Charlie Munger, masterclass investor, rational thinker and Warren Buffett’s right-hand man, died in late November only a few weeks prior to becoming a centenarian. Munger and Buffett amassed an investment track record that can only be described as a ‘tour de force’. While partnered at Berkshire Hathaway (1978-2023), the two Omaha natives saw their company’s shares climb by nearly 20% per year, about 900 basis points ahead of the S&P 500® Index, annualized. If you had invested $10,000 in Berkshire at the beginning of 1978 and left it untouched, you’d have about $40 million today. Excluding dividends, a $10,000 investment in the S&P 500 Index in 1978 would be worth less than $500,000 today.

In his final interview Munger was asked to reveal the secret to both his longevity and success. The response was simple but brilliant. “Crazy is way more common than you think. It’s easy to slip into crazy. Just avoid it, avoid it, avoid it.”

As we approach the end of 2023, it’s once again the season for festive decorations, office holiday parties…and Wall Street forecasts for the S&P 500 Index for the next calendar year. While Munger would certainly have suggested avoiding crazy behavior at year-end celebrations, he might also have questioned the rationality of annual market prognostications that garner such close attention of investors and news outlets. Publishing a single point estimate that attempts to account for so many anticipated and even more unforeseen events that impact equity prices over a 12-month period goes in the “too hard” bucket in my opinion.

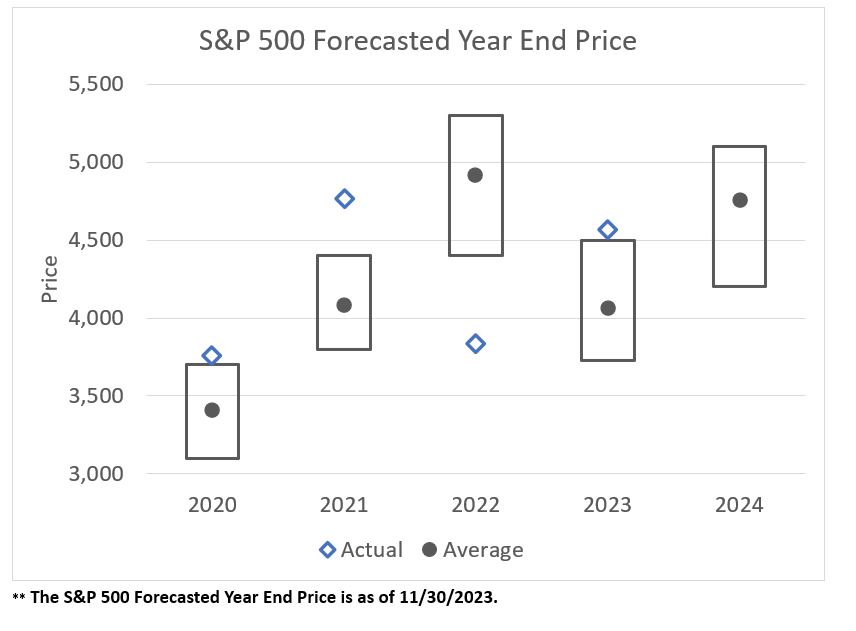

Note: Wall Street firms included in the estimates are Bank of America, Barclays, BMO, Deutsche Bank, Goldman Sachs, JP Morgan, Morgan Stanley and UBS.

Source: FactSet and Bloomberg.

Data as of November 30, 2023

In each of the past four years, the year-end price of the S&P 500 Index has not even been bracketed by the range of these Wall Street forecasts made 12-months prior. The closest the average estimate came to the actual year-end Index price was in 2020, at nearly 10% below the actual result. While this might sound critical, in reality no one could blame these firms’ forecasts for being so far off. Who could have possibly predicted the market’s undulations over the past few years; the pandemic, the ensuing fiscal and monetary response, the rapid increase in valuation multiples, the subsequent and equally rapid compression of valuation multiples, and more recently the incredibly narrow market leadership driving Index concentration to levels never experienced before?

Turning to 2024, there are several known unknowns that are in focus for investors. With inflation in decline and unemployment slowly climbing, (when) will the Fed begin cutting rates? Can the U.S. consumer maintain its surprising resilience? Will geopolitical conflicts lead to unknown economic consequences? Can China regain investors’ confidence? Will investors remain inebriated by the promise of Generative AI, or will they demand that companies demonstrate immediate growth acceleration? Will additional data on the effectiveness of GLP-1s create a broader set of associated winners and losers in the equity market? Will the U.S. presidential election directly or indirectly impact equity markets in the coming year? Will the Magnificent Seven continue to lead a very narrow market, or will the prospect of a new economic cycle broaden out the set of winners, creating a more favorable stock pickers’ market? Beyond these questions, there will almost certainly be a set of additional, unexpected events that create market volatility, possibly trumping the known unknowns in importance.

