Fast Reading:

- Disruption in the Strait of Hormuz has created a global energy supply shock, driving higher oil prices and triggering a sharp, inflation-led repricing of interest rate expectations across major economies.

- While markets are pricing a more aggressive central bank response, we see the inflation impact as transitory and expect weakening growth, already evident in many developed economies, to become the dominant force shaping policy.

- Against this backdrop, we remain positioned for a slowdown, using heightened volatility to add exposure to short and intermediate duration, with a medium-term view that central banks will pivot back toward easing.

Introduction

In Greek mythology, the story of Zeus and Pandora strikes us to be an enduringly relevant metaphor for what we’re seeing unfold in the Middle East; developments that are driving several inflection points, particularly within commodities and rates markets. We will spare you the full retelling of Pandora’s story here, but highlight the moment when the box [jar] is opened, releasing evils into the world before being closed again, leaving only hope remaining inside. Our views of the path that led to war in Iran carries a similar resonance, particularly when considering its implications for the global economy.

The path to conflict surprised us, and we are now focused on assessing the range of potential scenarios ahead of us and whether they warrant changes to our asset allocation. At this stage, we have a high level of conviction in our portfolio positioning and have used the elevated levels of market volatility as an opportunity to add to positions on the front and intermediate parts of sovereign interest rate curves.

The effective closing of the Strait of Hormuz, a critical artery for global trade, has triggered a commodity supply shock. We believe this has very different implications from a demand shock, which can typically be influenced more directly by monetary policy. For the current supply shock to be a persistent driver of inflation, and thereby increase the chances of a sustained central bank policy response, one of two conditions would likely need to occur: (1) energy prices would need to rise consistently at the same rate each period to maintain the same impact to consumer price indices, which we view to be highly unlikely; or (2) energy price increases would need to become imbedded in inflation expectations, influencing wage negotiations and corporate price-setting decisions. The latter represents a more credible risk, in our opinion.

Recent events in the Middle East have driven a sharp rise in sovereign interest rates, particularly at the short-end of rate curves in energy-importing economies most sensitive to fossil fuel price increases. This reflects an aggressive, hawkish repricing of global monetary policy expectations following the surge in energy prices. The most extreme examples can be seen in expectations for the Bank of England and the European Central Bank. While higher energy prices are typically associated with increased inflation alongside weaker growth, we believe recent rate moves have been driven almost entirely by inflation concerns. This has been particularly acute in countries/regions where central banks have a singular mandate surrounding price stability. Given the recent experience with elevated inflation, still above target in many economies, this reaction is not entirely surprising.

That said, while we acknowledge the initial inflationary impact, we disagree with the view that aggressive monetary tightening is the appropriate response. Monetary policy works with a lag, and conventional practice is to look through supply shocks while monitoring potential medium-term implications and second-round effects. By the time policy tightening takes effect, the shock is often already dissipating. Moreover, our recent assessment of the global economic cycle suggests a weak starting point across many developed economies, characterised by considerable levels of economic slack, disinflationary pressures, and policy settings that are already near neutral or restrictive.

