The famous adage from arguably Shakespeare’s most popular play is the backdrop of our journey this month. Juliet, of the House of Capulet, falls in love with Romeo, a member of the House of Montague, with which the Capulets have a blood feud. Juliet’s profound proclamation that Romeo’s name is just a label suggests the importance of a person or thing is the way it is; not because of what it is called.

As we transition naturally from classical poetry of the late 16th century to equity markets circa 2023, one might question the logic of the tragic heroine. After all, Artificial Intelligence (AI) has become this year’s most prominent catchphrase. While generative AI differs from traditional AI (the former is used to produce new content; the latter is used to simply detect patterns), this important distinction be damned! It’s the phrase ‘AI’ that seems to matter most to both companies and investors today.

Source: FactSet as of July 10, 2023

This is not the first time in which companies have been lured by a popular buzzword or catchphrase to capture the imagination of their investor base. In 2001, a group of authors affiliated with Purdue University’s Krannert School of Management published a study[1] that documented the striking positive stock price reaction to the announcement of corporate name changes during the “dot-com” boom of the late 1990s. The authors found that during a period from mid-1998 through mid-1999, companies that changed their name to a ‘dot-com’ moniker earned “significant abnormal returns on the order of 53% for the five days around the announcement date.” A rose by any other name? Not by a longshot.

They also determined that this price reaction was similar across all companies, regardless of their actual involvement with the Internet. A mere association with the term 'Internet' was enough to provide a firm with a large value increase. Of course, the dot-com bubble burst in the early 2000s... when stocks of companies that transitioned their names AWAY from the Internet began to benefit!

