Jacqueline Kennedy Onassis structured her will with an approach toward charity and her heirs that, given the outlook for interest rates, is back in style.

Through her will, former first lady Jacqueline Kennedy Onassis left behind a sizeable inheritance for her children while incorporating an innovative estate planning tool aimed at meeting her philanthropic goals. Mrs. Kennedy’s will included a little known technique at the time—called a Charitable Lead Trust (CLT)—to provide a longterm benefit to charity and her family, while minimizing her estate tax liability. Best employed while interest rates are low, the CLT is even more attractive today than when Mrs. Kennedy’s plan was conceived.

A CLT is known as a “split-interest trust” because it provides a stream of cash flow for one set of charitable beneficiaries for a fixed term, with the remainder going to a second set of beneficiaries, usually family members. It can be established during one’s lifetime or at death, with a goal of minimizing gift or estate tax. For example, a donor could establish a CLT today for a 10-year term. During the period, the CLT would pay an annual annuity to a charity. At the end of the 10 years, any assets remaining in the trust would pass to the donor’s heirs.

A CLT is known as a “split-interest trust” because it provides a stream of cash flow for one set of charitable beneficiaries for a fixed term, with the remainder going to a second set of beneficiaries, usually family members. It can be established during one’s lifetime or at death, with a goal of minimizing gift or estate tax. For example, a donor could establish a CLT today for a 10-year term. During the period, the CLT would pay an annual annuity to a charity. At the end of the 10 years, any assets remaining in the trust would pass to the donor’s heirs.

Several wealthy families have used CLTs, including the heirs of Sam Walton, founder of Wal-Mart. They have deployed the structure to transfer more than $9 billion with minimum taxation. The Waltons are not alone. U.S. families in 2012 held nearly $24 billion in CLTs, according to IRS data.

The CLT provides significant wealth transfer and charitable benefits for someone whose wealth will probably exceed the gift and estate tax exemption, set at $5.45 million for 2016. First, the IRS determines the present value of a trust by adding together the stream of scheduled payments to charity and the income from a threshold interest rate set every month by the IRS and locked in when the CLT is created. (The rate for March is 1.8%.) If the trust’s assets are invested for growth and appreciate beyond the threshold rate, then there will be trust assets remaining at the end of the term that will pass to family members without any transfer taxes. That can result in meaningful savings. Today, after the gift and estate tax exemption is exhausted, federal transfer tax rates are 40%.

No Drag

Another benefit accrues based on the income tax efficiency of a CLT. It is a taxable trust but, if structured as its own tax-paying entity as a non-grantor trust, it receives a charitable income tax deduction based on the annual payment to charity. This deduction is not limited by the level of adjusted gross income, as it can be for individuals. Instead, it is a dollar-for-dollar deduction that often will allow the trust to operate with no tax liabilities. Without a “tax drag” on the trust portfolio, the assets stay invested and grow for the benefit of family beneficiaries. While an individual who makes similarly sized gifts to charity over time will also benefit from the tax deduction, the difference between an allocation for tax paid compared with no tax paid can total as much as 0.5 percentage point per year in after-tax annualized returns. Over time, that difference can add meaningful value to the remainder gift.

The CLT is most effective when two factors are aligned: the IRS threshold interest rate is low, and growth of the assets in the trust is high. The IRS threshold growth rate generally correlates with yields on Treasury securities. So it is safe to assume that as interest rates rise, the IRS will also raise its threshold rate. With Federal Reserve policymakers forecasting as many as four increases in the benchmark interest rate this year, the benefits of a CLT may begin to wane over time. The current IRS rate, while nearly double the 1% level in 2012, is far below the 10% of the early 1990s. Delaying establishment of a CLT may mean lost opportunity. While the White House and some lawmakers have called for closing the CLT’s gift-tax “loophole,” such efforts have yet to gain traction in Congress.

