Unlike my good friends who frequent Baltimore’s finest dining establishments about as often as the division-leading Orioles win (you know who you are), I would never be confused for a wine connoisseur. Yet through osmosis I’ve learned that aging affords some wines time to become smoother and mellower, developing a fuller flavor as the months and years pass.

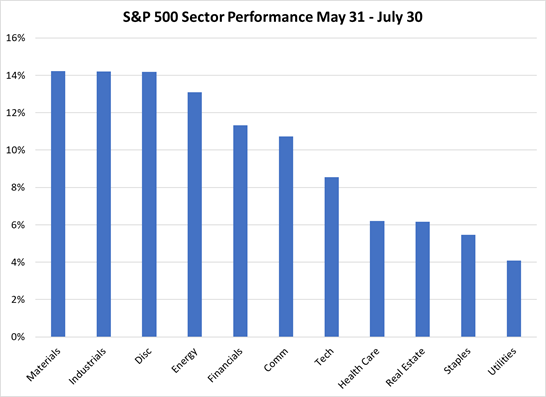

While the majority of wine lovers would shudder at the comparison of a mature half bottle of sweet Sauternes and International Paper, I shall attempt to make the connection. Most investors have been laser focused on generative AI and the Sensational Seven this year. However, over the past two months it’s been the old economy stocks leading the market. Old economy refers to industries that have not changed significantly despite advances in technology – subsectors like steel, agriculture and manufacturing come to mind, but for inclusivity let’s broaden the definition out to the industrials and materials sectors.

Source: FactSet. Data as of July 30, 202. Sectors are based on the Global Industry Classification Standard (GICS) classification system.

If we go back 50 or so years, corporate giants like General Motors, Ford and General Electric were among the very largest in the world by market capitalization. Today, it is challenging to find an industrials or materials company among the top 35 constituents in the S&P 500® Index by weight – the largest today is Linde plc, a global industrial gas producer (held in some of our sustainable strategies) that is not a household name. Still, the combined weight of industrials and materials stocks in the S&P 500 Index remains formidable at 11% - nearly as large as the oft-discussed consumer discretionary sector.

As resilient as the US consumer has been during this rate hiking cycle that may have reached its climax, US manufacturing activity according to the Institute of Supply Mangers (Purchasing Managers Index) has continued to contract, with a reading below 50 since last October. June’s reading of 46 indicated the fastest rate of contraction in the manufacturing sector since May 2020, while July’s reading of 46.4 was only marginally better. Demand remains weak as the economy continues to shift away from goods and towards services, yet very low customer inventory levels indicate the period of destocking could be concluding, a potential positive for future production should demand start to percolate.

