In August, superstar singer and entertainer Taylor Swift completed the first leg of her Eras tour in Los Angeles, performing 52 dates through 20 U.S. cities over the past few months. Despite causing Ticketmaster’s (owned by Live Nation Entertainment) website to crash last November due to overwhelming traffic, ticket revenue from Ms. Swift’s tour – which now continues outside the U.S. - is expected to reach roughly $1.5 billion. No prior tour has even approached $1 billion in ticket revenue. What’s more, while the average ticket price (not resale) is around $200-$250, the average Eras “experience” – inclusive of outfit, food and beverage, travel and merchandise – has cost more than $1,300 per person. One research company estimates the potential U.S. economic impact of the Eras tour at close to $5 billion. No less an authority on the economy than the Federal Reserve stated, “May was the strongest month for hotel revenue in Philadelphia since the onset of the pandemic, in large part due to an influx of guests for the Taylor Swift concerts in the city.” Travel, experiences and Taylor Swift have kept the U.S. economy afloat this summer!

In 1998, co-authors and economists B. Joseph Pine II and James H. Gilmore published an article in the Harvard Business Review titled, “Welcome to the Experience Economy”. The authors claimed that the next generation of consumers would prefer compelling experiences over products, and proclaimed the arrival of the fourth economic frontier, following the agrarian, industrial and service economies.

Surely, they couldn't have envisioned quite this magnitude of success for Taylor Swift, Beyonce’s Renaissance World Tour (which was the likely cause of rising inflation in Sweden this spring) or the Barbie movie (raking in close to $1.4 billion at the box office) in 2023. Girl Power, indeed!

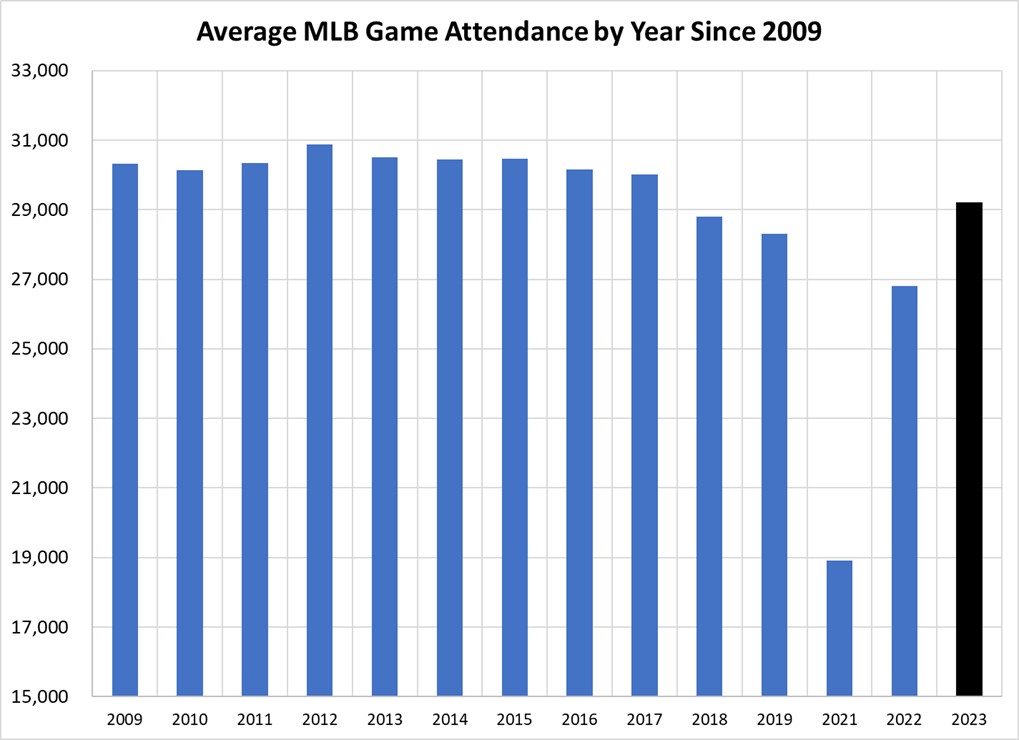

Other forms of "experiences" have seen a material pick-up in demand as well. Take Major League Baseball. The sport experienced waning popularity in the years leading up to and following the pandemic. With a few rule changes to shorten the length of the game – and perhaps due to the rebound of the "Experience Economy" – this year’s average attendance is its highest since 2017. Fun fact – compared to 2019 levels, my adopted hometown Orioles have seen the second largest percentage increase in home attendance per game in 2023, up more than 40%. Winning doesn’t hurt!

Source: ESPN

The list continues with restaurants, hotels, casinos, airlines and cruise lines. I’ve consumed 2q earnings transcripts from companies across all of these industries. Nary a one is expecting or seeing the consumer slowing down. Here are just a few examples worth sharing:

LYV (Live Nation): “We’re seeing strong growth in theaters and clubs. Our amphitheaters are doing great, substantially up in number of fans attending per show, and the high-end stadiums are doing very well. And how is the low end? Demand across ALL (demographics) continues to be very strong.”

BKNG (Booking Holdings): “We saw an acceleration in total growth of nights booked from 1q to 2q in North America…and we’re forecasting further acceleration of night growth from 2q to 3q.”

RCL (Royal Caribbean): “I want to share what we are seeing for millions of daily interactions with our customers. Sentiment remains strong and is bolstered by strong labor markets, high wages and excess savings.”

