Brown Advisory has championed sustainable investing for more than a decade. Some years ago, we expanded our framework into sovereign bonds, a relatively less developed area in sustainable fixed income. We view sovereign bonds as an asset class with great potential to navigate and address key environmental and social challenges facing the global economy. Our framework combines quantitative methodology with qualitative analysis in an effort to build a holistic assessment of a country’s risks and opportunities that is comparable across countries yet able to capture subtleties and gradations. We believe that one size does not fit all when assessing sovereigns’ sustainability profiles. We illustrate our approach with an in-depth analysis of Brazil, where we believe Brazil is in the process of undergoing a transition to become more sustainable as issues like climate and the environment become centre-stage once again.

Investors across the globe increasingly seek to incorporate research on sustainability-related risks and opportunities into investment decisions across asset classes to align their investment outcomes with their sustainability goals. Equity markets were the earliest and fastest adopters of this type of research, with corporate bond markets following suit, alongside the establishment of sustainable investing principles. However, sustainability approaches are still relatively less developed in other segments of fixed income markets, such as sovereign bonds, securitised credit and private debt1

Being the largest sector within fixed income—with approximately $62 trillion2 in outstanding debt and backed by the power of government—we believe that the ability and reach of sovereign issuers to navigate and address key environmental and social challenges goes well beyond the scope of a corporate issuer. Furthermore, sovereign analysis focusing on sustainability factors has the potential to reduce risk and identify compelling investment opportunities in government and corporate bonds, and particularly in emerging markets.

This paper discusses the evolution of our sustainable investing approach, from equities to corporate bonds and, most recently, sovereign debt. As the landscape continues to evolve, so too does our approach to research as more data becomes available and new lessons learned.

THE EVOLUTION OF SUSTAINABLE INVESTING AT BROWN ADVISORY

We believe that while the proliferation of sustainability themes in global investing is tremendously encouraging, investors must remain vigilant in their own examination of the authenticity of labels and claims. Brown Advisory has championed sustainable research and investing for more than a decade, driven by extensive experience in fundamental, bottom-up equity and credit research, and experience in sustainable investing, originally developed at Winslow Management Company which joined our firm in 2009.

Our sustainable investing philosophy and process were developed in-house and are supported by a robust team of research analysts, portfolio managers and other dedicated professionals. Our approach is consistent and systematic across our platform. It is based on three core tenets:

- Integration of Sustainability into Fundamental Research:We believe that investment decisions and performance outcomes improve with the combination of in-depth sustainability and fundamental analyses.

- Focus on Risks and Opportunities: Our research approach seeks to assess management of risks related to sustainability characteristics and identify opportunities that address key environmental and/or social challenges, which we believe can lead to improved performance and impact.

- Constant Innovation: We have a long history in sustainable investing and strive to stay at the forefront of this space. We continue to develop, refine and enhance our frameworks, approaches and strategies.

Our dedication to advancing sustainable investing principles is reflected in the continued expansion of our team and sustainable investment offerings, our continued transparency and reporting on the impact and sustainable merits of our investment decisions, and our extensive collaboration with key organizations. These include the Principles for Responsible Investment (PRI), the Sustainability Accounting Standards Board (SASB), International Capital Market Association (ICMA), Emerging Market Investor Alliance (EMIA) and CDP, among others, which are helping advance global standards for disclosures and reporting, and improving data availability.

Since integrating our research over a decade ago, we have expanded our framework to encompass corporate, securitized and municipal bonds. Through our global sustainable fixed income platform, we established a framework for sovereign bonds. As is the case with all asset classes, we are always learning and looking for new ways to enhance the frameworks we have already built.

FROM CORPORATE CREDIT TO GOVERNMENT DEBT: IN-DEPTH RESEARCH

Sustainable investment analysis for companies is generally well-understood. Our approach to evaluating sovereigns based on sustainable investment criteria is a natural evolution rather than a completely new construct.