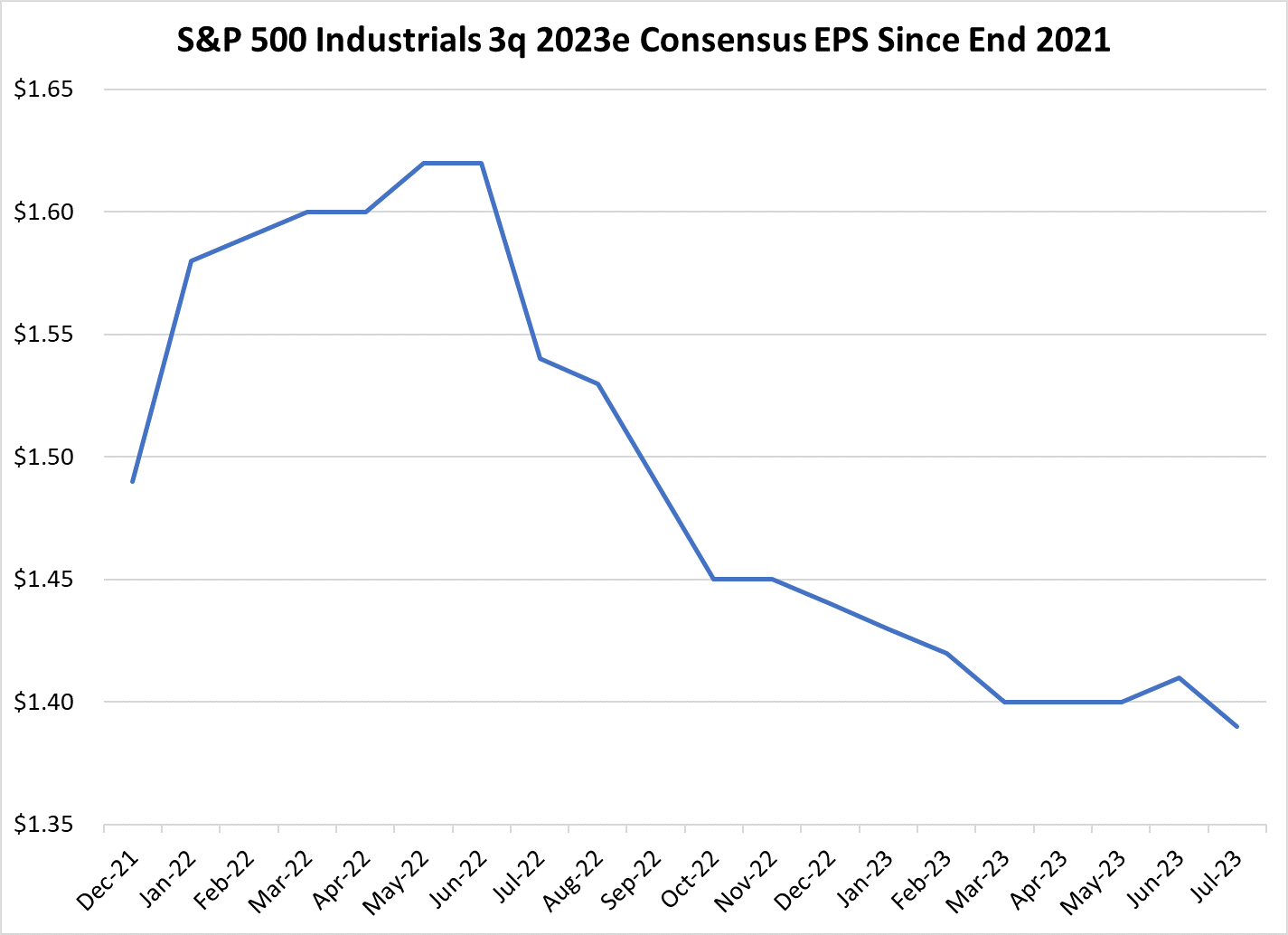

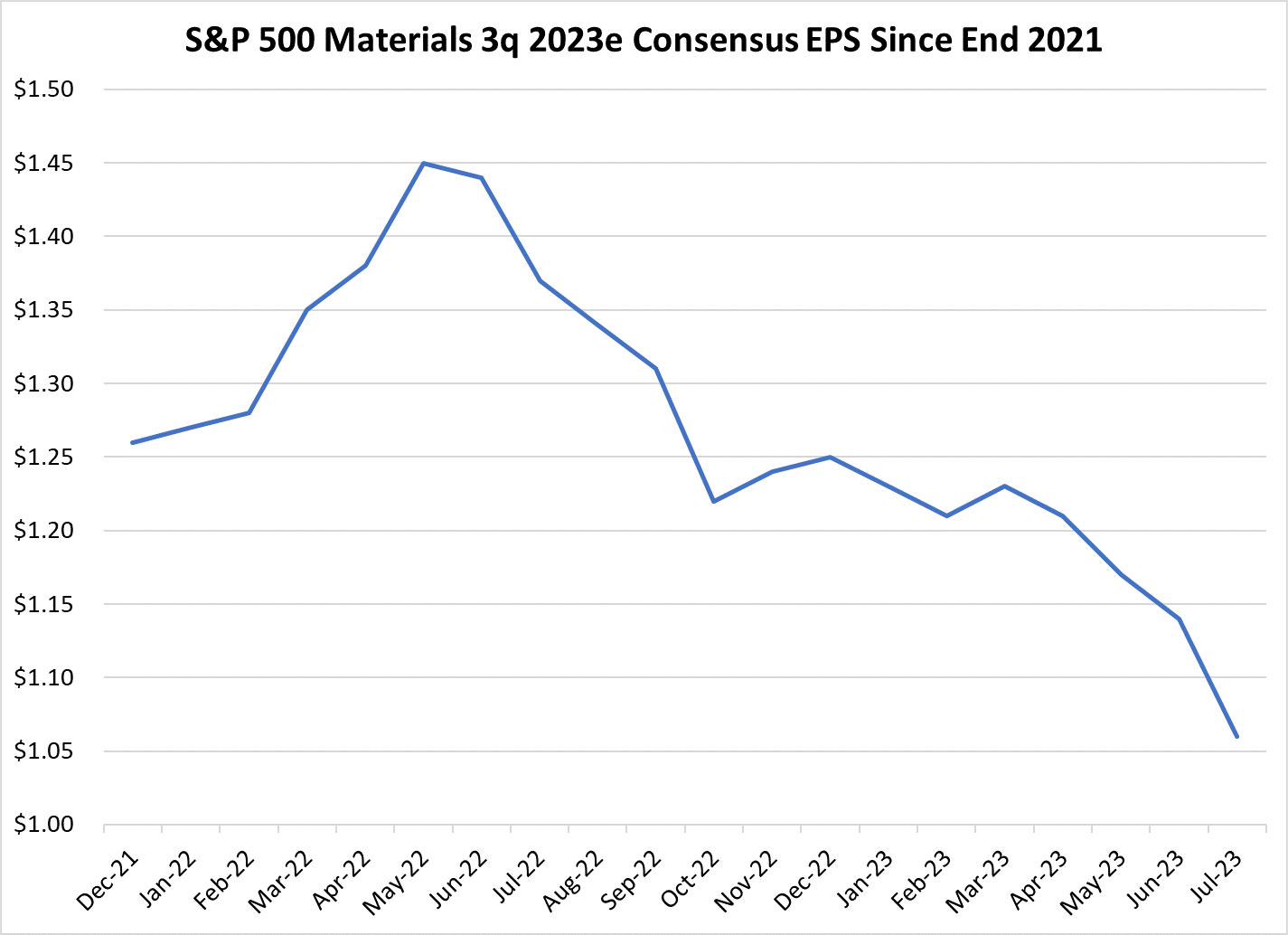

Historically, cyclical stocks will begin to climb a couple of months in advance of any significant rise in earnings expectations. As shown below, we haven’t seen much of an inflection yet in estimates for these two sectors (consistent with the ISM data). However, it’s worth pursuing what companies from the old economy are saying thus far this earnings season in order to gauge whether positive earnings revisions are on the horizon, perhaps supportive of a further broadening of stock market leadership.

Source: FactSet. Data as of July 30, 2023

Source: FactSet. Data as of July 30, 2023

Below, we highlight earnings call comments from a handful of old economy companies in recent weeks. You’ll note the tone of these excerpts run the gamut – some suggest the bottom is upon us or even behind us; others suggest a recovery is truly a world away. It’s challenging to generalize “old economy” with just one face and name, although the equity market tends to do just that. After all, while the Sensational Seven compete with each other in pockets, they are all different business models. Time will tell whether the perception of an improving backdrop for old economy sectors will persist, but for now, the stocks in these areas, much like an aged, rare Madeira are getting better with time.

Ticker | % Return (June-July) | Comment |

|---|---|---|

ODFL | 35% | “We’re at the end of a long, slow cycle.” |

NUE | 31% | “Positive trends continue in the automotive and energy sectors.” |

FCX | 30% | “…growing intensity in autos, renewables and data centers.” |

IP | 22% | “We believe that destocking is finally coming to a close.” |

JBHT | 22% | “We saw evidence from customers in June that destocking has moderated.” |

CCK | 22% | “Europe – the core consumer is exceptionally weak…stretched to make ends meet.” |

SHW | 21% | “Some positive signs in new residential construction indicate we may have reached bottom.” |

