Amboy, California – or what’s left of it – sits in the eastern Mojave Desert in San Bernardino County, about 200 miles northeast of Los Angeles. In the mid-20th century, a period defined in America as the “Golden Age” of road trips, the town became a popular stop along Route 66 which ran from the Great Lakes to the Pacific Ocean. With hundreds of permanent residents and numerous tourists stopping for fuel and a bite at Roy’s Café, Amboy was a thriving town with a main street, serving as a lively desert crossroads.

Source: City of Amboy, California

Today, all that’s left of Amboy is the iconic Roy’s neon sign from yesteryear, cracked asphalt and empty sun-bleached buildings. The town no longer has any permanent residents. The strong scent of gasoline and burger grease now a faint memory, Roy’s is now a gift shop filled with memorabilia of a town time left behind.

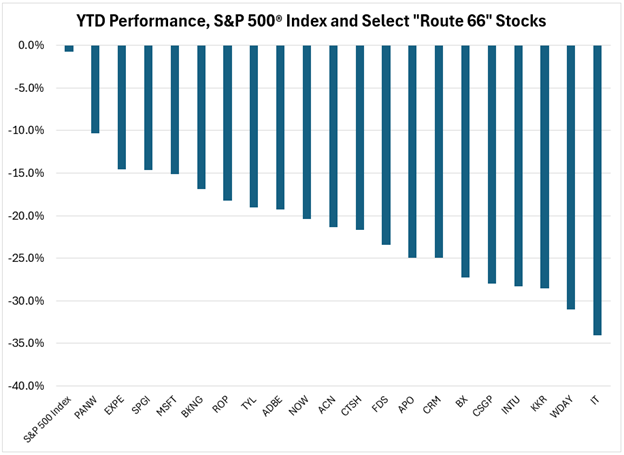

Investors can relate to the story of Amboy. Parallels can be drawn to legacy media and cable stocks, office real estate investment trusts (REITs) during the height of hybrid work trends, and traditional brick-and-mortar retailers that haven’t established omnichannel strategies. More recently, the release of next-generation AI large language models (“LLMs”) optimized for code generation, reasoning and agentic workflows have pushed several groups of stocks to the brink of abandonment. Models like Anthropic’s Claude Opus 4.6 and OpenAI’s GPT – 5.3 – Codex, both released in early February, have the potential to automate certain cognitive tasks traditionally employed by specialized software tools, professional and information services companies, and enterprises that extract and analyze data.

Many investors have concluded that these powerful AI agents could replace large amounts of white-collar work, leaving certain companies obsolete or at least economically pressured. SaaS/enterprise software companies like Workday and Salesforce, IT consulting firms like Accenture and Cognizant, and data-heavy information services companies like S&P Global and FactSet Research Systems saw investors desert their stocks during the first several weeks of 2026 in similar fashion to residents departing Amboy about 50 years ago.

Note: Data as of March 9, 2026

Source: FactSet®. Please see the end for stock names.

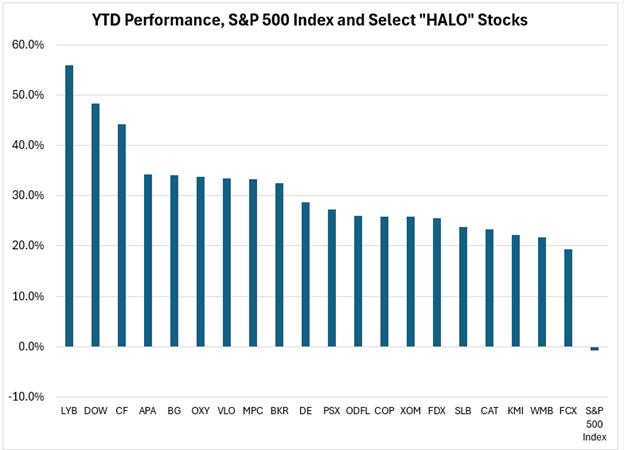

At the same time, investors have clamored into stocks that literally carry a “HALO” effect – an acronym for “heavy assets, low obsolescence”. As opposed to asset light businesses that are perceived as “at-risk” from AI development and deployment, these more capital-intensive Energy, Materials and Industrials companies are viewed as safe from agentic AI disintermediation.

Note: Data as of March 9, 2026

Source: FactSet®. Please see the end for stock names.

Risks to “HALO” Stocks

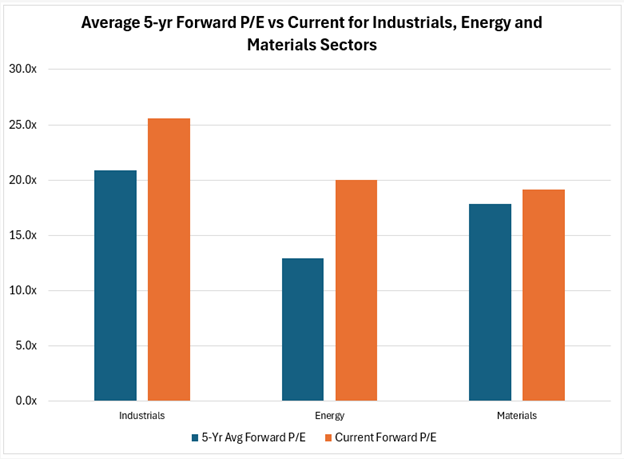

Before we cruise towards “Route 66” stocks, I’d like to provide a few datapoints that describe how crowded conditions have become within the HALO group. The Industrials S&P sector ETF, also known as the “XLI”, currently trades near an all-time high on forward P/E at 26x. At the beginning of March, oil major Exxon unusually traded in-line with cloud service provider Microsoft on forward P/E for the first time since the pandemic. Deere, a global manufacturer of agricultural and construction equipment, trades at nearly a ten-point P/E premium to S&P Global after spending the past decade at a discount to this leading ratings and financial intelligence company. Never mind that companies in economically sensitive sectors – there’s a reason they are known as “cyclicals” – carry significant earnings volatility in the event GDP growth recedes. Historically, the combination of elevated valuations and high earnings expectations in cyclical sectors creates reason to pause.

Note: Data as of March 9, 2026

Source: FactSet. Sectors are based on the Global Industry Classification Standard (GICS ®) classification system.

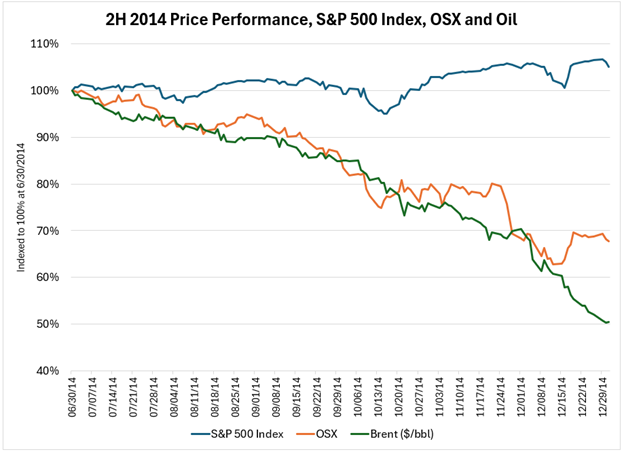

Look no further than the PHLX oil service sector index (“OSX”), which enjoyed its own HALO moment in mid-2014. Oil prices had traded in the elevated range of $100-$120/bbl for the prior few years driven by tight supply/demand conditions and geopolitical risk. Investors and upstream financiers were lulled into believing this was the “new normal” range for oil prices, supporting favorable economics for virtually all oilfields, everywhere. It led to global upstream oil and gas capital spending of almost $900 billion according to industry consultant Rystad Energy (remains “peak spend” for the industry), as well as heightened utilization and pricing power for the oil service industry. In June 2014 the OSX traded at about 17x P/E, a 10% premium to the less cyclical and broader S&P 500® Index. By the end of 2014 the price of oil had been nearly cut in half, driven by weaker global demand, the surprising growth of U.S. shale output, and a new Organization of the Petroleum Exporting Countries (OPEC) strategy to defend market share rather than price. Within six months, forward earnings-per-share (EPS) estimates for the Index declined by more than 20%, while its P/E multiple fell roughly 20%. The OSX lost nearly a third of its value in the second half of 2014, while the S&P 500 Index rose 5% during that period.

Note: Data from June 30, 2014 – December 31, 2014

Source: FactSet®.

Could this time be different? Sure. Further advancements in agentic AI could broadly support SG&A efficiencies, while physical or robotic AI innovation could reduce manufacturing costs for heavy asset companies. However, we are referencing a deflationary scenario, one in which companies that sell commodities or physical products would have fewer constraints on productive capacity along with lowering the cost of production, creating the potential for oversupply and price competition. Investors have cast away asset-light, information-advantaged service businesses rather uniformly in recent weeks on the premise that one cannot disprove the narrative that AI will eat into their economic profits at some point in the future. Can’t the same be said of the HALO group based on this logic? Perhaps the Interstate Highway System just hasn’t reached these towns yet.

