The day your business sells is often remembered as a finish line with wire confirmation, signatures, congratulations, and the quiet exhale that comes after years (or decades) of disciplined effort. But for many founders, owners, and multi-generational operators, the real transition begins the next morning.

What changes is not just your net worth. It’s the nature of your wealth, how it behaves, how it funds your life, how it’s taxed, and how it’s stewarded across your family and community. The sale converts something you ran into something you own, and those are fundamentally different experiences.

In our work with business builders, we often return to a simple idea: the best post-sale outcomes are rarely “post-sale” decisions. They are the result of a planning process that starts well before a letter of intent and continues with clarity and calm through the first years of liquidity.

Why the Sale Can Feel Unsettling — Even When It’s a Success

For all the celebrations a transaction brings, the sale can create a surprisingly sharp emotional and operational dislocation. In practice, most owners experience three immediate shifts:

From “Stable Value” to “Marked to Market”

For years, your balance sheet likely centered on an operating asset you understood intimately. You could explain its value with customers, contracts, talent, and cash flow. After a sale, the center of gravity often becomes a portfolio which is priced daily, broadcast in headlines, and accompanied by a new kind of volatility.

From a Paycheck (or yield) to Total Return

Operators are accustomed to income: compensation, distributions, rents, or predictable draws. Post-sale wealth is different. The portfolio’s job is to generate total return, a blend of income and appreciation, across assets with different cycles and liquidity profiles. That shift requires a new mindset and, often, a new spending framework.

From Control to Coordination

In the business, you influenced outcomes: hiring decisions, customer strategy, timing of investments, and the pace of growth. In the markets, even the best investors must accept that control is limited and that successful execution depends on coordination among advisors, managers, and family stakeholders. Brown Advisory often describes this as a “thinking partnership,” built to help clients develop decision frameworks and a coherent vision for what comes next.

Tax realities are layered on top of these shifts: some owners feel they’ve lost levers they once had, such as timing deductions and expenses inside the business to manage taxable income. In a liquid portfolio, outcomes can feel less customizable unless tax-aware investment management and planning are intentionally designed into the system.

Start Earlier Than You Think: The Planning “J-curve” Advantage

Entrepreneurs intuitively understand the J-curve in building by investing time and capital early to unlock outcomes later. Planning works the same way: the highest-impact decisions typically require runway. Early dedication to planning can pay off meaningfully later, and the process is most effective when calibrated to key decision moments in the business lifecycle.

A “pre-sale” plan is not a single event. It’s a progression ideally organized around milestone moments (funding rounds, recapitalizations, valuation inflections, new partners or the first serious M&A conversations). The goal is to deliver results without forcing the owner to divert attention from building.

Before The Sale: Build Optionality and Reduce Preventable Leakage

If you only do one thing early, do this: clarify your objectives. Transaction structure, timing, and planning strategies should serve the end goal – family, freedom, reinvestment, legacy, philanthropy – not the other way around.

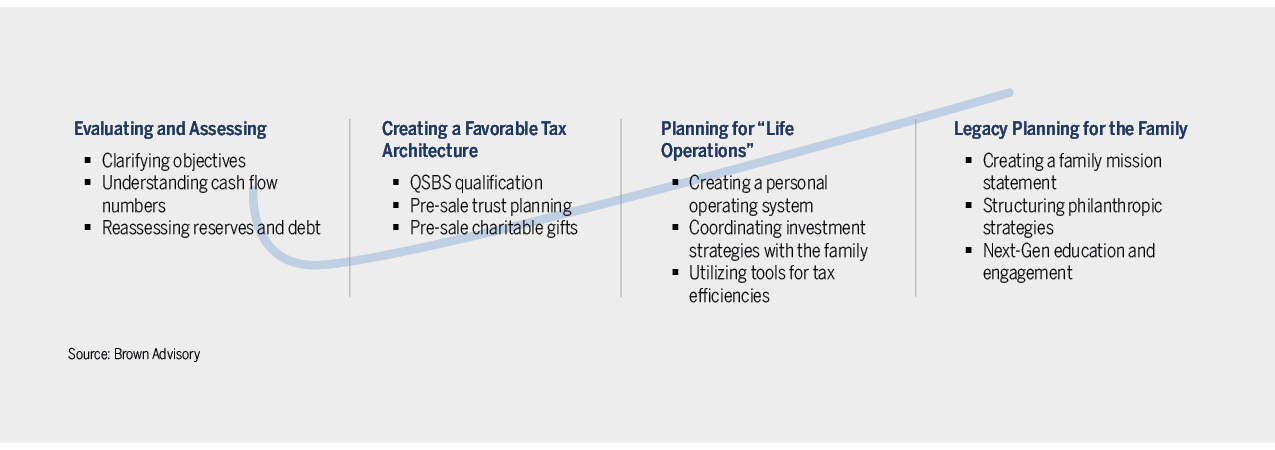

From there, pre-sale planning tends to cluster into five high-impact categories:

Understanding Your (Cash Flow) Numbers

Long-term cash-flow sustainability hinges on a handful of core numbers that show whether your financial engine can reliably support your lifestyle over decades. These figures reveal resilience, flexibility, and where small adjustments can meaningfully improve outcomes. Start with your annual spending requirement, the total amount you need each year to maintain your lifestyle, including fixed, variable, and irregular expenses. Next, inventory reliable income sources you can count on with high certainty (salary, pensions, annuities, or guaranteed benefits). Then evaluate your withdrawal rate from investments: what percentage of your portfolio you’ll draw each year, and whether that rate is sustainable under both normal and stressed market conditions. From there, translate the plan into the portfolio size required to support those withdrawals and an expected growth/ volatility range that frames long-term durability. Finally, quantify the practical modifiers that protect flexibility: cash reserves (your liquidity buffer that reduces forced selling) and debt obligations (balances, interest rates, and required payments that reduce optionality).

Tax Architecture And Exit Strategy

For many founders, the difference between “good” and “great” outcomes is not valuation but tax and structure. Where applicable, QSBS qualification can be a powerful planning tool, potentially allowing substantial federal capital gains exclusion if requirements are met. It is also detail-sensitive — documentation, tracking, and coordination with tax advisors are often decisive. Trust planning can support wealth transfer and, in some cases, amplify tax benefits. In the right fact pattern, non-grantor trusts can be part of broader planning, including multi-state considerations and thoughtful implementation. Finally, if philanthropy is part of your family’s story, charitable strategies before the sale can materially improve efficiency. Gifting pre-sale shares (rather than cash after closing) may be more tax efficient. Common vehicles include donor-advised funds and private foundations, and in certain cases charitable remainder trusts.

Wealth Transfer Planning While Valuation Is Still “Private”

Before liquidity, there may be opportunities to transfer value at discounted or more favorable terms, particularly when the business is still closely held and prior to a final pricing mechanism. For families considering multi-generational planning, this can include discounted gifts to irrevocable trusts for descendants, funding trusts over time (rather than all at once), and pairing longer-term strategies with enough flexibility that the plan can evolve alongside the business.

A Plan For Life Operations, Not Just Investments

Selling a business often removes a hidden infrastructure: the people and processes that made life run smoothly. Owners may suddenly need to answer practical questions they haven’t faced in years:

- How do I get funds on a regular cadence?

- Who pays household bills and manages cash flow?

- Who coordinates insurance, tax documents, calendars, and family logistics?

Transaction Readiness Without Losing Momentum

At Brown Advisory, we recognize the dilemma that entrepreneurs face: builders thrive on risk, ambiguity, and control traits that can make proactive transition planning feel unnatural or easy to defer. The practical solution is often a middle path: focus on transaction readiness early, so the business and the owner are not forced into rushed decisions later.

Having a good handle on these things upfront allows you to evaluate what will be required upon exit (post-tax) and assess whether there is likely excess capital for more advanced planning. The consistent theme: these are not “week before closing” projects. They require time for proper design, documentation, and coordination among legal and tax professionals.