Crossing the Threshold

In terms of investments, careful thought must go into the selection of assets to transfer to the CLT. Naturally, a donor wants to invest in assets that will grow at a rate higher than the IRS threshold. But to maximize the gift tax benefit, the donor wants to dramatically outperform the IRS rate. Thoughtful research and careful selection of assets can therefore boost the trust’s prospects for success.

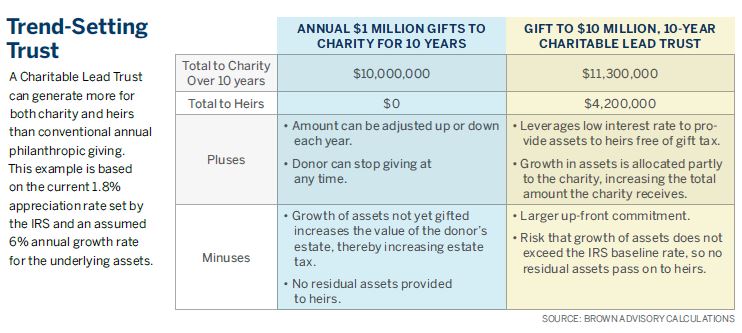

Using a CLT has clear advantages compared with the usual approach of annual charitable giving. Consider the above chart, which compares making annual charitable gifts of $1 million during a 10-year period with creating a $10 million CLT terminating after 10 years with the current 1.8% threshold appreciation rate set by the IRS and an assumed 6% annual growth in assets.

Mrs. Kennedy’s CLT was designed to begin at her death and last for 24 years, with the amount remaining at the termination of the trust passing on to her family. She aimed to save her estate millions of dollars in federal estate tax, boosting the amount provided to charity and her family. However, she gave her children the option to forgo the CLT and its tax advantages and obtain their inheritance outright, without delay. Unfortunately, they chose that option, and Mrs. Kennedy’s thoughtfully planned CLT never came into existence.

A CLT as envisioned by Mrs. Kennedy remains a powerful tool for philanthropic giving and for providing for heirs, especially with today’s historically low interest rates. Its potential benefits show that innovative estate planning never goes out of style.

Other articles in this issue:

Through the Storm

Stock market volatility has spiked in response to immediate market concerns about energy prices, weakening economic growth in China and changes to monetary policy, as well as momentous capital-market shifts during the past 20 years. In times like these, investors earn their stripes by staying focused on their long-term goals.

By Paul Chew, CFA, Head of Investments

A Lift Amid Headwinds: The Appeal of Mortgage Bonds

With the Federal Reserve tightening for the first time since 2006, investors may generate competitive returns from the comparatively stable market for mortgage-backed securities.

By Tom Graff, CFA, Head of Fixed Income and John Henry Iucker, Fixed Income Research Analyst

‘The Ultimate Mobile Device’: Redefining the Automobile

For more than a century, automakers have provided a way to find adventure and new possibilities just beyond the horizon. Now the industry is also trying to satisfy consumers’ Web-focused wanderlust.

By Simon Paterson, CFA, Equity Research Analyst

Present at the Creation: Early-Stage Venture Capital

While headlines often focus on Uber, Airbnb and other private companies valued at more than $1 billion, we are looking beyond the so-called unicorns to find opportunities for bigger returns in early-stage venture capital.

By Jacob Hodes, Co-Head of Private Equity and Keith Stone, Private Equity Venture Analyst

The views expressed are those of the authors and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance. In addition, these views may not be relied upon as investment advice. The information provided in this material should not be considered a recommendation to buy or sell any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients or other clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients and is for informational purposes only. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication.

This communication and any accompanying documents are confidential and privileged. They are intended for the sole use of the addressee. Any accounting, business or tax advice contained in this communication, including attachments and enclosures, is not intended as a thorough, in-depth analysis of specific issues, nor a substitute for a formal opinion, nor is it sufficient to avoid tax-related penalties.