shown above, there is meaningful dispersion in how retailers are faring in the current macro environment. Off-price retailers such as Ross Stores and TJX Companies have experienced minimal change to their second half (Aug-Jan) EPS consensus estimates in recent months as customers continue to frequent their predominantly physical “treasure hunting” stores. General merchandise big-box retailers such as Walmart and Target have only seen moderate negative earnings revisions in recent months, as customers typically traffic their stores looking for deals and opportunities to consolidate their purchases at fewer merchants.

On the other end of the spectrum are the lower price-point discount chains such as Five Below, Dollar Tree and Dollar General, all of which have seen significant negative second half earnings revisions. A more challenging promotional backdrop along with lower-income consumers feeling worse off financially plays into these companies’ difficulties. However, Dollar Tree commented this quarter that middle and upper-income households were also under some pressure. As a reminder, the typical price point at these stores is only $1-$5, while according to Bloomberg, the average transaction value is below $25.

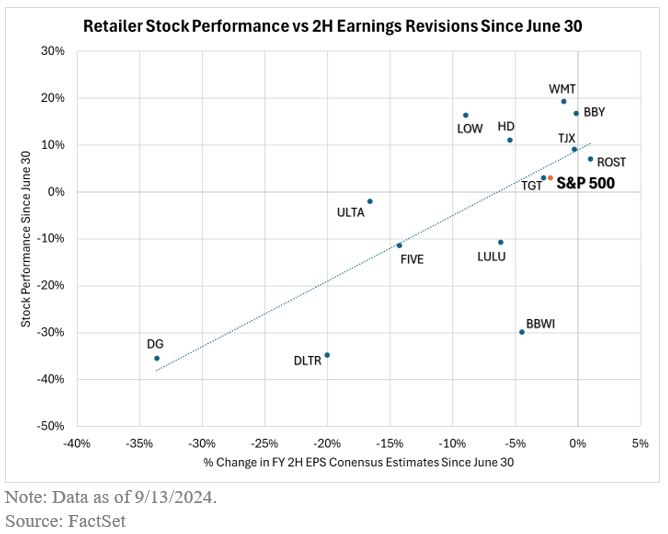

These retailers’ stocks have responded to their respective adjustments in earnings revisions for the second half of the year. Generally, the lower-price discount concepts are the worst performing stocks quarter-to-date, while the retailers with minimally negative, or positive earnings revisions have experienced positive stock performance. I would note that the S&P 500® Index is below the trendline on this chart, suggesting that the retail stocks shown have received more stock price benefit from changes to earnings revisions than the broader Index. In other words, while the S&P 500 Index has seen its 2H EPS consensus revisions at negative 2%, the Index is up 3% on the quarter. The trendline of these retail stocks would have predicted a mid-to-high single-digit return for the S&P 500 Index for the same adjustment to earnings estimates.

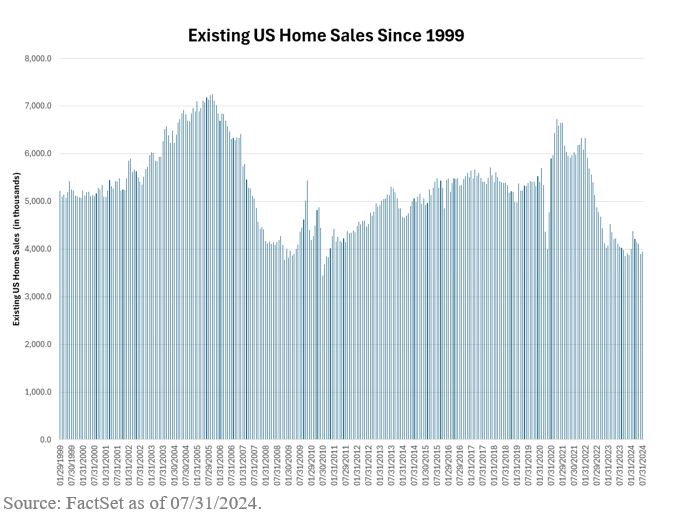

Home improvement stocks Lowes (LOW) and Home Depot (HD) are above the trendline – both have seen solid, positive stock performance despite 5-10% declines in 2H earnings estimates. Investors are likely looking past near-term financial performance and are instead assuming that business conditions will improve with rate cuts, which should help to lower mortgage rates. High borrowing costs largely explain why existing U.S. home sales remain at nearly a 15-year low, below an annually adjusted rate of four million homes. Historically, home improvement company fundamentals are directly influenced by changes in existing home sales trends.

