Fast Reading

- Artificial Intelligence (AI) infrastructure financing is expanding through debt, leases, hardware financing and equity raises, creating a more complex funding environment.

- For bond investors, the key question is whether future cash-flow generation can support the scale of capital investment now being assumed, particularly as some issuers rely on growth expectations, creative financing structures or debt-like lease commitments.

- We remain cautious beyond AI “picks and shovels,” where bondholders face downside risk without equal participation in potential upside.

Introduction

Several months ago, we penned Mind the Inflection Points: Artificial Intelligence & Debt, where we set out our initial thoughts on AI infrastructure as an investment theme. We wanted to revisit the topic because many of the trends we highlighted continue to play out – and, in some cases, have accelerated. This is particularly true of the use of debt, and the changing nature of that debt, as a funding mechanism for AI infrastructure development. There have also been some recent inflection points worth considering in relation to demand for, and pricing of, AI applications, as well as the regulatory environment.

To date, our investments have remained focused on the “picks and shovels” of the AI investment cycle. As bond investors, we continue to struggle to build conviction in other parts of the AI infrastructure boom, including hyperscalers such as Alphabet, Amazon, Meta, and Oracle, where we find it difficult to reconcile fundamentals with valuations.

At the same time, actual and potential IPOs from companies such as SpaceX, Anthropic, and OpenAI suggest that private markets may be reaching their limits for higher-profile companies with significant growth capital requirements. This is particularly interesting to us given the implied growth assumptions and relatively weak free-cash-flow profiles of many of these businesses, which historically have been better served in private markets than public markets.

While the scale of debt financing associated with AI infrastructure development has not surprised us, the return of companies such as Alphabet – and potentially Meta – to the equity market for funding has. Additionally, Space Exploration Technologies, or SpaceX, recently announced its intention to acquire Cursor for $60 billion in an all-stock transaction using recently issued equity. These decisions may carry signaling value for equity valuation. We’re particularly interested, however, in the signaling value associated with companies that still appear to have meaningful balance sheet capacity while maintaining investment-grade credit ratings.

If some of the strongest issuers in the market are now choosing to raise equity, we are left to wonder whether the scale of debt financing may surprise us over the coming quarters and years. Our view of investing in bonds issued by hyperscalers is that more attractive opportunities may emerge in the future, once these balance sheet transformations are better understood or valuations better reflect the associated uncertainty.

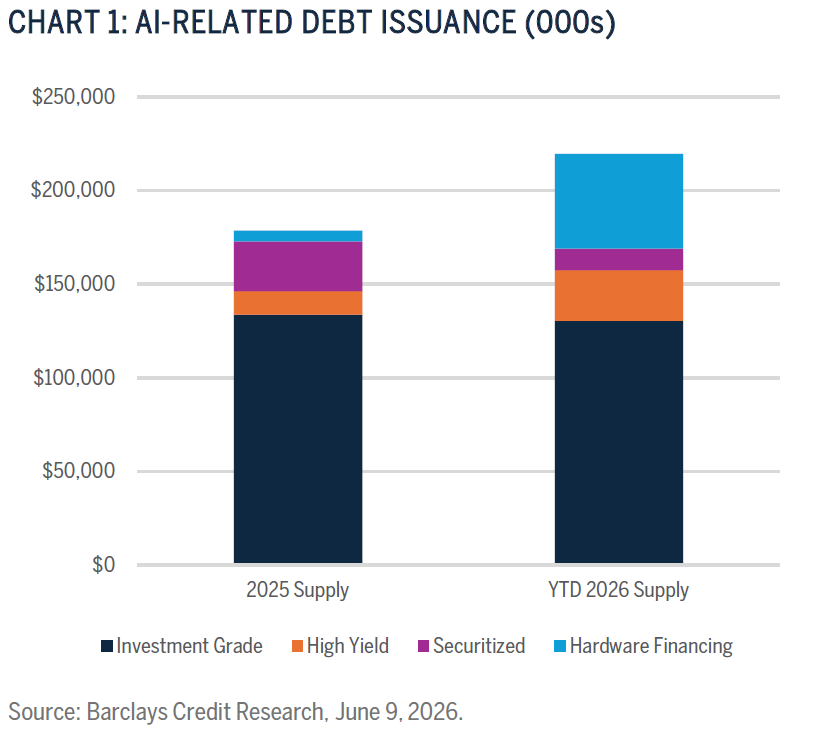

Barclays recently compared year-to-date debt issuance through the first week of June with the prior year’s total issuance across several U.S. dollar fixed income asset classes tied to the AI investment cycle: investment-grade and high-yield corporate debt, securitized debt, and hardware financing debt. Investment-grade issuance over this year-to-date period reached last year’s total of approximately $130 billion.1 High-yield corporate issuance surpassed $27 billion, more than twice last year’s total. Securitized issuance is on pace to reach last year’s level, with more than $11 billion issued thus far this year. Hardware financing, for publicly reported transactions, has increased ninefold, surpassing $50 billion.2

