A Letter of Introduction From The Portfolio Managers

Since launching this strategy more than 13 years ago, the demand for information on ESG, impact, and sustainability has risen dramatically. This is partly due to a confluence of global crises that are broadly affecting how people view the world, and partly due to regulatory or political scrutiny, but regardless, the appetite for information, disclosure and transparency has never been higher. We have always tried to be transparent about our approach to sustainable investing, and our annual Impact Reports are a prime opportunity to explain that approach.

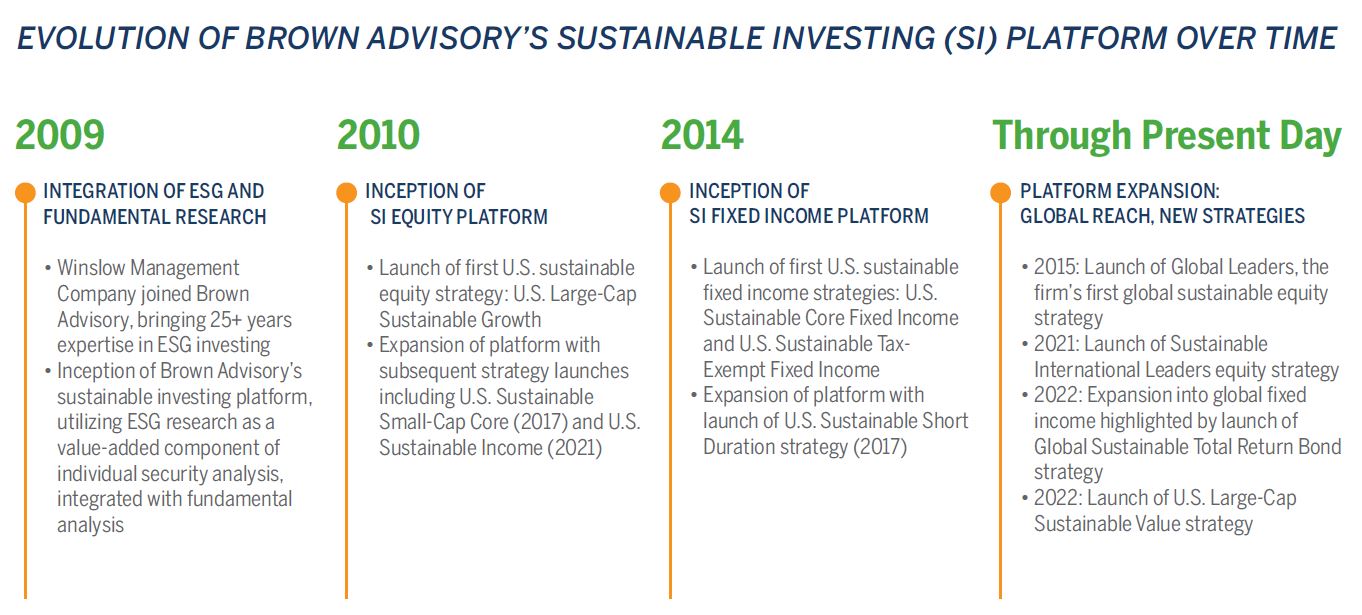

Despite the changing expectations and regulations in this investing arena, we have not altered our sustainable investing (SI) process since our strategy’s inception, and we remain committed to the same investment principles that have guided us since 2009.

Then, as now, we did not seek to meet any external definition or label; we simply believed that using a sustainability lens with investment research provides additional information that helps us judge the merits of a long-term investment.

At the outset, we formalized a research framework for understanding the sustainability risks and opportunities that companies face. To understand ESG-related risks, we look at a wide variety of both quantitative and qualitative information to learn about reputational risks, potential obstacles to attracting and retaining talent, externalized consequences to humans and nature, and the governance practices in place for overseeing these matters. In terms of sustainable opportunities—the “upside” financial potential of a company’s sustainability strategies or attributes—we look for investments that can claim a distinct “sustainable business advantage” or “SBA” that has the potential to spur meaningful revenue growth, margin improvement, market share or other key drivers of enterprise value.

From the start, we understood that our effort to answer this expanded set of questions about a company would lead us to diverse and sometimes imperfect data sources, many of which were not commonly used in traditional investment research. In our view, our results over time have benefited from the fact that we look for information and review data sources that many other investors may ignore. We are active, high conviction investors, and believe that attempting to broadly categorize groups of companies as “good” or “bad” is antithetical to our philosophy. Every company and every situation is unique, and it requires intense and creative research to evaluate each of these situations, parse a wide swath of information, and hopefully make winning decisions more often than not.

Our research into ESG risks and our efforts to identify SBA represent just one aspect of our strategy to generate outperformance; we seek out companies that meet our three equally important criteria of strong fundamentals, sustainable business advantages, and attractive valuation. We believe that many desirable investment opportunities in the large cap growth space lie at the intersection of these three ideas.

We also aim to be transparent about the outcomes of our investment process in the data we display here, such as data describing the carbon intensity of our portfolio or how an investment aligns with the United Nations’ Sustainable Development Goals (SDGs). To be clear, our job as investors is, and always has been, to generate attractive returns, and we believe that ESG research is a means to that end. But after doing this for more than a decade, we have found countless examples where an investment offered plenty of potential for returns as well as positive impact, and there was no need to make a tradeoff. In general, we find that the companies that think comprehensively about risks such as climate change, labor issues, safety and so forth—at all stages of their value chains—are often the companies that are thinking most effectively about their broader businesses as well.

Over the years, we have seen that our focus on performance can create natural alignment with clients who are focused on real-world impact as the end goal. We agree that performance and impact can go hand in hand. Insofar as businesses and hence investment returns depend on natural resources, a stable climate and stable societies, the long-term sustainability of these key elements is a consideration in our capital allocation.

We hope this impact report provides insights into where/how we find relevant extra-financial information, how we discern both qualitative and quantitative ESG data into investment insights, and transparency into how we apply these insights.

Sincerely,

Karina Funk, CFA

Portfolio Manager

David Powell, CFA

Portfolio Manager

*Brown Advisory entities included are: Brown Advisory LLC, Brown Investment Advisory & Trust Company, Brown Advisory Ltd., and Brown Advisory Trust Company of Delaware, LLC.