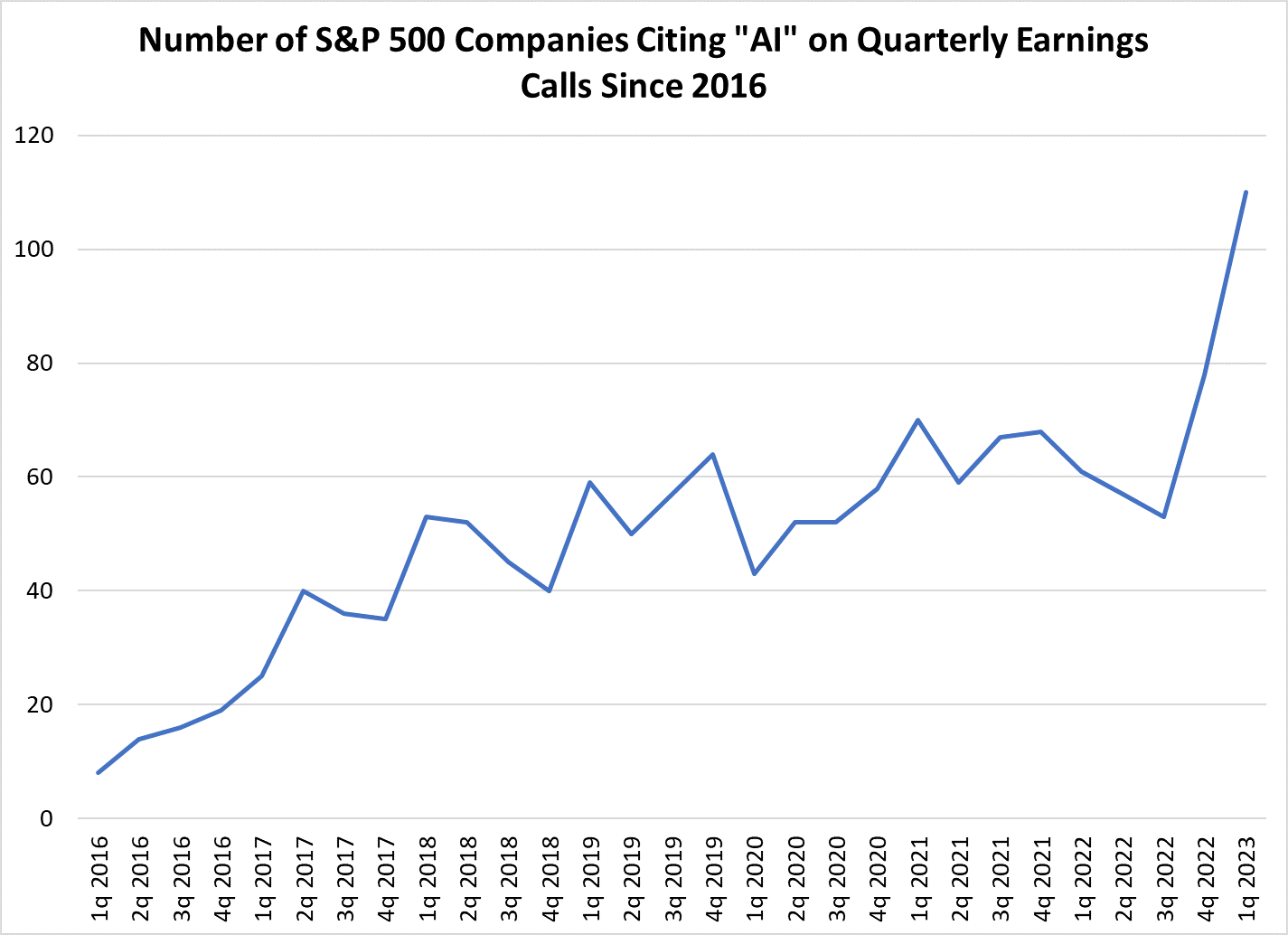

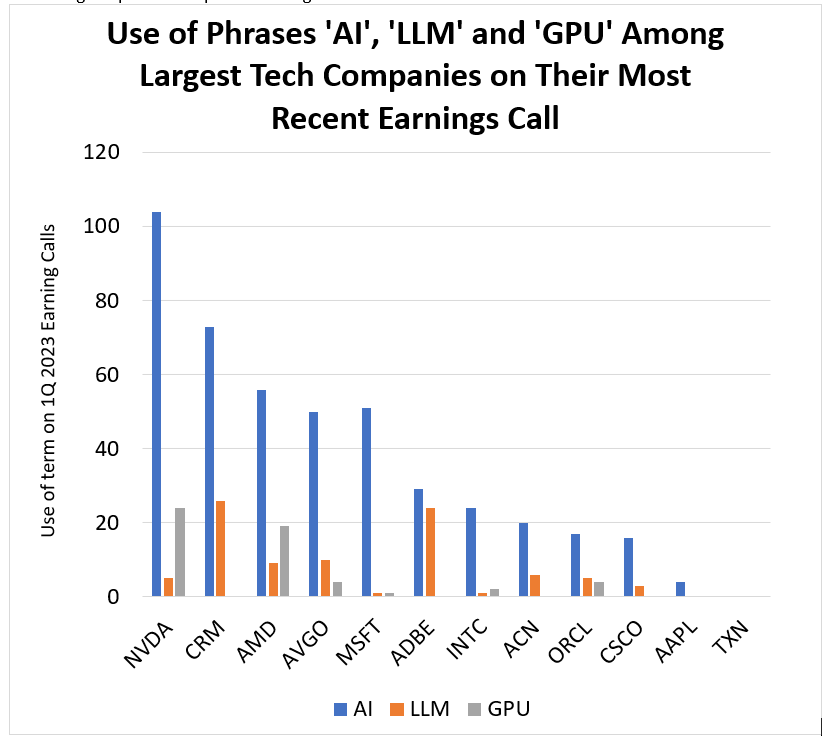

While the broad use of the term ‘AI’ has occurred across many sectors during recent earnings calls (including the industrials sector, according to FactSet, 17 S&P 500® Index companies uttered the phrase last quarter) we were able to closely analyze the largest dozen information technology companies. We broadened the catchphrase to also incorporate graphic processing units (‘GPUs’) and large language models (‘LLMs’), which are also key related buzzwords. In the chart below, you’ll see that the majority of these large-cap tech companies were generous in their use of these terms on their calls.

Source: FactSet as of July 10, 2023. Please see the end of this letter for company names.

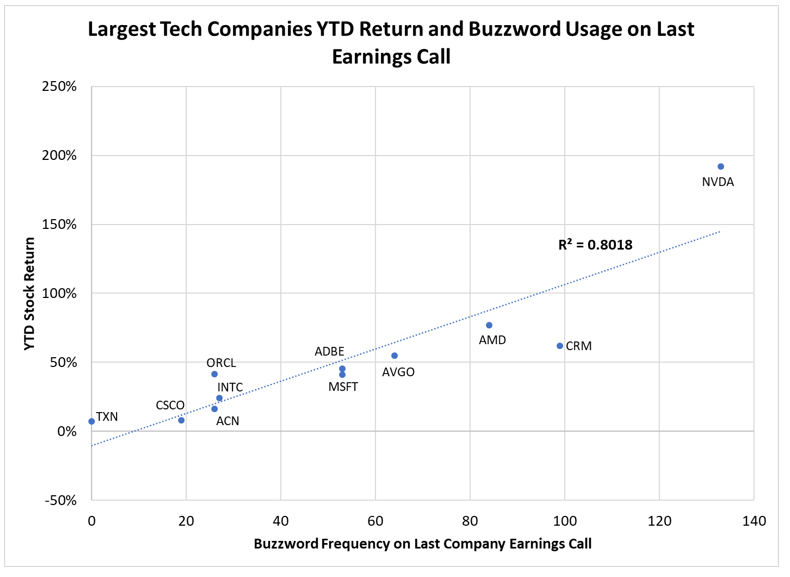

With Purdue University's study in mind, we wanted to examine whether there was much if any correlation between year-to-date stock price performance and the frequency of these buzzwords in the most recent earnings transcripts of these large technology companies. The findings are statistically relevant – the more times AI was mentioned on a company earnings call, the higher the stock has risen this year. I should note that we left Apple (AAPL) out of the chart below as it continues to march to the beat of its own drum – AI-influenced or not. I’m sorry, dear Juliet, but on the surface 2023, much like the dot-com era, appears to be a period where mere association matters more than "truth and substance".