In total, this represents approximately $220 billion of year-to-date issuance. Hyperscalers accounted for approximately 23% of total investment-grade, non-financial corporate supply, while the Technology sector, including Amazon and Meta, represented 38% of total supply.3

The U.S. dollar market has not been the only source of funding. Hyperscalers such as Alphabet and Amazon have also issued significant amounts of debt in non-U.S.-dollar markets. Together, these two companies have issued $60 billion year-to-date, including Alphabet’s £1 billion 100-year bond in the U.K. We can think of only a small number of technology-related “century bonds” issued over the last 30 years, dating back to the late 1990s, and we believe that scarcity is instructive. It probably goes without saying that we would find it difficult to underwrite a 100-year bond when the underlying business model, competitive landscape, and capital-deployment requirements are being reshaped by a technology cycle moving far faster than the maturity of the debt.

Separately, SpaceX recently announced its intention to issue at least $20 billion of debt on the heels of their IPO. We view this as notable given the company’s negative free-cash-flow profile. Rating agencies have assigned investment-grade ratings to the issuer that appear to be based largely on balance sheet liquidity, reinforced by IPO proceeds, and on the same growth assumptions being made by equity investors. We would prefer to anchor a bond investment in sustainable free cash flow generation.

The nature of debt investments in this ecosystem also continues to evolve. In our prior piece, we discussed “circular investments” and off-balance-sheet financing. Since then, we have observed additional forms of creative financing worth highlighting. The rapid growth in hardware financing has allowed issuers to reallocate credit risk to the financed hardware and relevant counterparties – whether the manufacturer or the consumer of the hardware output – while aligning the financing with the future revenue commitments associated with that hardware.

Lease obligations on issuer balance sheets are also increasing, particularly for companies such as Oracle. At the end of August 2025, Oracle reported $100 billion of additional lease commitments expected to commence over the following eleven quarters through fiscal year 2028.4 By the end of May 2026, Oracle reported $260 billion of additional lease commitments expected to commence over the ensuing eight quarters through the fiscal first quarter of 2029.5 This is large debt-like exposure relative to $130 billion of debt on the balance sheet and will require corresponding, future revenue commitments to come to fruition. Similar to the circular funding we highlighted in the earlier piece, our interpretation is that financing creativity is increasing as funding capacity is becoming more constrained.

As bondholders, we view free cash flow as an important credit metric for assessing debt-service capacity. We often adjust free cash flow – classically defined as cash from operations less capital expenditures – for ongoing payments, such as stock dividends, that can be viewed as quasi-permanent. Another feature of the cash-flow statement worth considering, particularly for hyperscalers and other AI-adjacent companies, is the cash used to repurchase stock. These companies typically have large equity programs associated with employee compensation, and many repurchase stock to limit dilution from those stock compensation programs. These adjustments to free cash flow can be significant and not always well understood.