Despite tremendous uncertainty facing investors at the beginning of 2023, the S&P 500 Index has generated a total YTD return (through November) of nearly 21%; with just seven companies in the Index contributing nearly three-quarters of the return. The Magnificent Seven have captured the hearts, minds and wallets of public equity investors this year, as these companies carry strong competitive advantages, are beneficiaries of secular trends including in many cases Generative AI and have pristine balance sheets. Yet, at current valuations, one must consider whether other quality companies could offer more favorable risk-reward opportunities.

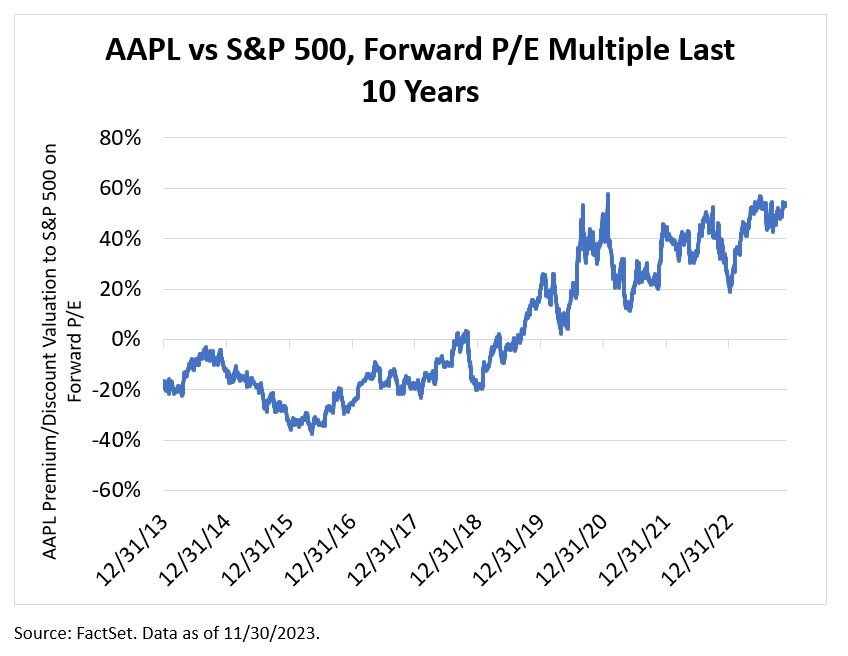

Apple (AAPL), the largest company by market cap among the Magnificent Seven (recently eclipsing $3 trillion in market value), has experienced nearly 40% P/E multiple expansion during 2023 (trading at 29x forward as of end November). The median change in P/E for all S&P 500 Index constituents this year is slightly negative. The stock trades at more than a 50% premium to the broader market on forward P/E, versus an average premium of just 4% over the past ten years. Is the current level of premium valuation approaching “crazy”? Ironically, AAPL is Berkshire Hathaway’s largest stock position by far, valued at about $175 billion. Sadly, it’s too late to ask Munger for his thoughts on the topic.

Munger’s advice to “avoid crazy”, translated into security analysis is largely to avoid the avoidable mistakes. Be aware of what you don’t or can’t know. Don’t make the same mistakes in repetition. Invest in what you know. Invest like you own the business (because you do). Read incessantly to gain knowledge that can help you build mental models and invest more methodically. Invest in quality businesses that have greater control over their destiny than others – less can go wrong (in theory).

In truth, there is no silver bullet, short list or simple catchphrase that can help us deliver Buffett and Munger-like returns. Their investment track record in terms of both performance and longevity may never be seen again, regardless of improvements in AI. However, by establishing process and a consistent philosophy, we can stay within the guardrails of sanity long enough to make more positive investment decisions for clients than the alternative.

Rest in peace, Charlie. And thank you for sharing your genius with us.

Charles Thomas Munger (January 1, 1924 – November 28, 2023)

Thanks for reading, and remember to never skip a Beat - Eric

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

Terms and Definitions:

The S&P 500® Index, an unmanaged index, consists of 500 stocks chosen for market size, liquidity, and industry group representation. It is a market-value weighted index (stock price times number of shares outstanding), with each stock's weight in the Index proportionate to its market value.

Standard & Poor’s, S&P®, and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a subsidiary of S&P Global Inc.

All financial statistics and ratios are calculated using information from FactSet as of the report date unless otherwise noted. FactSet® is a registered trademark of FactSet Research Systems, Inc.

Earnings per share (EPS) is a measure of a company's profitability, calculated by dividing quarterly or annual income (minus dividends) by the number of outstanding stock shares. The higher a company's EPS, the greater the profit and value perceived by investors.