UNP | 21% | “Automotive – we expect growth to continue driven by strong OEM production.” |

FTV | 20% | “Healthcare – industry recovery is on track as labor and productivity challenges moderate.” |

MMM | 19% | “Ongoing weakness in electronics, soft discretionary retail spend patterns and mixed industrial.” |

BA | 16% | “Broadly (in aerospace), demand is strong and resilient.” |

DOW | 16% | “Third, fourth quarters are going to be the low point and then we start to ramp back.” |

AVY | 15% | “The period of challenging results will soon pass…inventory destocking (is) moderating.” |

IEX | 14% | “Key customers…are considering lower growth in China and overall macro pressures.” |

GWW | 14% | “Pockets of softness, including decelerating growth in manufacturing and commercial services.” |

GE | 13% | “Looking at the (aerospace) market, departures have almost returned to pre-COVID levels.” |

LIN | 11% | “We are seeing some economies (China, EMEA) stagnate or start to soften.” |

PPG | 10% | “We expect global industrial production to remain at lower levels in 3q.” |

FAST | 9% | “PMI has always been a good indicator…suggesting the back half is going to be weak.” |

CSX | 9% | “We look for destocking activity to wind down…though timing remains uncertain.” |

SNI | 8% | “We’re now assuming the economic recovery is pushed into 2024.” |

WM | 2% | “Customers seem to be taking a more cautious wait-and-see approach regarding large jobs.” |

HON | 1% | “Our aerospace business continues to perform at a very high level.” |

RTX | -5% | “Global commercial air traffic remains on track…very robust summer travel season.” |

Thanks for reading, and remember to never skip a Beat - Eric ![]()

CIO Perspectives Podcast: A New Bull Market? Markets shaking off a long list of concerns

In this episode, Erika Pagel and Sid Ahl are joined by Brown Advisory’s David Schuster, portfolio manager of the firm’s Small Cap Fundamental Value strategy, for a discussion about the surprising resilience of capital markets in the face of a challenging economic environment.

Listen now

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

Factset® is a registered trademark of Factset Research Systems, Inc

Global Industry Classification Standard (GICS) and “GICS” are service makers/trademarks of MSCI and Standard & Poor’s.

Figures shown on sector diversification and quarterly attribution by detail slides may not total due to rounding.

Terms and Definitions:

Sensational Seven Stocks: Apple Inc. (AAPL), Microsoft Corp. (MSFT), Amazon.com, Inc. (AMZN), Alphabet Inc. (GOOG), Nvidia Corp. (NVDA), Meta Platforms Inc. (META) and Tesla Inc. (TSLA)

Old Dominion Freight Line Inc. (ODFL), Nucor Corporation (NUE), Freeport-McMoRan Inc (FCX), International Paper Co (IP), J B Hunt Transport Services Inc. (JBHT) , Crown Holdings, Inc. (CCK), Sherwin-Williams Co. (SHW), Union Pacific Corp. (UNP), Fortive Corp (FTV), 3M Co. (MMM), Boeing Co (BA), Dow Jones Industrial Average (DOW) , Avery Dennison Corp. (AVY), IDEX Corporation (IEX), WW Grainger Inc (GWW) , General Electric Co. (GE) , LINDE ORD (LIN), PPG Industries, Inc. (PPG), Fastenal Co. (FAST), CSX Corporation (CSX), Canadian National Railway (CNI), Waste Management, Inc. (WM), Honeywell International Inc. (HON), Rtx Corp (RTX)

The S&P 500 Index, an unmanaged index, consists of 500 stocks chosen for market size, liquidity, and industry group representation. It is a market-value weighted index (stock price times number of shares outstanding), with each stock's weight in the Index proportionate to its market value.

Standard & Poor’s, S&P®, and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a subsidiary of S&P Global Inc.

The ISM Manufacturing Index, also known as the purchasing managers' index (PMI) a monthly indicator of U.S. economic activity based on a survey of purchasing managers at more than 300 manufacturing firms.

Earnings Per Share (EPS) is measured as a company's profit divided by the outstanding shares of its common stock.