For investors focused on sustainability, labeled bonds can represent a powerful opportunity to pursue positive environmental or social change while also earning attractive fixed income returns. However, with the tremendous growth in the labeled bond market and the proliferation of new and innovative financing structures, it has become all the more critical to conduct in-depth due diligence in order to ensure that labeling does not lose its impact. Moreover, integrating ESG factors into the fundamental research process is important to mitigate and appropriately price risk. If properly vetted, labeled bonds can be an attractive investment and a powerful tool to finance the fight against climate change and create a more equitable world.

Fixed income offers a compelling structure for investors who value sustainability, as it permits tracing and quantifying an investment’s environmental and/or social impact. The opportunity set for global sustainable fixed income investing comprises a large and growing amount of debt issued by companies, governments and other entities committed to sustainable practices. The growth of this opportunity set has been so tremendous over the past few years that it deserves an encore to our 2018 piece Income and Impact: Adding Green Bonds to Investment Portfolios.

A segment of the global sustainable fixed income market—the labeled bond market—articulates sustainability goals explicitly, either by earmarking proceeds or linking the structural characteristics of their bonds to predefined sustainability/environmental, social and/or governance ESG objectives. The growth in this space is particularly appealing to investors seeking to make a positive impact, but it is important to note that it comes with immense challenges, namely a lack of standardization and independent verification of said labels, in the absence of which incentives for greenwashing (or mislabeling) may prevail. While appealing, bond labels are no shortcut for the prudent investor. Proper due diligence continues to be crucial to assess the validity of bond labels. Furthermore, it is important to note that a proper due diligence and analysis on the issuer and of the use of proceeds may uncover that other, unlabeled bonds may ultimately have equal or larger impact on global sustainability, even though they do not carry a label.