Note: Performance as of July 5

Source: FactSet

While the scatterplot displayed above presents compelling evidence, it doesn’t paint the whole picture. Perhaps the companies that frequently discuss AI in their earnings calls, and have experienced significant stock price appreciation, are also effectively convincing analysts that there will be a corresponding increase in demand for their products and services in the years ahead. Surely, NVIDIA (NVDA) is the big winner this year because of the remarkable upward revenue guidance it has provided for the next several quarters. However, very few companies have been explicit as to the magnitude of accelerated revenue they expect to generate as a function of generative AI.

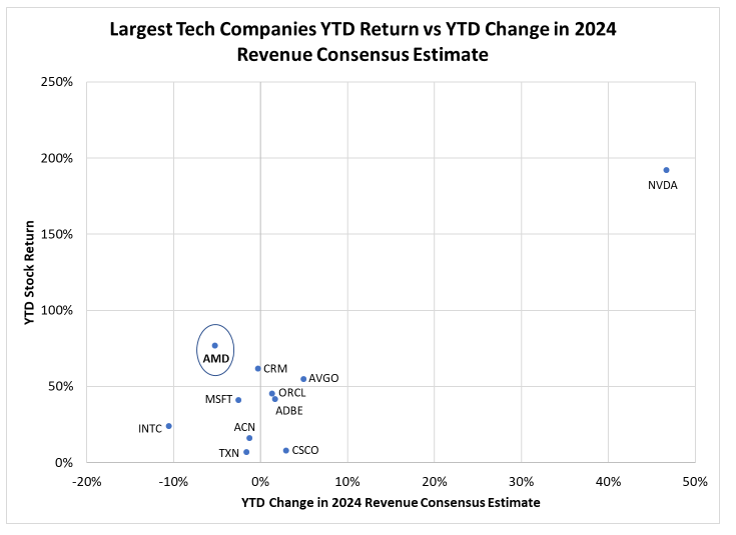

The chart above confirms that a handful of large cap tech companies have seen an increase in 2024 consensus revenue estimates this year. However, just as many have seen their consensus revenue estimates for 2024 decline this year despite the excitement around generative AI. Advanced Micro Devices (AMD) – which we do not cover/own – has seen its forward revenue estimate decline by a sizeable 5% this year, yet the stock has climbed 75% YTD. While AMD will likely continue to attempt to compete with NVDA’s GPUs, AMD’s stock run rhymes with the “dot-com” effect - driven by mere association.

We are still in the very early innings of a technological advancement that has driven equity market returns this year, where early winners have seemingly already been crowned. Similar to prior periods of market hype, buzzwords and speculation should eventually give way to “truth and substance” – and in the end Juliet’s rose adage will likely prove accurate. Call NVDA by any other name, and it is still in the catbird seat to capture its fair share of data center infrastructure spend in the years to come as a result of ChatGPT’s success and the imaginations it has captured. Other companies – some within the technology sector and others outside – are parroting a catchphrase that may sputter in relevance. “Out, out brief candle!”

Thanks for reading, and remember to never skip a beat – Eric

CIO Perspectives Podcast: Banking Crisis Update, AI Developments & COVID Normalization

In this episode, Erika Pagel and Sid Ahl are joined by Mike Poggi for a wide-ranging discussion about some of the forces currently disrupting capital markets, including: ongoing struggles within regional banks, the rapid progression of AI, lingering impacts of COVID and the re-opening of the economy.

Listen now

[1] “A Rose.com by Any Other Name”, Journal of Finance, published in December, 2001.

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

Factset® is a registered trademark of Factset Research Systems, Inc

Terms and Definitions:

R-squared (R2) is a statistical measure that represents the proportion of the variance for a dependent variable that’s explained by an independent variable in a regression model.

Forward revenue is an estimate of the next period's revenues of a company, usually until the completion of the current fiscal year and sometimes to the following fiscal year.

The S&P 500® Index is an unmanaged index consisting of 500 stocks chosen for market size, liquidity, and industry group representation. It is a market-value weighted index (stock price times number of shares outstanding), with each stock's weight in the Index proportionate to its market value.

Standard & Poor’s, S&P®, and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a subsidiary of S&P Global Inc.

All financial statistics and ratios are calculated using information from FactSet as of the report date unless otherwise noted. FactSet® is a registered trademark of FactSet Research Systems, Inc.

The Global Industry Classification Standard (GICS) was developed by and is the exclusive property of MSCI and Standard & Poor’s. “Global Industry Classification Standard (GICS), “GICS” and “GICS Direct” are service marks of Standard & Poor’s and MSCI. “GICS” is a trademark of MSCI and Standard & Poor’s.

Nvidia Corp. (NVDA), Salesforce Inc. (CRM), Advanced Micro Devices, Inc. (ADM), Broadcom Inc. (ADGO), Microsoft Corp. (MSFT), Adobe Inc. (ADBE), Intel Corp. (INTC), Accenture Plc. (ACN), Oracle Corp. (ORCL), Cisco Systems Inc. (CSCO), Apple Inc. (AAPL), Texas Instruments Inc. (TXN)