At Brown Advisory, we often describe ourselves as “bottom-up” investors. That means we tend to focus more on stock selection conviction—in other words, understanding companies “from the bottom up”—and less on “top-down” concepts like sector allocation or broader macroeconomics.

But we never forget that we manage diversified portfolios, and those portfolios are indeed affected by macro factors; inflation, interest rates, bank liquidity and other issues facing the economy will of course influence the prospects of the companies we hold in our strategies.

Two recent examples: First, the March banking crisis appears to be contained for now, but I am loathe to even speak those words for fear of jinxing a recovery. Bank stocks seem to have bottomed (at least in the short-term), leaving the second- and third- largest bank failures in U.S. history in their wake after those banks unraveled with a speed that shocked most observers. Second, OPEC announced on April 1 that it would cut production by more than a million barrels per day; unfortunately, it was not an April Fools’ joke, and neither was the subsequent news that the new targets would remain in place through 2023. While this buoyed energy markets, it renewed palpable fears of prolonged inflation across the broader economy and investment community.

Both of these scenarios will likely have far-reaching impacts across many sectors of the economy, and will factor into the performance of many companies. To tackle these kinds of questions, our portfolio managers—who, as noted, generally focus on bottom-up fundamental research—have developed a variety of methods and perspectives for “bringing the macro” into their decisions.

FROM BOTTOM TO TOP

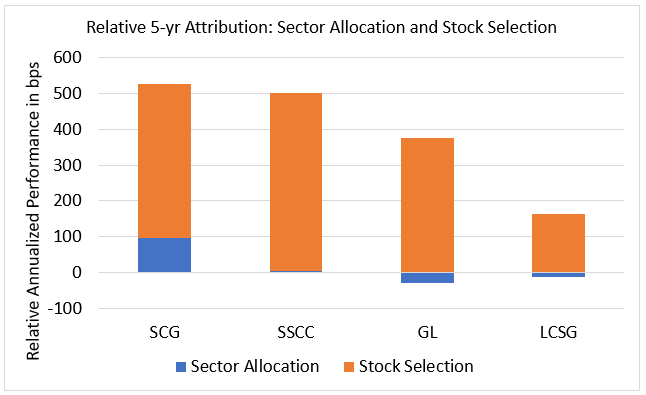

When our strategies have demonstrated relative outperformance over time, generally that outperformance has been driven more by stock selection (the “bottom-up” factor) than by sector allocation (the “top-down” factor). The below chart illustrates how this has played out for four of our strategies, over the past five years:

Note: Data is based on Representative Account Performance during the period ended 3/31/2023, and is calculated based on gross of fees attribution and ex-cash.

Source: FactSet

Yet none of these portfolio managers could truly succeed if they completely avoided top-down analysis of macro factors—first, second and even third derivative impacts of central bank policy decisions, geopolitics and many other issues are important for their portfolios.

Our portfolio managers differ in how they incorporate “the macro” into their thinking on portfolio construction, although there are points in common.

- David Powell and Karina Funk (Large Cap Sustainable Growth) approach macro risk through a combination of high standards for business quality, position size management and having a clear upside and downside target on each holding. The strategy is currently invested ~65% in what the PMs view as durable and less cyclical businesses, and 35% in more rapidly growing and less mature business models.

- Priyanka Agnihotri (Sustainable International Leaders) watches macroeconomic data points closely in an effort to understand where we are in a particular economic cycle. She considers that information when, for example, she is deciding whether to add to a position or trim it. However, the strategy primarily focuses on business quality, and she seeks to invest in companies that she believes can hold up well under a range of economic scenarios.

- Chris Berrier (Small Cap Growth) tends to maintain a lower-beta portfolio, which is an outcome of his preference for higher-quality business models. He likes to think of macro scenarios in terms of probabilities—do I think this scenario is more/less likely than the market seems to think?—and that has helped prioritize incremental capital allocation decisions.

- George Sakellaris (Mid-Cap Growth) utilizes the takeaways from the team’s hundreds of company management discussions each year as a way to build a macro view across various industries. This approach helps the strategy formulate opinions on many different subsectors, each of which may be subject to its own, asynchronous cyclical pattern.

