It’s time to pop open the champagne! Despite a heavy dose of pessimism among industry experts throughout 2023, the S&P 500® Index is in fact in bull market territory. As of the end of last week (June 9th), the broad Index has risen 20% since its most recent trough on October 12, 2022 in the face of several factors that on the surface might appear counterintuitive to a bull market. To borrow from the New York Sun’s famous 1897 editorial exclaiming the bona fide presence of Santa Claus, “Virginia, your little friends are wrong. They have been affected by the skepticism of a skeptical age.”

Source: Apple TV+

We no doubt continue to live in a skeptical age (with the possible exception of the hype surrounding generative AI); but with good reason. Over the past few months the US has experienced three sizable regional bank failures, bi-partisan negotiations that extended to the 11th hour in order to prevent a default on US government debt, mixed economic data pushing down earnings expectations and inflation levels that remain well above the Fed’s target. With this imbroglio of a backdrop, only 35% of the S&P 500’s constituents have outperformed the Index since the market trough last October.

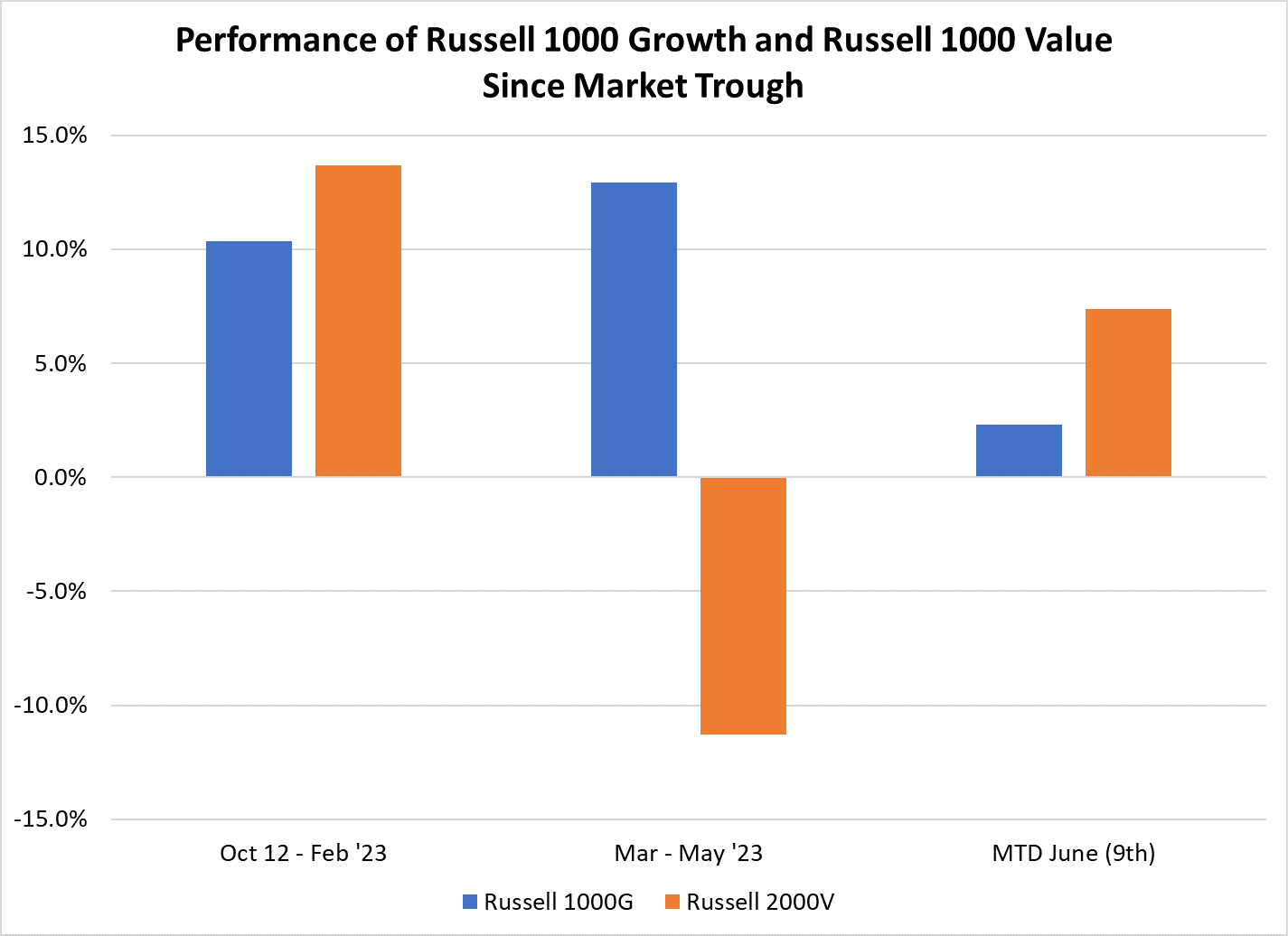

This last point may not be terribly surprising, given the media’s rapt attention placed upon the Sensational Seven (AAPL, MSFT, AMZN, GOOG, NVDA, META and TSLA have combined to account for the entirety of the market’s positive return year-to-date). However, at least as measured since the market trough in October, the period of outperformance among these mega-cap tech-oriented companies was largely concentrated in the March through May timeframe. The combination of investor fear surrounding the uncertainty of the early March regional bank crisis and the late May debt ceiling negotiations, combined with NVDA’s impressive evidence of highly accelerated investment in generative AI, created an ocean-wide gap in performance among the haves and have nots. We’ve rarely seen a three-month stretch so heavily dominated by just a handful of companies, leading to the Russell 1000® Growth Index demolishing the Russell 2000® Value Index from March to May in similar fashion to Novak Djokovic’s drubbing of Carlos Alcaraz on his way to a record 23rd Grand Slam victory at the French Open this month.

Source: FactSet Data as of 06/12/2023

Source: FactSet Data as of 06/12/2023

During the pronounced March – May period, only 21% of S&P 500 constituents beat the Index – that’s about as narrow as market leadership gets. The breakdown of the average characteristics of Index outperformers and underperformers during this period are shown below, demonstrating how larger, higher multiple and higher growth entities were in vogue during these three months.

Source: FactSet Data as of 06/12/2023

Our own research analysts have taken these recent trends into consideration when adjusting their internal stock ratings thus far in 2Q. Since the beginning of April, our team has upgraded close to 15 names while downgrading nearly 20. Below, we present the difference in characteristics (on average) among the stocks that have been upgraded relative to those downgraded.

Source: FactSet Data as of 06/12/2023

Clearly, in recent weeks our team has been favoring the smaller, less expensive stocks that have been underperforming based on this set of data. That said, during a recent team research meeting, our analysts who cover the Sensational Seven stocks (excluding TSLA which we don’t own) were not inclined in an absolute sense to trim positions in those names given their favorable longer-term characteristics and return profiles.