There are many similarities between the types of factors we look at across corporate and sovereign debt. Ultimately, we seek to assess an issuer’s ability to service its obligations and deploy capital in an effective way. Fundamental corporate and sovereign debt analysis evaluates financial and non-financial indicators as well as specific bond characteristics. Distinctions between corporate and sovereign research arise as we define and identify the variables to evaluate each category. For instance, while non-financial indicators in fundamental corporate debt analysis assess management teams, in the case of sovereigns, the analysis involves evaluating central bank independence, quality of institutions, and the domestic and international political landscape.

Historically, sustainable investment analysis of sovereign debt was primarily focused on governance issues. However, we believe that environmental and social matters are of critical significance to sovereign growth potential and debt sustainability. For example, we believe that human capital, climate change and governance are as important to sovereigns as they are to companies. For a corporation, human capital is crucial to its ability to innovate and to mitigate against operational disruptions, just as it is key to a country’s ability to grow and develop economically. Likewise, for a company, we may evaluate its ability to attract and retain talent through its training and development programs, cultural initiatives, and employee safety metrics. For a country, we look at health and education outcomes, employment opportunities for citizens, and measures of inequality (e.g. Gini index). From an environmental standpoint, climate change is an issue creating significant disruption globally. Many corporations will likely have to restructure their business models, just as many countries will likely have to restructure their economies to mitigate and adapt to its effects. Lastly, governance comes down to how leadership— whether it be a company’s management team or a group of elected government officials—meets the needs of and is being held accountable by its various stakeholders.

FRAMEWORK FOR SOVEREIGNS: ONE SIZE DOES NOT FIT ALL

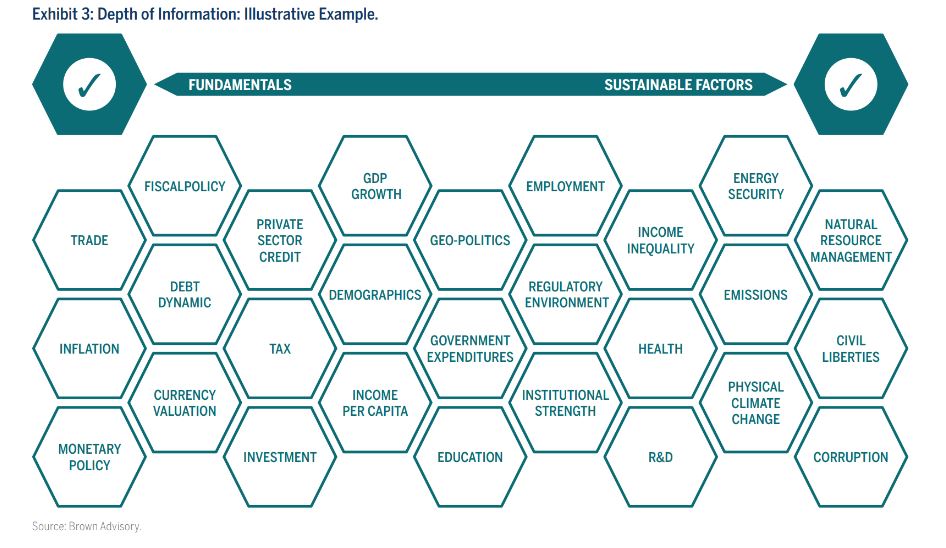

Risks and opportunities related to sustainability factors ultimately have an impact on a country’s potential for economic growth and political stability. The breadth required for analysis of sovereigns is challenging. The range of risks and opportunities that each country faces can be extremely broad, and there is often tremendous variation in the extent to which these have an impact. While consistency is a necessary condition, it is important to recognise that the effectiveness of such a framework hinges on its ability to capture nuance. Our framework combines a quantitative methodology with qualitative analysis in an effort to build a holistic assessment of a country’s risks and opportunities that is comparable across countries yet able to capture subtleties and gradations. We believe that one size does not fit all when assessing the sustainability profile of sovereigns.