After The Sale: Design Your New Balance Sheet To Support Your Life

Once liquidity arrives, planning becomes real-time and intensely personal. Brown Advisory’s work with entrepreneurs explicitly recognizes that the transition from owner to investor raises new questions, and that post-sale success includes both implementation of long-term plans and the “next steps” on family, governance, and philanthropic objectives. In practice, the first 6–18 months post-sale are typically about three priorities:

Revisit Capital Sufficiency And Cash Flow Clarity

Before you optimize returns, you need confidence that your lifestyle is sustainably funded across market environments, tax regimes, and family needs. This often means defining a long-term spending policy, establishing cash reserves for near-term needs, and creating a cadence for distributions from the portfolio that mirrors the psychological comfort of a “paycheck,” even if the portfolio is designed for total return.

Investor Education And Decision Frameworks

Many owners know their businesses better than they know about markets and that’s normal. The goal isn’t to become a day-to-day market expert; it’s to develop a repeatable set of rules for decision-making (rebalancing, liquidity management, risk limits, and manager selection) so daily headlines don’t drive long-term outcomes. For entrepreneurs who are no longer in the day-to-day of operating a business, the most durable portfolios tend to separate two buckets:

- The Core Portfolio: built to fund your lifestyle, protect purchasing power, and support long-term family objectives with appropriate liquidity and diversification.

- The Sandbox: a defined allocation for private opportunities PE/VC, direct deals, or strategic concentrations where you can stay close to what you know and enjoy the builder’s mindset.

Rebuilding Purpose And Momentum

Business builders are wired for motion. For many, inactivity after an exit is not restorative, it’s destabilizing. The healthiest post-sale paths often include a deliberate plan for engagement: board work, mentoring, a new venture, or a philanthropic focus that is active rather than purely financial.

Tax-Aware, Not Tax-Obsessed

Tax efficiency can materially improve outcomes, especially when your wealth has shifted from a business engine to a taxable portfolio. Common tools include:

- Tax-loss harvesting

- Thoughtful asset location

- For some investors, specialized tax-aware investment strategies considered by some as an evolution of tax-loss harvesting in managed accounts

But a reminder worth stating plainly: don’t let the tax tail wag the dog. Complexity has financial, administrative, and emotional costs. A strong plan weighs the value of sophistication against the friction it introduces, and it ensures you retain direct access to enough liquid capital to fund your lifestyle indefinitely.

Philanthropy And Family Governance: Turning Wealth Into Shared Purpose

Liquidity is not only a financial event, it is a family event. Over time, the most successful wealth transitions are the ones rooted in shared clarity: values, purpose, and a practical plan for decision-making across generations.

We believe that a family mission statement is a useful way to filter out the background noise and focus on long-term personal, financial, and philanthropic objectives. For many families, this becomes the anchor that connects the right giving vehicle (donor-advised fund versus foundation), legacy planning that integrates charitable and wealth transfer strategies (including CLAT structures in appropriate situations), and next-generation education and involvement through family meetings, shared learning, and a clear understanding of responsibilities.

The point is not to manufacture agreement on everything. The point is to create enough shared language and process that wealth remains a tool by serving human and community goals rather than becoming a source of confusion or conflict.

Closing Thought: The Goal Is Agency

A sale often replaces a familiar set of challenges with a new, unfamiliar set. The answer is not to minimize complexity by ignoring it. The answer is to translate complexity into clarity and into a decision framework that supports your life, your family, and your purpose. That is the post-sale paradigm shift: moving from building value to stewarding it intentionally, collaboratively, and with the confidence that comes from a plan designed well before the moment it is needed.

Our Strategic Advisory team remains committed to helping you through this exciting new phase of your life. We are here to help with any questions or concerns you may have and as always, we look forward to starting a conversation so please do not hesitate to contact us. ![]()

The views expressed are those of Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested.

The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.