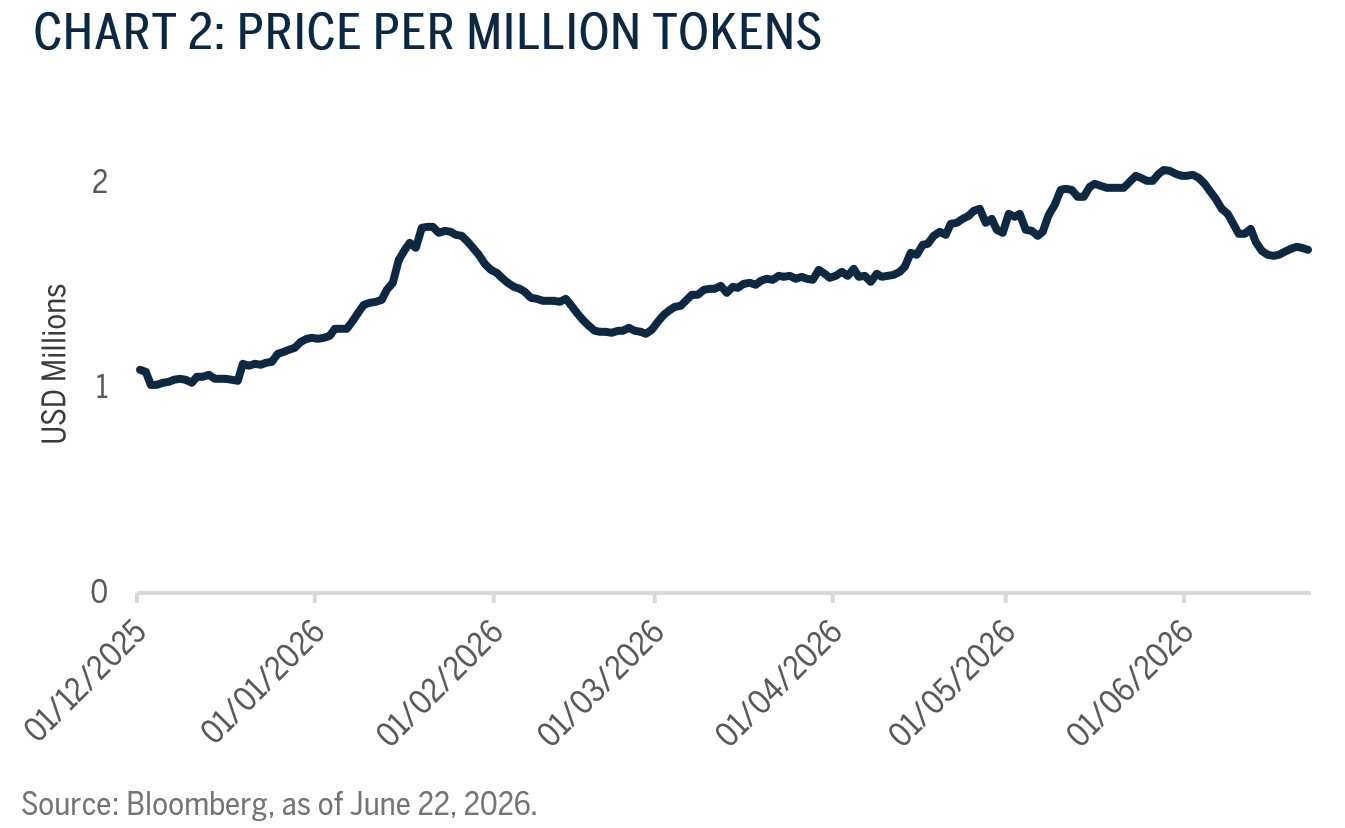

Recent articles and data on demand and pricing trends within the AI ecosystem also appear to represent important inflection points for bond investors in AI-adjacent companies, particularly those with shrinking or negative free cash flow profiles. On the demand side, companies have been outspending AI budgets and, as a result, are becoming increasingly focused on productive use cases and return on investment from AI applications. On the pricing side, companies like OpenAI have been rumored to be considering price reductions to protect demand in an increasingly competitive environment driven by peers such as Anthropic and lower-cost competitors in China.