THE ‘GREEN, SOCIAL AND SUSTAINABLE’ RUSH

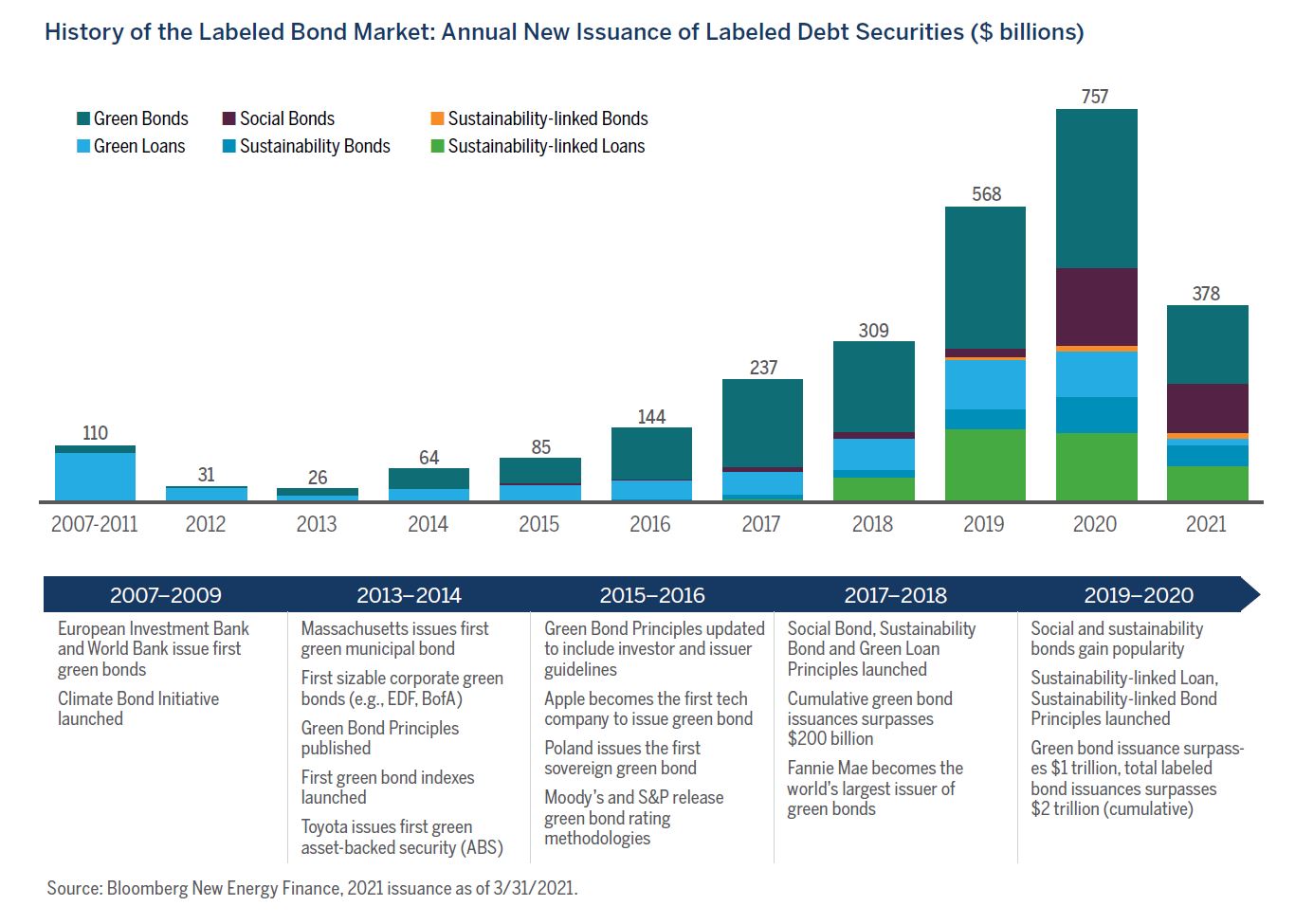

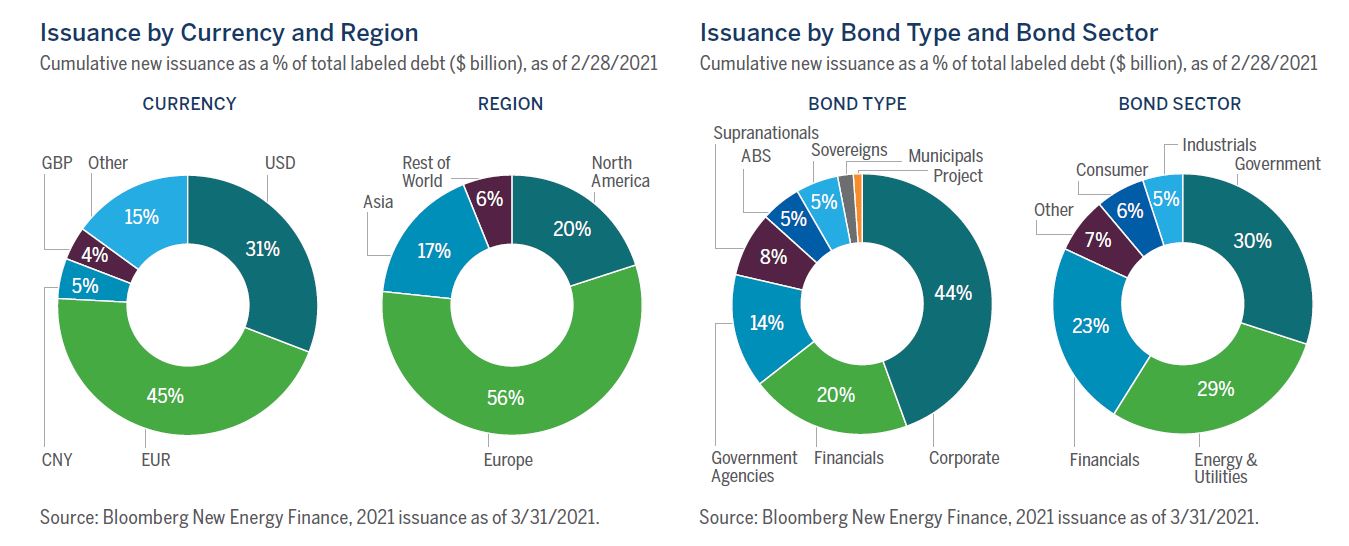

The size and composition of fixed income instruments geared to raise capital for sustainability-related matters continues to grow exponentially. As climate change has garnered increasing attention, the green bond market has surged, surpassing $1 trillion in total issuance in 2020. Moreover, a host of new labels has emerged in addition to the green label as social issues have come to light. In total, the global sustainable debt market surpassed $2 trillion in total issuance in 2020 and comprises a diverse opportunity of green, social and sustainability bonds, as well as emerging labels, such as sustainability-linked bonds. Green, social and sustainability bonds, and green loans’ labels are directly connected to the use of proceeds explicitly stated by the issuer and are earmarked to specific projects (dedicated purpose financing). Instead, the proceeds of sustainability-linked bonds and loans are not earmarked but connected to issuer green/ social key performance indicators (KPIs) and performance (general purpose financing). Sustainability-linked bonds and loans offer a mechanism to hold the issuer accountable if they do not achieve their stated sustainability goals—usually through a one-time stepup in coupon rate if the sustainability performance target (SPT) has not been achieved by the designated date.