Our framework combines a quantitative methodology with qualitative analysis in an effort to build a holistic assessment of a country’s sustainability-related risks and opportunities that is comparable across countries yet able to capture subtleties and gradations. We believe that one size does not fit all when assessing the sustainable investment profile of sovereigns.

Cross-country data is abundant, and its consistency and coverage have increased over recent years. Such abundance of information, coupled with biases, inconsistencies and lags that are still present in country data, require establishing clear criteria to separate signal from noise. In spite of these challenges, we believe that quantitative data is critical to harmonizing this extremely diverse universe.

While quantitative scores are informative, in isolation, we believe they offer an insufficient view of a country’s full profile. We complement quantitative scores with more traditional, in-depth qualitative analysis that validates and determines the materiality of underlying data for each country. Qualitative analysis allows us to identify trends, evaluate policy developments and current events to ensure timeliness of the quantitative data, and better estimate future developments.

Our in-house Sovereign Sustainability Score provides an initial indication of a country’s performance from over 30 indicators across a number of factors. The score is assessed against multiple peer groups—defined by income level, region and emerging/ developed market classification—to get a better contextual understanding of a country’s sustainability performance.

Our assessment is also dynamic: we calculate a momentum score to show the progress or deterioration over the last five and 10 years. This is supported by a qualitative analysis of recent trends, policy and current events that enable us to validate and determine the materiality of underlying data, assess the trajectory, and identify indications of improvement. We evaluate each sovereign on key criteria that we believe can affect political stability, promote economic growth and drive progress on key environmental and/or social challenges.

Peer group comparisons are essential in the analysis, given the broad range of characteristics encompassed by issuers. Emerging market sovereigns can often be at a disadvantage when assessed against traditional sustainable investing metrics, as they may have limited resources or are in an earlier phase of their economic development. However, we believe that there are compelling opportunities to provide capital to these issuers to support their transition to becoming more sustainable and to build resilient economies. By being able to compare countries across various peer groups and through our qualitative overlay, we believe we have a much more comprehensive understanding of a country’s sustainability performance and can determine which factors are material to its credit profile.

As in other asset classes, we believe engagement can be a particularly useful tool to enhance our due diligence and promote progress on key issues. We continue to explore opportunities to engage with debt management offices, other government officials and nongovernmental organizations either directly or through broader investor initiatives, such as the Emerging Markets Investor Alliance (EMIA). As sovereign issuers are increasingly looking to attract capital from sustainable investing-orientated allocators, it is important for us to have a seat at the table.

FUNDAMENTAL AND SUSTAINABLE RESEARCH INTEGRATION

From the bottom up and top down, we seek to build a mosaic of information to evaluate and analyse a country’s investment profile with integrated qualitative and quantitative fundamental and sustainable investment research. Multiple factors are interwoven into fundamental analysis. Together, they provide a complete picture of the fundamentals and the embedded risks and opportunities of a particular issuer. For example, social factors are focused on human capital and the ability of a country to increase economic competitiveness through its citizens. Environmental factors are focused on how a country is managing its natural capital so that it can be more resilient over the long term. And finally, governance factors are helpful in assessing a country’s ability to execute on the above objectives and ultimately meet the needs of its various stakeholders.

CASE STUDY: BRAZILIAN GOVERNMENT BONDS

Brazil has been a particularly interesting case to watch over the last year. Our initial assessment of Brazil in 2021 illuminated gaps in relying solely on quantitative data, noting that it painted a much rosier picture in terms of environmental factors than was the reality under the Bolsonaro administration. Since then, Lula has been re-elected to the presidency and we expect to see improvement in these areas over time, which we believe will be important for the resilience of the Brazilian economy.

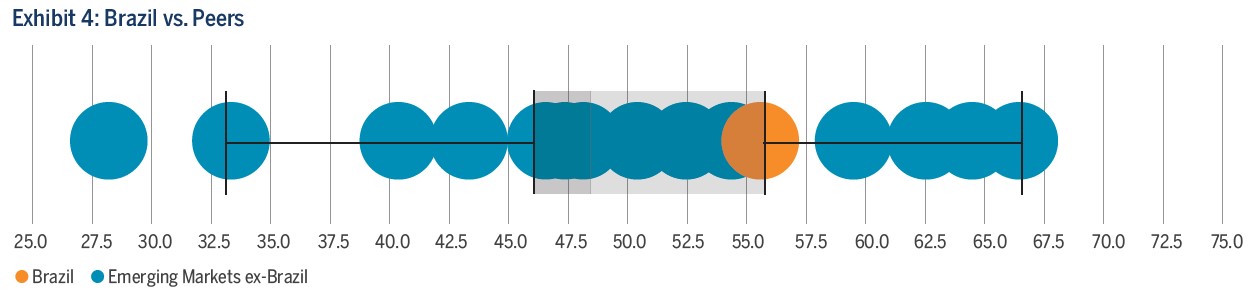

As shown in Exhibit 4, Brazil’s overarching sustainability score performs relatively well compared to its emerging market peers on an absolute basis.

Our initial assessment of Brazil in 2021 illuminated gaps in relying solely on quantitative data, noting that it painted a much rosier picture of the Environmental pillar than was the reality under the Bolsonaro administration. Since then, Lula has taken power and we expect to see improvement in these areas over time, which will be important for the resilience of the Brazilian economy.

Note: The boxplot shows the distribution of the countries’ sustainability scores through displaying the data quartiles (or percentiles) and averages. The vertical bars indicate (from left to right) the minimum score, first (lower) quartile, median, third (upper) quartile, and maximum score. Blue circles show values for the different countries in the sample and the orange circle shows the value for Brazil. The area shaded in dark gray represents the second quartile and the area in lighter gray represent the third quartile, i.e., the data closer to the average. Source: World Bank (https://datatopics.worldbank.org/esg/), United Nations, World Health Organization, International Labor Organization, Food and Agriculture Organization, Transparency International, Freedom House, International Energy Agency, ND-GAIN index (https://gain. nd.edu/our-work/coun-try-index/) and Brown Advisory. Includes most recently available data as of July 21, 2022.