CZR (Caesars Entertainment): “We’re not really seeing anything I can speak to that’s material in terms of softness at any level of property.”

DAL (Delta Air Lines): “Consumers want to travel. It’s their number one big ticket purchase priority and they desire premium experiences.”

HLT (Hilton): “I know there are a lot of questions on the leisure business. What I would say to you is we’re having a WILDLY strong summer in leisure.”

DRI (Darden Restaurants): “Within the restaurant industry, there appears to be only minimal switching between lower-priced occasions at this point. Overall, we’re not seeing anything concerning.”

Pretty straightforward, right? There’s a longer-term trend benefiting experiences over things – there are literally dozens of recent articles on the Internet that emphasize that happiness comes more from experiences than material goods. During the pandemic, consumers went overboard on accumulating goods and people are now making up for lost time. Thus, not only is the trend towards experiences a secular phenomenon, but cyclically in vogue today.

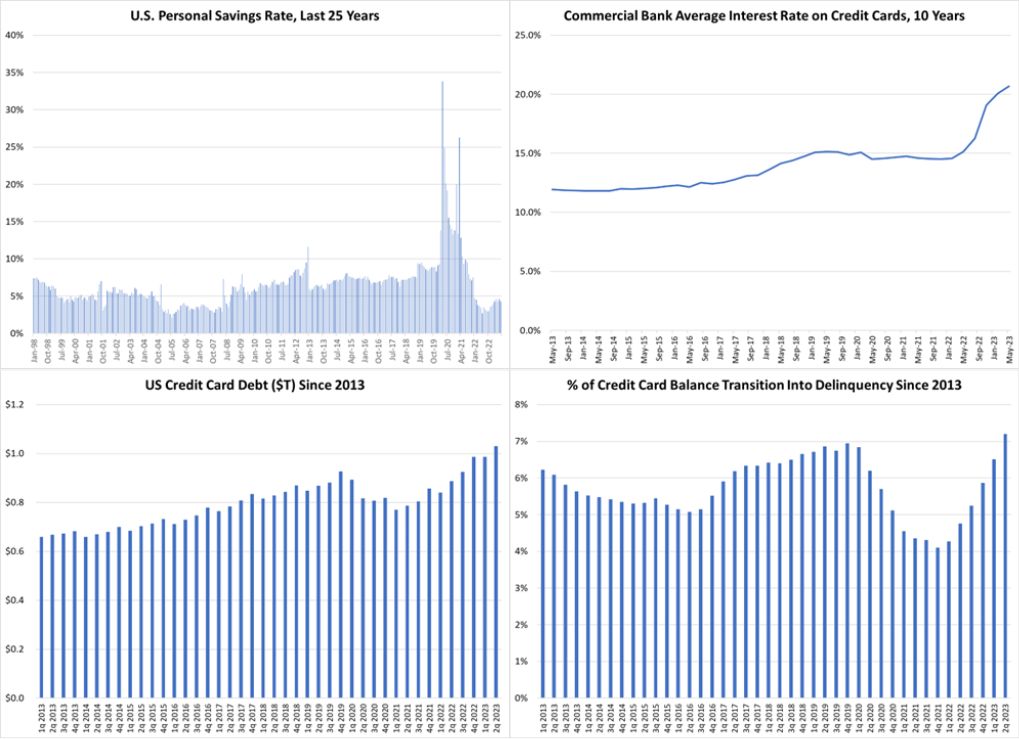

Surely however, the party cannot last forever - although I’m certainly not qualified to tell Swiftie Nation to stop singing and dancing! Still, recent economic data reveals a consumer who may need to take a breather. The Fed recently stated that U.S. credit card debt had eclipsed $1 trillion for the first time, rising $45 billion in 2q. Additionally, delinquencies on credit card debt are on the rise, while savings rates are historically low and average interest rates on credit cards are north of 20%! Although bank deposit levels were elevated in recent years, consumers are suddenly at risk of taking on very high-cost debt to maintain their experience-based lifestyles.

Source: US Federal Reserve

I can see the multitude of Swifties shaking their heads at this data, saying “Eric, you just don’t get it. Seeing Taylor Swift on stage is an other-worldly experience…and I’d do it again.” In fact, I do get it – if I could go back in time, I would have refinanced my home in 2017 to watch Roger Federer win his final Wimbledon trophy. However, that’s back when mortgage rates were sub-4%!

Thanks for reading, and remember to never skip a Beat - Eric

CIO Perspectives: Goldilocks Economy and Opportunities Outside the Magnificent Seven

In our latest episode, Sid and Erika are joined by Mick Dillon, who co-manages Brown Advisory’s Global Leaders and Global Focus strategies and has played a critical role in developing the firm’s global equity investment platform since joining Brown Advisory in 2014.

Listen now

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

Factset® is a registered trademark of Factset Research Systems, Inc

Global Industry Classification Standard (GICS) and “GICS” are service makers/trademarks of MSCI and Standard & Poor’s.

Figures shown on sector diversification and quarterly attribution by detail slides may not total due to rounding.

Terms and Definitions:

Listed stocks:

Live Nation (LVY), Booking Holdings (BKNG), Royal Caribbean (RCL), Caesars Entertainment (CZR), Delta Air Lines (DAL), Hilton (HLT), Darden Restaurants (DRI)