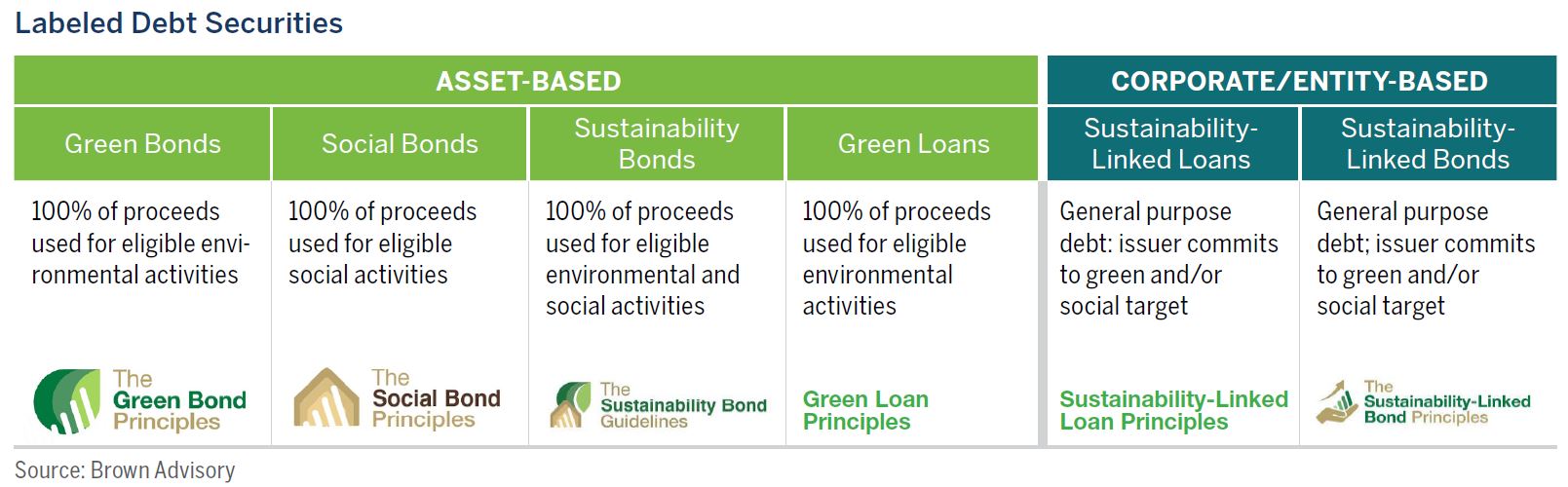

TYPES OF LABELED DEBT SECURITIES

Green Bonds. All of the proceeds are allocated to specific environmental projects, including renewable energy, environmentally sustainable management of living natural resources and land use, clean transportation, sustainable water and wastewater management, climate change adaptation, production technologies and processes, and green buildings. Blue Bonds are another label used for bonds financing marine and oceanbased projects.

Social Bonds. All of the proceeds are allocated to address or mitigate a specific social issue and/or seek to achieve positive social outcomes, including affordable basic infrastructure (e.g., clean drinking water, sewers, sanitation, transport, energy); access to essential services (e.g., health, education and vocational training; health care; financing and financial services); affordable housing; employment generation, including through the potential effect of small and medium enterprise financing and microfinance; food security; socioeconomic advancement; and empowerment.

Sustainability Bonds. All of the proceeds are allocated to a combination of environmental and social projects.

Sustainability-linked Bonds. A forward-looking performancebased bond instrument for which the financial and/or structural characteristics can vary depending on whether the issuer achieves predefined sustainability/ESG objectives. The sustainability- linked bond structure can be an effective way for issuers to procure financing for general purposes according to their overarching sustainability strategy. These may also be called SDGlinked bonds in reference to the UN Sustainable Development Goals (SDGs).