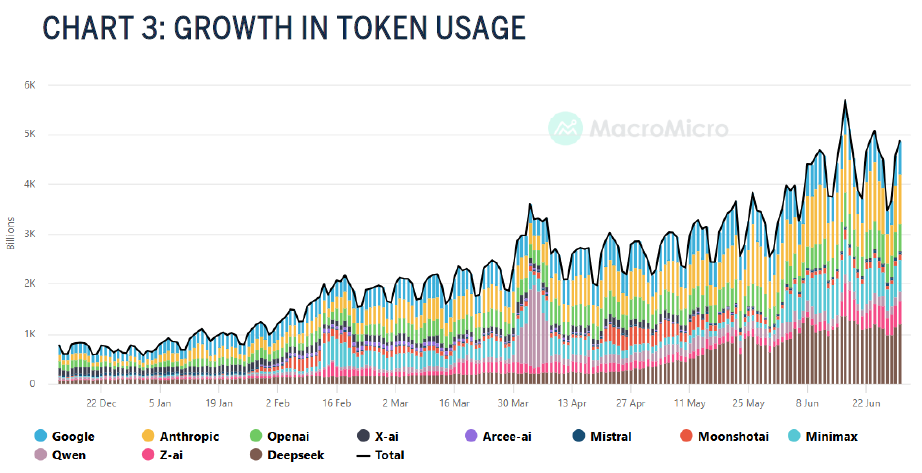

According to the Silicon Data LLM Token Expenditure Index, as shown in Bloomberg data, the price per million tokens has declined more recently. Data from OpenRouter, as presented by MacroMicro, also suggest that most of the growth in token usage has been coming from Chinese AI models and Anthropic, in that order. We cannot help but see parallels between today’s AI competitive landscape and that of the automotive industry, where Chinese automakers have placed significant pressure on U.S. and European competitors.

Source: OpenRouter Data Presented by MacroMicro, as of June 30, 2026; https://en.macromicro.me/charts/148532/world-openrouter-token-usage

We recently read The Infinity Machine by Sebastian Mallaby, a well-written origin story of AI told primarily through the perspectives of DeepMind and its founder, Demis Hassabis. We found the book’s analogies to the Manhattan Project instructive when thinking about the natural tension between the competition to win a technology race and the potential risks to humanity.

The recent encyclical written by Pope Leo XIV is also a reminder of the gravity underlying this technological innovation. Anthropic has recently shared the stage with the Pope while also finding itself in the crosshairs of the Trump Administration, first for refusing government access to its platform for specific use cases and, more recently, for creating the latest version of its AI model, which was powerful enough to raise national-security and cybersecurity risks.

Our view is that regulatory risk is likely positively correlated with the success of AI innovation. It is therefore a topic we expect to revisit if and when we begin investing in AI beyond the “picks and shovels.”

We believe this kind of complexity increases the challenge of underwriting AI economics. It also underscores the importance of a successful transition from training to inference adoption across the AI ecosystem. That transition will be necessary to deliver an adequate return on investment, particularly as annualized capital investment approaches the $1 trillion mark.

For us, this environment calls for higher levels of caution. Bondholders do not participate in the upside potential of these investments, yet they are exposed to the downside if revenue commitments, utilization rates, residual values, construction budgets, energy supply, regulation, or funding and refinancing assumptions do not materialize as expected.

We still do not think an “end-is-nigh” framing is especially useful. Nor do we think it’s necessary. The more relevant conclusion, in our view, is that the required levels of investment conviction should rise with financing complexity, dependence on growth assumptions, and uncertainty.

As a result, we’re likely to remain focused on investing in companies that benefit from AI-related spending – the “picks and shovels” of this investment cycle. We are also likely to remain on the sidelines when it comes to investing in companies raising incremental capital to finance the AI infrastructure buildout, at least until we see evidence that cash-flow generation and balance sheet health are beginning to stabilize, or until valuations better reflect our view of ongoing and material debt issuance, potential balance sheet transformations, and risks surrounding free cash flow.

More broadly, we expect to maintain a defensive posture in credit exposure within portfolios until our view of aggregate corporate credit fundamentals is better aligned with valuations, which have not been this rich since the late 1990s.

As always, we’re keen to debate this important topic and would welcome your thoughts.

- Source: Barclays Credit Research, as of June 9, 2026.

- Source: Barclays Credit Research, as of June 9, 2026.

- Source: Barclays Credit Research, as of June 9, 2026.

- Oracle SEC filings.

- Oracle SEC filings.

Disclosures

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results.

Past performance is not a guarantee of future performance, and you may not get back the amount invested.

The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell or hold any of the securities or funds mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent that specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. This material is intended solely for our clients and prospective clients, is for informational purposes only and is not individually tailored for or directed to any particular client or prospective client.

The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy and is not a complete summary or statement of all available data. The information in this document has not been independently reviewed or audited by outside certified public accountants. The information provided is not intended to be a forecast of future events or a guarantee of future results. Past performance is not indicative of future performance.

Terms and Definitions

Capital expenditures (CapEx) are funds used by a company to acquire, upgrade, and maintain physical assets such as property, buildings, technology, or equipment.

Credit risk is the risk that an issuer fails to make scheduled interest or principal payments.

Free cash flow (FCF) represents the cash a company generates after cash outflows to support operations and maintain its capital assets.

Return on Investment (ROI) is a financial ratio that measures the profit generated from an investment relative to its cost.

Residual value is the estimated value of a fixed asset at the end of its lease term or useful life.

“Bloomberg®” is a service mark of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited.