2024 ASSET ALLOCATION VIEWS

Discussion of 2024-2026 Scenario Analysis

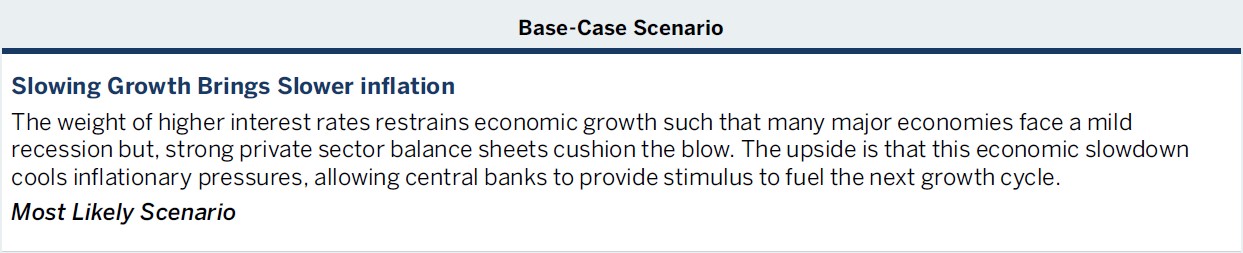

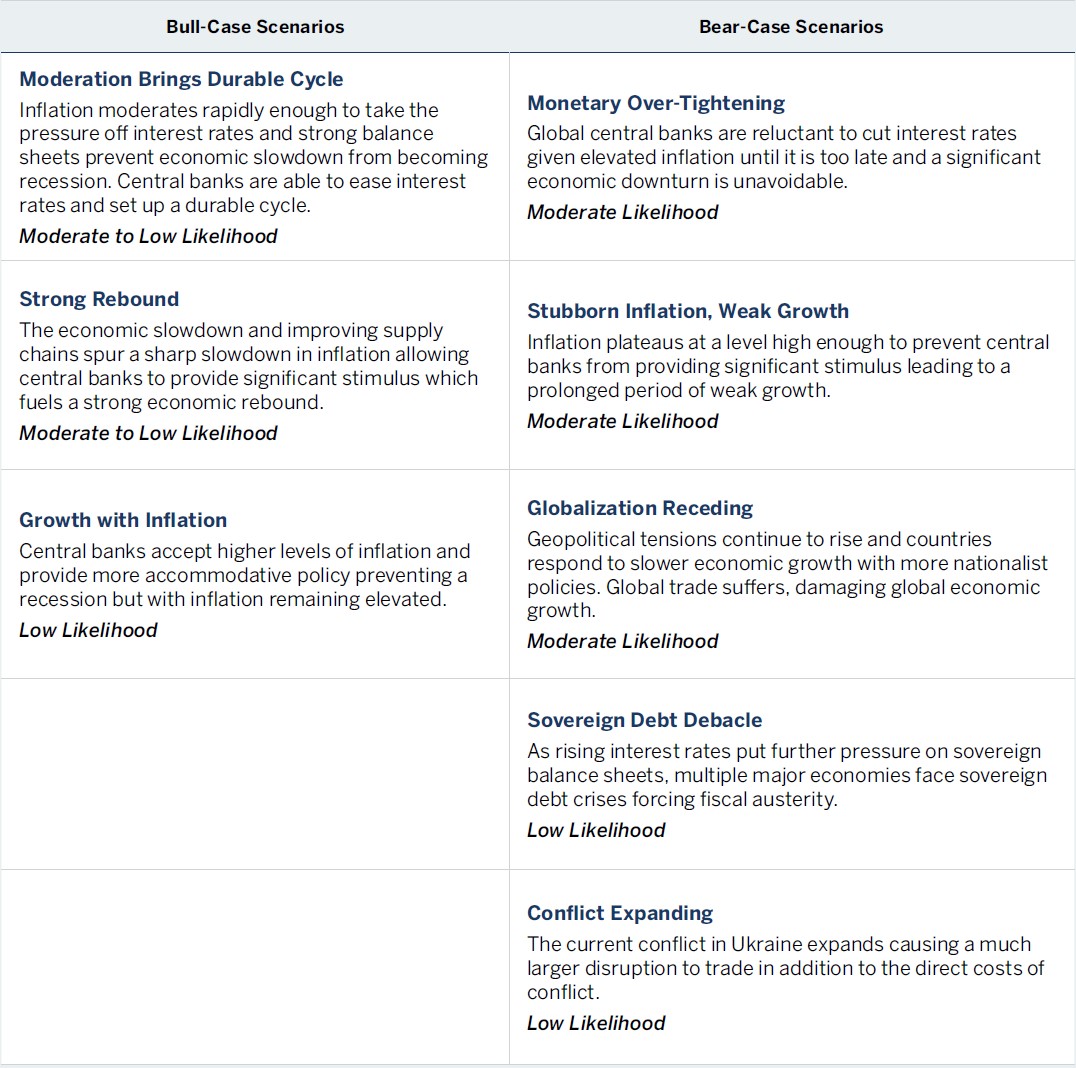

Asset Allocation Scenario Analysis

Our asset allocation stance is largely based on our long-term return and drawdown risk estimates across asset classes. For equities, the key inputs for our long-term return estimates are starting valuations, economic growth expectations (or potential GDP growth) and changes in interest rates. For fixed income, the key input is starting yields (incorporating both base government bond yields and credit spreads), with some influence from the slope of the yield curve and anticipated changes in yields.

The year 2023 brought another tangible increase in bond yields (despite the major decline at the end of the year), and equity market valuations rose broadly during the year—both of these trends reduced the overall long-term appeal of equities vs. bonds. Therefore, we have been utilizing fixed income and credit more extensively than we did when interest rates were far lower.

Equity markets are also generating diverse return streams, by market segment as well as by individual company. Small caps have lagged large caps for some time (small caps tend to be sensitive to interest-rate changes), so our forward view of small caps is more optimistic than that of large caps (which are more fully valued at the moment). We have a similar view about the runway available in emerging markets vs. developed markets. Of course, small-cap and emerging-market investments tend to be more volatile and more cyclical, especially during uncertain times, and we must take this into account with any allocations to those asset classes.

Medium-Term Outlook (18 to 36 Months)

Most major economies fared better than expected while combating inflation and rising rates in 2023. With inflation starting to ease, hopes have risen that central banks may be able to ease interest rates and avoid a recession.

The odds of a soft landing have increased over the past year, but the global economy is far from out of the woods, and most major economies have already slowed to some extent. The full pressure of higher interest rates has yet to be felt; that pressure will mount as old, lower-cost debt is replaced at higher coupons. Geopolitical tensions and weakness across U.S. regional banks are additional threats.

The European and Chinese economies are at risk from several broad factors, including demographic challenges that are already weighing on growth. China’s ongoing real estate and debt situation is also a meaningful concern for investors.

With so much uncertainty, it is more important than ever to prepare our clients’ portfolios for a wide range of scenarios. A good deal of our thinking this year, and last year, has been focused on the interplay between interest rates and inflation, and how those factors will affect the broader economy. How central banks “land” the economy will depend on their aim: how well they estimate the “true neutral” policy rate—in other words, an interest-rate equilibrium point that neither restricts nor stimulates the economy. It is an important balancing act: Recession looms if they err on one side, while renewed and stubborn inflation awaits them if they err in the other direction. We consistently labor to ensure that our clients are as well prepared as possible for this full range of potential market outcomes.

Note: All commentary sourced from Brown Advisory as of 12/31/23 unless otherwise noted. Alternative Investments may be available for Qualified Purchasers or Accredited Investors only. Click here for important disclosures, and for a complete list of terms and definitions.