With this growth, we have seen great diversification along multiple dimensions, as the emergence of new labels has expanded the scope of eligible projects and bond structures. For instance, green bonds had traditionally been popular instruments for power utilities and REITs, where there are clearly defined projects and capital expenditures are large. Now, the sustainability-linked bond label, while still nascent, offers an alternative for issuers that are interested in aligning their bond issuance with an overarching sustainability strategy without having to earmark specific use of proceeds. Additionally, while social issues had typically taken the backseat in sustainable investing, they garnered tremendous attention more recently. In 2020, we saw a proliferation of social projects as COVID-19 and a focus on racial injustice shed light on the societal gaps that could be addressed by various entities. Sustainability bonds, too, have proved to be an important instrument for issuers that are operating at the intersection of environmental and social impact (e.g., improving the energy efficiency of affordable multifamily housing units), and those that may not have enough of either green or social projects to warrant standalone benchmark size issuances. The growth of new labels has created a dynamic and diverse opportunity set for investors to have tangible impact across a myriad of issues and sectors across the globe.

IS IT TOO EASY TO BE GREEN, SOCIAL OR SUSTAINABLE? DO DUE DILIGENCE!

Amid a rush for sustainable or green investments, what makes a bond green, social or sustainable may determine an issuer’s access to and cost of capital. Thus, the growth of the space, coupled with a not-yet-fully-developed set of criteria, enforcement and transparency in itself, has ultimately set up perverse incentives for greenwashing, or the practice whereby, due to the growing popularity in the space, issuers claim their debt is green, social and/or sustainable when it is not.

With the exception of blatantly dishonest practices where green, social and/or sustainable is nothing more than an unsubstantiated claim (or maybe minimal compliance with required criteria to obtain a label), greenwashing is a far more nuanced issue. Are instruments financing the purchase of offsets or renewable energy credits greenwashing? Is a bond financing a one-off renewable energy project truly connected to the overarching sustainability strategy of an issuer? What about issuers raising capital to finance their transition from high-emitting, hard-to-abate sectors, like in the oil and gas sector?1 Are bonds used to finance procurements from diverse suppliers truly generating meaningful social impact?

While the ICMA Principles2 provide guidelines for the issuance of labeled bonds, it must be noted that adherence to these is purely voluntary and the principles are not comprehensive, still leaving room for plenty of subjectivity as it relates to defining what is green, social or sustainable. Furthermore, adherence and compliance with the criteria are largely determined by issuer and/or underwriter, posing a conflict of interest. A number of external reviews and certifications3 have emerged to help provide credibility to the market and ensure alignment with the ICMA Principles, and the development of the EU Green Bond Standard seeks to define more specifically what classifies as green, but this is largely work in progress. Generally, we are supportive of the development of more robust standards to the extent that it increases transparency among issuers, but we ultimately believe that it is up to the investor to determine what meets their criteria for green, social or sustainable debt.

In our view, labeled bonds require the same level of due diligence as nonlabeled bonds, a due diligence that comprises both the issuer and the use of proceeds (earmarked or not) and KPIs (if any). In addition, we conduct ESG risk management and sustainable opportunity assessments at the issuer level, where we look to see how the use of proceeds fits into the issuer’s overarching strategy and capital expenditure planning. From a risk perspective, while labeled bonds may be an obvious choice for sustainable investors, most are actually unsecured obligations that are equal to the issuer’s other outstanding debt. It is therefore critical to also conduct issuer-level ESG and credit analysis. From an opportunity perspective, for a power utility issuing a green bond to finance a renewable energy project, we must see how that project fits into its broader goals for transitioning its energy mix toward more renewable sources—it can’t just be a oneoff project. While as of the writing of this publication, we have yet to participate in a sustainability-linked bond, we follow a similar approach, seeking to understand how the bond issue fits into the issuer’s overarching sustainability strategy and assessing the materiality of the chosen sustainability performance targets to its core operations/offerings and the ambitiousness of the stated goal.

While we do take into account external reviews and certifications in our analysis, we believe our own in-depth due diligence is required in order to ensure that labeling does not lose its impact. This will continue to be of utmost importance as the labeled bond market grows and expands into new and innovative financing structures.