Lastly, below are select quotes from these companies’ earnings calls that more-or-less express that over the past few months, the consumer is feeling added pressure driven by elevated interest rates and macroeconomic uncertainty. However, we are now at the precipice of the long-awaited Fed rate-cutting cycle, which could inject incremental optimism during future company earnings calls.

- HD: “Big-ticket comp transactions (those over $1,000) were down 5.8% compared to Q2 last year. We continue to see softer engagement in larger discretionary projects where customers typically use financing to fund a project such as kitchen and bath remodels.”

- LOW: “People aren’t moving nearly as often as they typically do because current mortgage rates are so much higher than their existing rates. Housing turnover is hovering near its lowest levels since the mid-1990s.”

- WMT: “I know everyone is looking for some piece of information that maybe indicates further weakness with our members and our customers; we’re not seeing it.”

- TGT: “Over the summer, we reduced our prices on about 5,000 frequently purchased items in many markets and we saw an acceleration in both our unit and dollar sales trends in these businesses.”

- TJX: “Our comp sales increases across all of our divisions were once again entirely driven by an increase in customer transactions.”

- ROST: “Our low-to-moderate customers…are clearly seeking value. Now more than ever, we believe price/value is critical when determining where to shop.”

- LULU: “Our full year revenue guidance acknowledges the uncertainty around the shorter holiday shopping season, and the US election in Q4.”

- BBY: “Many categories, including major appliances and TVs, continued to be very promotional in pursuit of stimulating interest and sales.”

- BBWI: “We are seeing a more value-seeking customer now versus our prior expectations and the macro is choppier. We saw traffic pressures throughout the quarter.”

- FIVE: “Very similar to what we saw in Q1 where our lower income demographic was underperforming, and our higher income demographic was outperforming…we continue to see that same dynamic.”

- DLTR: “Beginning this quarter, we started to see inflation, interest rates and other macro pressures have a more pronounced impact on the buying behavior of (middle and upper-income households).”

- DG: “Approximately 30% of our customers have at least one credit card that has reached its limit. And in our latest survey, 25% of our customers surveyed noted they anticipated missing a bill payment in the next six months.”

Thanks for reading, and remember to never skip a Beat – Eric

Source: Factset®. FactSet is a registered trademark of FactSet Research Systems, Inc

Retailer stocks: Bath & Body Works Inc (BBWI), Best Buy Co Inc (BBY)Dollar General (DG), Dollar Tree (DLTR), Five Below (FIVE), Home Depot (HD), Lowes (LOW), Lululemon Athletica Inc (LULU), Ross Stores (ROST), Target (TGT), TJX Companies (TJX), Ulta (ULTA), and Walmart (WMT).

Company information is sourced from each company’s earnings call.

The views and opinions expressed in this podcast are those of the speaker(s) and do not necessarily reflect those of Brown Advisory. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. The information provided in this podcast is not intended to be and should not be considered a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

Sectors are based on the Global Industry Classification Standard (GICS) sector classification system. The Global Industry Classification Standard (GICS) was developed by and is the exclusive property of MSCI and Standard & Poor’s. “Global Industry Classification Standard (GICS), “GICS” and “GICS Direct” are service marks of Standard & Poor’s and MSCI. “GICS” is a trademark of MSCI and Standard & Poor’s.

The S&P 500® Index represents the large-cap segment of the U.S. equity markets and consists of approximately 500 leading companies in leading industries of the U.S. economy. Criteria evaluated include market capitalization, financial viability, liquidity, public float, sector representation and corporate structure. An index constituent must also be considered a U.S. company. These trademarks have been licensed to S&P Dow Jones Indices LLC. S&P, Dow Jones Indices LLC, Dow Jones, S&P and their respective affiliates (collectively "S&P Dow Jones Indices") do not sponsor, endorse, sell, or promote any investment fund or other investment vehicle that is offered by third parties and that seeks to provide an investment return based on the performance of any index. This document does not constitute an offer of services in jurisdictions where S&P Dow Jones Indices does not have the necessary licenses. S&P Dow Jones Indices receives compensation in connection with licensing its indices to third parties.

An investor cannot invest directly into an index.

Terms and Definitions:

Earnings per share (EPS) is a company's net income subtracted by preferred dividends and then divided by the number of common shares it has outstanding.