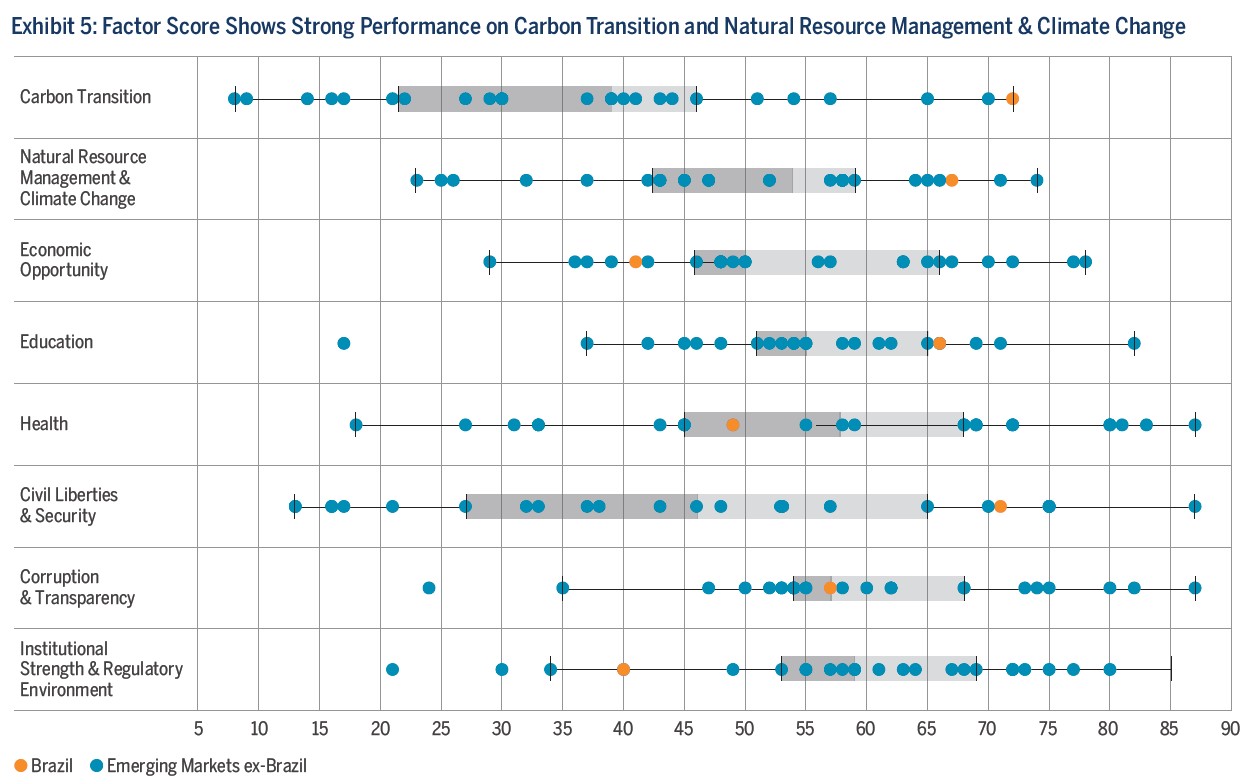

Examining the underlying data provides a better understanding of the drivers of a country’s overall performance as demonstrated in Exhibit 5 on the following page. Notably, the data shows Brazil as a top performer on Carbon Transition and Natural Resource Management and Climate Change; however, this is an example of how the quantitative data does not always tell an accurate story and where qualitative analysis is necessary to provide a more holistic understanding of the risks and opportunities.

Brazil has a relatively natural resource intensive economy, which presents challenges as it seeks to curb deforestation and mitigate the physical risks of climate change. In particular, Brazil is highly reliant on the agriculture sector as a leading commodity exporter (soybeans, sugarcane, corn, poultry, cotton, beef). In 2021, crop and livestock production accounted for 8% of GDP, but when factoring in processing and distribution, it is estimated that Brazil’s agriculture and food sectors accounts for closer to 29% of GDP (according to the U.S. Department of Agriculture).

Growth in this area over the last decade, combined with dismantling of environmental protections under Bolsonaro, has led to rapid deforestation in the Amazon as more land is cleared to be exploited for agricultural uses (primarily cattle ranching) for economic gain. Although Brazil has designated large swathes of land as protected (contributing to its top-quartile performance in this factor), protections are not enforced in practice and its natural resource depletion rate is very high. Under Bolsonaro, the government stopped enforcing environmental crimes almost entirely, and now has a backlog of 17,000 uncollected fines. In contrast, Lula oversaw a 70%+ decrease in deforestation during his previous two presidential terms, and since winning re-election has recommitted to doing so this time around as well.

In the short time since Lula won re-election, international support for the Amazon Fund from its primary donors, Norway and Germany, has come back after being suspended during the Bolsonaro administration. Additionally, the EU voted to ban the import of deforestation-linked products in September 2022, suggesting there will be an increasing price to pay for inaction. These are just a few examples of how Brazil’s focus on curbing deforestation can enable greater access to funding from both the public and private sectors. We believe these financial incentives will be critical to make the economic transformation needed to decouple growth from natural resource exploitation.

While environmental matters took a backseat under the Bolsonaro administration, we expect to see a heightened focus here under the new Lula administration. High unemployment and income inequality remain key social concerns, but a relatively high spend on education is supportive of economic growth outside of traditionally more natural resource intensive industries. Lastly, corruption remains a key governance risk under Lula, though we expect there to be heightened scrutiny and his powers somewhat muted given a more divided congress.