It’s a tricky moment for investors as we approach the early summer lull (most companies are in a “quiet period” and the flow of earnings reports has declined to just a trickle). Earnings season for 1Q (March-quarter end) was generally better than expected, however commentary from April quarter-end companies across retail spoke of a deteriorating consumer spending environment in April and into May in many cases. At the same time, market leadership thus far in June (since the effective end of the debt ceiling drama) has shown a broader trend with the Russell 2000 Value Index substantially outperforming the Russell 1000 Growth Index.

Time will tell whether the next 5-10% move from roughly 4,300 on the S&P 500 Index will be up or down, but in the meantime, let’s celebrate a bull market that has surprised a large population of incredulous investors so far this year!

Thanks for reading, and remember to never skip a Beat - Eric ![]()

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

Factset® is a registered trademark of Factset Research Systems, Inc

Terms and Definitions:

Sensational Seven Stocks: Apple Inc. (AAPL), Microsoft Corp. (MSFT), Amazon.com, Inc. (AMZN), Alphabet Inc. (GOOG), Nvidia Corp. (NVDA), Meta Platforms Inc. (META) and Tesla Inc. (TSLA)

The S&P 500® Index is an unmanaged index consisting of 500 stocks chosen for market size, liquidity, and industry group representation. It is a market-value weighted index (stock price times number of shares outstanding), with each stock's weight in the Index proportionate to its market value.

Standard & Poor’s, S&P®, and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a subsidiary of S&P Global Inc.

The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values.

The Russell 2000® Value Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index representing approximately 8% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership.

Frank Russell Company (“Russell”) is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. Neither Russell nor its licensors accept any liability for any errors or omissions in the Russell Indexes and / or Russell ratings or underlying data and no party may rely on any Russell Indexes and / or Russell ratings and / or underlying data contained in this communication. No further distribution of Russell Data is permitted without Russell’s express written consent. Russell does not promote, sponsor or endorse the content of this communication.

Next Twelve Months P/E Ratio: The sum of a company's price-to-earnings, calculated by taking the current stock price and dividing it by the projected earnings per share for the next 12 months.

Long Term Earnings Per Share Compound Annual Growth Rate ( LT EPS CAGR), summarizes stock analysts' estimates for how quickly a company will grow its earnings per share. The mean annual growth rate of an investment over a specified period of time longer than one year. It represents one of the most accurate ways to calculate and determine returns for individual assets, investment portfolios, and anything that can rise or fall in value over time.

Free Cash Flow Yield is a measure of financial performance calculated as operating cash flow minus capital expenditures divided by its market value per share. Free cash flow (FCF) represents the cash that a company is able to generate after laying out the money required to maintain or expand its asset base. Free cash flow is important because it allows a company to pursue opportunities that enhance shareholder value. Without cash, it's tough to develop new products, make acquisitions, pay dividends and reduce debt

Market Capitalization is the value of the fund as determined by the market price of its issued and outstanding stock. The Weighted Average Market Capitalization of a portfolio equals the average of each holding's market cap, weighted by its relative position size in the portfolio (in such a weighting scheme, larger positions have a greater influence on the calculation).