- Maneesh Bajaj (Flexible Equity) uses a combination of the ideas mentioned above and emphasizes the element of human behavior in his thinking about macro factors. He believes that by successfully interpreting how people will internalize short-term data points and how they will react—out of fear, greed or other emotions—he can identify some of the buying/selling opportunities that flow from those human reactions.

While our managers build portfolios and deliberately set the size of each position in that portfolio, analysts are tasked with assessing the upside and downside potential of individual companies over a multiyear time horizon. This exercise requires analysts to identify which macro variables will likely have the greatest influence on a company’s fundamentals and evaluate the extent of positive and negative potential outcomes in best- and worst-case macro scenarios.

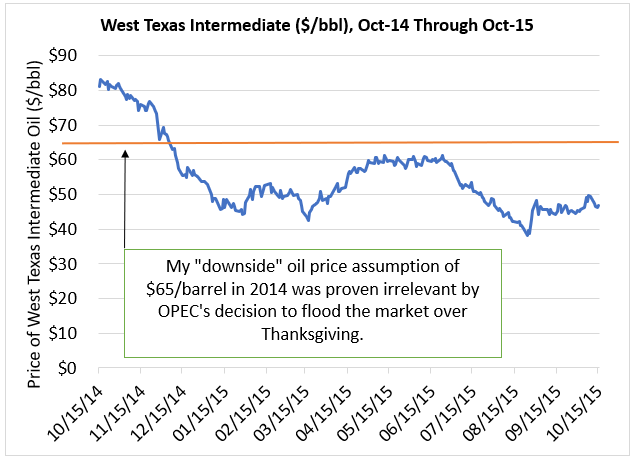

This is, of course, easier said than done. Happily, I can use myself as a handy illustration. Earlier in my career, I was Brown Advisory’s energy analyst, and during one stretch in the mid-2010s, I consistently used a downside oil price scenario of $65/barrel as a “floor” below which marginal wells would no longer make sense to operate. I even initiated coverage on an oil producer in October 2014, with a downside target predicated on that $65 floor. Unfortunately, in November OPEC chose to meet declining oil prices by MAINTAINING production, not cutting it as it had so many times over the years; this decision sent oil prices plummeting--and my downside target for that oil producer into the trash.

Source: FactSet (10/15/2014-10/15/2015)

At our firm, we very much appreciate the mindset of investors who claim to be entirely focused on bottom-up fundamentals; as noted that is where we try to spend the bulk of our research time as well. But I suspect that every investment ever made has been informed by some amount of macro “forecasting”—whether those forecasts were sophisticated financial models or simply manifestations of fear about grocery prices.

Our macroeconomic crystal ball is just as cloudy as everyone else’s (if you ever hear someone tell you they know what’s going to happen in the market, we would recommend that you run away), but we nonetheless work hard to analyze the primary macro factors that may help (or harm) the earnings prospects of each of our holdings. Sometimes, shocking external events emerge, such as the sudden demise of banks, global pandemics, or military invasion, and our analyses need to be recalibrated. This effort--a combination of art, science and a healthy portion of humility—gives us a stable aperture through which we can view the macro while remaining true to our bottom-up research process.

Thanks for reading, and remember to never skip a Beat - Eric ![]()

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

Factset® is a registered trademark of Factset Research Systems, Inc.

Small Cap Growth strategy, (SCG) The strategy invests primarily in the common stock of small domestic companies possessing what the portfolio managers see as above-average growth potential based on in-depth fundamental analysis.

Sustainable Small Cap Core strategy (SSCC) The strategy’s investing approach seeks outperformance through a concentrated, low-turnover portfolio of companies.

Global Leaders strategy (GL) The strategy will invest in equity securities of companies that the portfolio managers believe are leaders within their industry or country, as demonstrated by an ability to deliver high relative return on invested capital over time.

Large Cap Sustainable Growth strategy (LCSG) The strategy seeks long-term capital appreciation by investing in the common stock of mid- and large-cap companies that, in the manager’s view, effectively implement sustainable business strategies to drive their prospects for future earnings growth.