Note: The boxplot shows the distribution of the countries’ scores through displaying the data quartiles (or percentiles) and averages. The vertical bars indicate (from left to right) the minimum score, first (lower) quartile, median, third (upper) quartile, and maximum score. Blue circles show values for the different countries in the sample and the orange circle shows the value for Brazil. The area shaded in dark gray represents the second quartile and the area in lighter grey represent the third quartile, i.e., the data closer to the average. Source: World Bank (https://datatopics.worldbank.org/esg/), United Nations, World Health Organization, International Labor Organization, Food and Agriculture Organization, Transparency International, Freedom House, International Energy Agency, ND-GAIN index (https://gain.nd.edu/our-work/coun-try-index/) and Brown Advisory. Includes most recently available data as of July 21, 2022.

We are watching the evolution of Lula’s ministerial appointments closely to get a sense of how moderate (or not) his new administration will be. It has been a mixed bag so far —we are excited about his appointment of Marina Silva as Minister of the Environment and Climate Change given her long history as a champion for environmental causes, but have concerns about fiscal profligacy under Lula and his new Minister of Finance, Fernando Haddad. Increased social spending and subsidies have the potential to delay rate cuts from the Brazilian central bank which suggest that patience is warranted and clarity on policy demanded before owning Brazilian government debt. However, there may be opportunities to own corporate debt within Brazil to take advantage of strong commodity prices and improved balance sheets and valuations.

Our approach to analysing sovereigns is rooted in our three core tenets—integration of sustainability considerations into our fundamental research, focus on risks and opportunities and commitment to innovation— and draws on our extensive experience in fundamental analysis of corporate credit and government bonds.

CONCLUSION

Integrating research on sustainability-related risks and opportunities into sovereign debt analysis is the natural evolution of Brown Advisory’s global equity and fixed income sustainable investing platform. It also demonstrates our commitment to advancing the frontiers of sustainable investing.

Our approach to analysing sovereigns is rooted in our three core tenets— integration of sustainability considerations into our fundamental research, focus on risks and opportunities, and commitment to innovation—and draws on our extensive experience in fundamental analysis of corporate credit and government bonds. While our approach is consistent and systematic across asset classes and geographies, we believe it is flexible enough to capture the nuances that pertain to each country and the connections across and between different factors. Our qualitative analysis complements and enhances our quantitative data analysis to provide a true assessment and forecast of a sovereign’s current and future sustainability. ![]()

- Private debt may only be available to Qualified Purchasers or Accredited Investors.

- Bloomberg, World Countries Debt Monitor for developed markets and emerging markets as of 13/02/2023.

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results.

The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

All investments involve risk. The value of the investment and the income from it will vary. There is no guarantee that the initial investment will be returned.

Sustainable investment considerations are one of multiple informational inputs into the investment process, alongside data on traditional financial factors, and so are not the sole driver of decision-making. Sustainable investment analysis may not be performed for every holding in the strategy. Sustainable investment considerations that are material will vary by investment style, sector/industry, market trends and client objectives. The Global Sustainable Total Return Bond Strategy (“Strategy”) seeks to identify issuers that it believes may be desirable based on our analysis of sustainable investment related risks and opportunities, but investors may differ in their views. As a result, the Strategy may invest in issuers that do not reflect the beliefs and values of any particular investor. The Strategy may also invest in issuers that would otherwise be excluded from other funds that focus on sustainable investment risks. Security selection will be impacted by the combined focus on sustainable investment research assessments and fundamental research assessments including the return forecasts. The Strategy incorporates data from third parties in its research process but does not make investment decisions based on third- party data alone.

Reference to income inequality is according to the Gini index which measures the extent to which the distribution of income or consumption among individuals or households within an economy deviates from a perfectly equal distribution. A Gini index of 0 represents perfect equality, while an index of 100 implies perfect inequality.