LABELED BONDS AND BEYOND

At Brown Advisory, we strongly believe that an investor can best achieve income and impact goals by combining proper due diligence on sustainability with thorough fundamental credit analysis. We think integrating ESG factors into our fundamental research process enhances our efforts to mitigate and appropriately price risk in the bonds we evaluate (see Income and Impact, 2018).

While labeled bonds continue to grow and develop into a more mature global sustainable debt market, it is imperative that we, as investors, peel those labels by putting them through a thorough due diligence process. For investors focused on sustainability, labeled bonds can represent a powerful opportunity to pursue positive environmental or social change while also earning attractive fixed income returns.

Overall, we expect the momentum in this space to not only continue, but to also accelerate. If anything, the COVID-19 pandemic served as a proof point of why we need to focus on some of the social factors that may have been previously overlooked and not thought of as material financial risks. As a result, we might continue to see more social and sustainability bonds being issued to combat inequality. We also expect to see a heightened focus on climate change. We have seen a lot of companies and governments double down on their commitments to address climate change. In 2020, we saw Japan, South Korea and Canada commit to net zero by 2050, and China net zero by 2060. We also saw large corporations like General Mills, Facebook, BP and Shell make net zero by 2050 commitments. While this is an encouraging first step, we know that these commitments will need to be followed with significant investment in order to achieve these goals, and we believe the fixed income market is going to play a central role in financing these initiatives. We want to help support that transition by lending money to those issuers committed to the fight against climate change and a more equitable world. ![]()

- The concept of “Transition” bonds is emerging as companies from high-emitting, hard-to-abate sectors seek to issue ESG-labeled bonds to finance their transition, but do not want to be perceived by the market as “greenwashing”. ICMA has released the Climate Transition Finance Handbook in 2020 to set some high-level guidelines.

- ICMA is the secretariat that oversees the Green Bond Principles (GBP), Social Bond Principles (SBP), Sustainability Bond Guidelines (SBG), and the Sustainability-Linked Bond Principles (SLBP). The four key components for Green, Social, and Sustainability Bonds, according to the ICMA Principles are: use of proceeds, process for project evaluation and selection, management of proceeds and reporting. Given the different structure of Sustainability-Linked Bonds (a focus on KPIs rather than specific use of proceeds), the five key components are: selection of KPIs, calibration of sustainability performance targets (SPTs), bond characteristics, reporting and verification.

- External reviews and certification available include: (1) Third Party Assurance: independently verified against a set of criteria, typically performed by audit firms, e.g., KPMG , Deloitte; (2) Second Party Opinions: independently reviewed by institutions with specific ESG expertise, e.g., Sustainalytics, Vigeo Eiris, CICERO; (3) Ratings: independently scored against a third-party scoring/rating methodology, e.g., Moody’s, S&P; and (4) Certifications: independently certified against a recognized external standard or label, e.g. Climate Bonds Initiative (CBI) developed the Climate Bond Standard, which is aligned to Green Bond Principles, but uses rigorous scientific criteria to ensure that it is consistent with the 2 degrees Celsius warming limit in the Paris Agreement.

The views expressed are those of Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested.

The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client. All investments involve risk. The value of the investment and the income from it will vary. There is no guarantee that the initial investment will be returned. ESG considerations that are material will vary by investment style, sector/industry, market trends and client objectives. Our strategies seek to identify companies that we believe may have desirable ESG outcomes, but investors may differ in their views of what constitutes positive or negative ESG outcomes. As a result, we may invest in companies that do not reflect the beliefs and values of any particular investor. Our strategies may also invest in companies that would otherwise be screened out of other ESG-oriented funds. Security selection will be impacted by the combined focus on ESG assessments and forecasts of return and risk. Our strategies intend to invest in companies with measurable ESG outcomes, as determined by Brown Advisory, and seek to screen out particular companies and industries. Brown Advisory relies on third parties to provide data and screening tools. There is no assurance that this information will be accurate or complete or that it will properly exclude all applicable securities. Investments selected using these tools may perform differently than as forecasted due to the factors incorporated into the screening process, changes from historical trends, and issues in the construction and implementation of the screens (including, but not limited to, software issues and other technological issues). There is no guarantee that Brown Advisory’s use of these tools will result in effective investment decisions. BLOOMBERG, is a trademark and service mark of Bloomberg Finance L.P., a Delaware limited partnership, or its subsidiaries.