Bargain Hunting Along Route 66

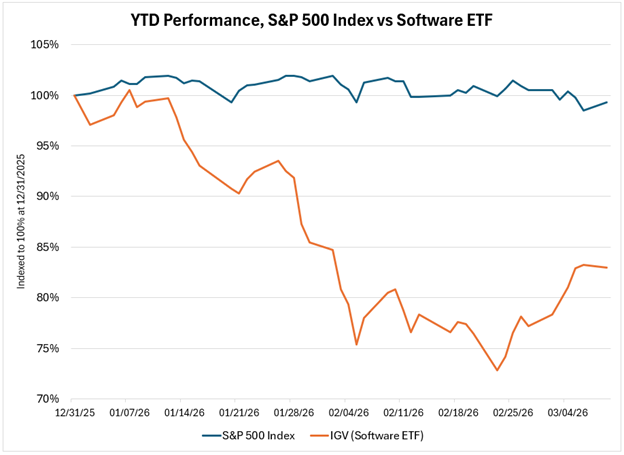

Two events seemed to mark the end (for now) of what’s become affectionately known as the “SaaSpocalypse” – the sudden obsolescence of software and related industries. Anthropic hosted an Enterprise Agents event on February 24th, which highlighted how Claude is positioned to play the role of “thinking partner” for software incumbents rather than disruptor. Then on February 25th, NVIDIA’s CEO Jensen Huang shared that markets “got it wrong” on AI’s threat to software companies. Since the Anthropic event, we’ve seen the IGV (software-sector ETF) bounce back 14%, although it remains -17% for the year.

Note: Data as of March 9, 2026

Source: FactSet®.

Our team has spent countless hours considering the potential disruption that AI advancements may have on individual stocks, sectors and the economy more broadly. We admit that it is impossible to know how this trend eventually plays out. We anticipate future new LLM announcements and exciting use cases that could continue the dystopian narrative for asset light, knowledge-based business models. However, investors who have rather uniformly abandoned “Route 66” stocks are not giving credit to management teams’ ability to adapt to new technology, nor barriers to change including ownership of proprietary data, operating in heavily regulated industries, and human touch. We’ve been selectively adding names and increasing positions in “Route 66” stocks during the sharp sell-off. While recognizing there could be intermittent volatility, we hypothesize that some, if not many of these stocks offer tremendous upside potential for the long-term investor.

“Come what may, it’s our town.” – James Taylor

Thanks for reading, and remember to never skip a Beat – Eric

Source: FactSet®. FactSet is a registered trademark of FactSet Research Systems, Inc.

Stocks: Palo Alto Networks Inc (PANW), Expedia Group Inc (EXPE), S&P Global Inc (SPGI), Microsoft (MSFT), Booking Holdings Inc (BKNG), Roper Technologies Inc (ROP), Tyler Technologies Inc (TYL), Adobe Inc (ADBE), ServiceNow Inc (NOW), Accenture Plc, Cognizant Technology Solutions Corp (CTSH), Factset Research Systems Inc (FDS), Apollo Global Management Ord Shs (APO), Salesforce Inc (CRM), Blackstone Inc (BX), CoStar Group Inc (CSGP), Intuit Inc (INTU), KKR & Co Inc (KKR), Workday Inc (WDAY), Gartner Inc (IT), LyondellBasell Industries NV (LYB), CF Industries Holdings, Inc. (CF), APA Corp (US) (APA), Bunge Global ltd (BG), Occidental Petroleum Corp (OXY), Valero Energy Corp (VLO), Marathon Petroleum Corp(MPC), Baker Hughes Co (BKR), Deere & Co (DE), Phillips 66 (PSX), Old Dominion Freight Line Inc (ODFL), ConocoPhillips (COP), Exxon Mobil Corp (XOM), FedEx Corp (FDX), Slb NV (SLB), Caterpillar Inc (CAT), Kinder Morgan Inc (KMI), Williams Companies Inc (WMB) and Freeport-McMoRan Inc (FCX).

Source: FactSet®. FactSet is a registered trademark of FactSet Research Systems, Inc.

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

An investor cannot invest directly into an index.

The S&P 500® Index is a capitalization weighted index of 500 stocks that is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. Index returns assume reinvestment of dividends and do not reflect any fees or expenses. Benchmark returns are not covered by the report of the independent verifiers. Standard & Poor’s, S&P®, and S&P500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a subsidiary of S&P Global Inc.

Forward P/E Ratio is determined by dividing the price of the stock by the company's forecasted earnings per share.

The PHLX Oil Service Sector Index (OSX) is a modified market capitalization-weighted index that measures the performance of 15 U.S. companies involved in the oil services industry, such as drilling, production, and equipment.

Earnings per share (EPS) is calculated as a company's profit divided by the outstanding shares of its common stock.