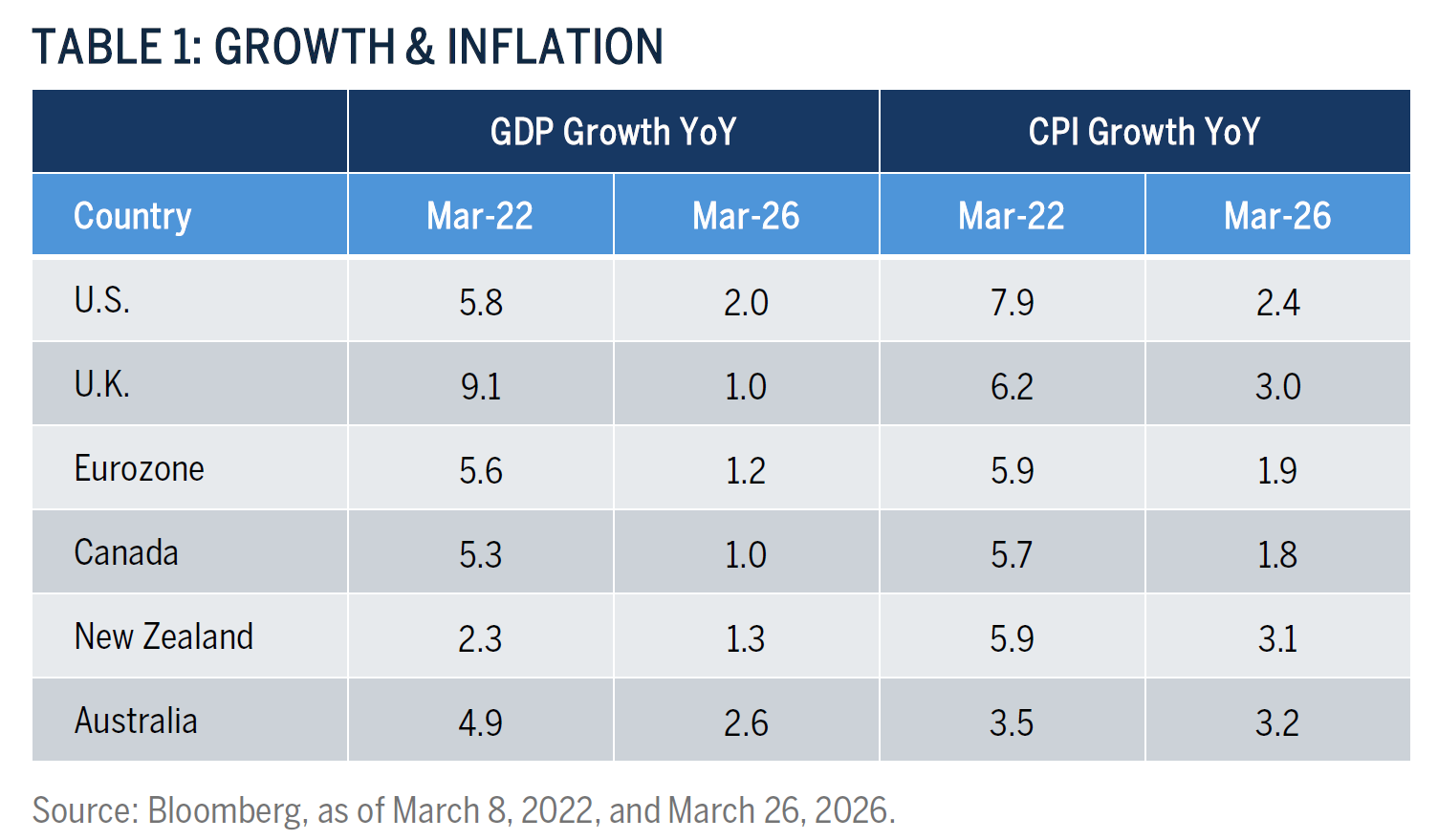

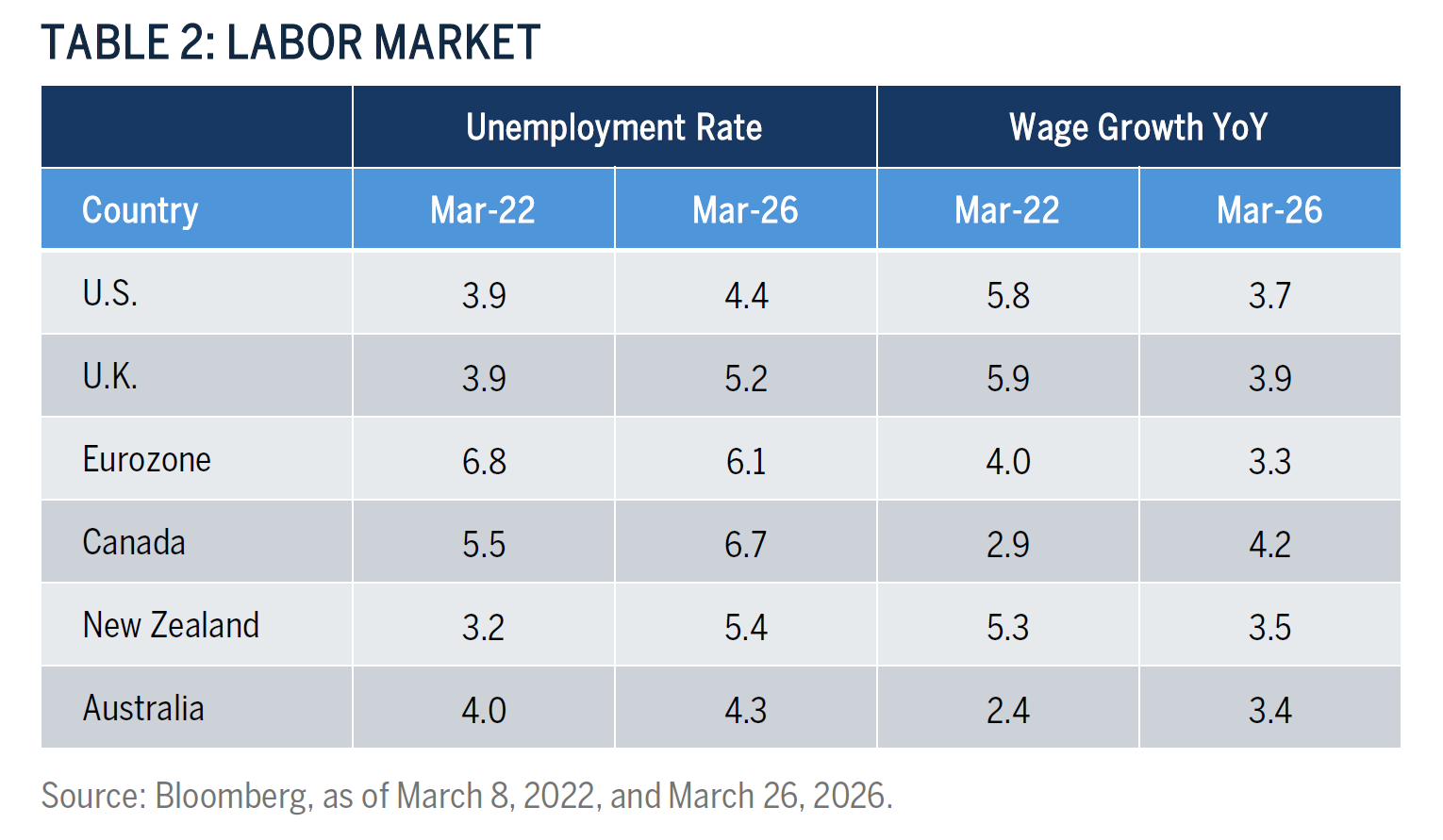

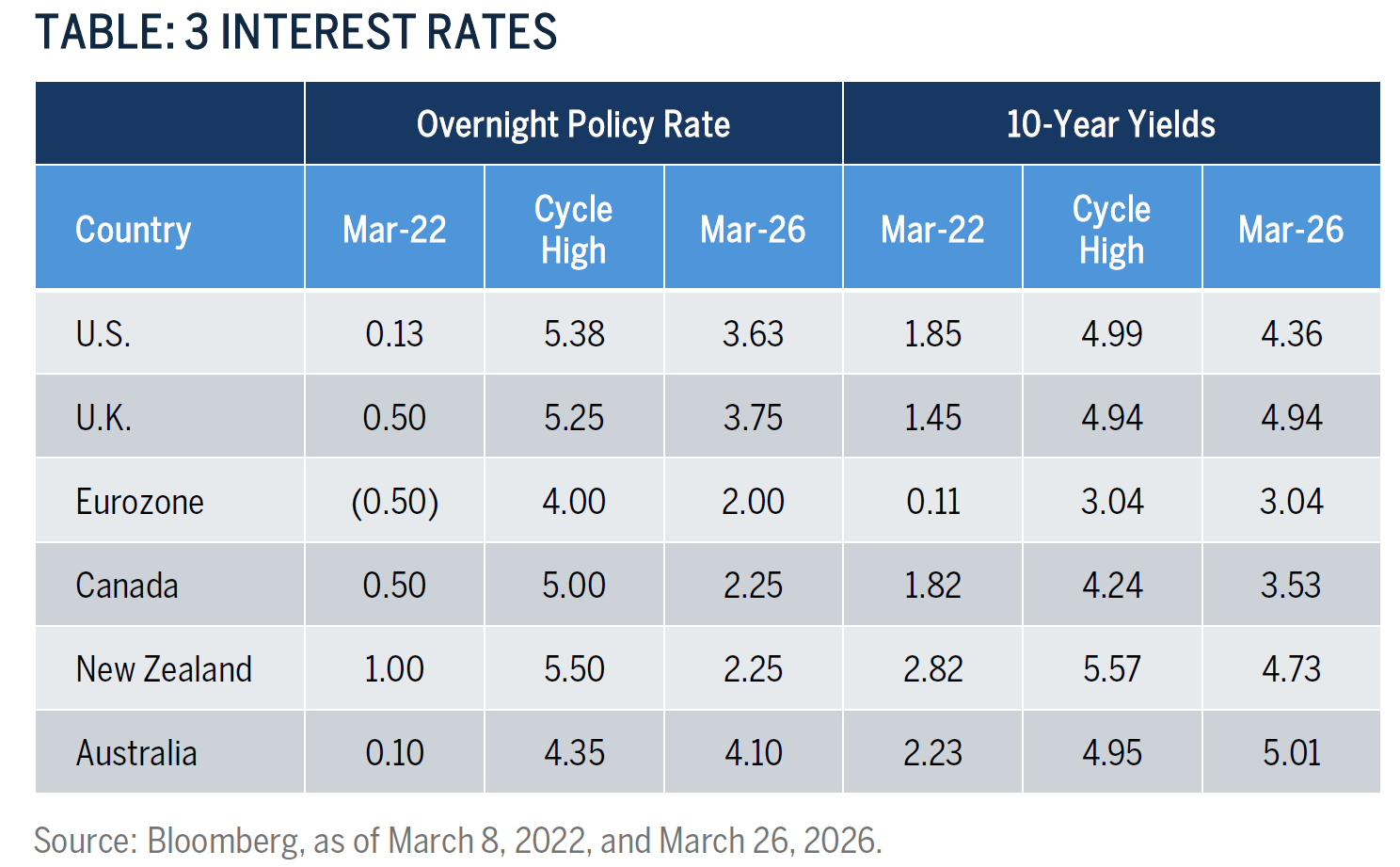

We do not claim to have unique insight into the trajectory or duration of the war in the Middle East. However, we have seen supply shocks before and today’s economic and market conditions differ greatly from past supply shock environments, particularly 2022. As can be seen in the tables here, growth and inflation are lower, interest rates are significantly higher, labour markets are weaker with slower wage growth, fiscal policy is tighter, and post-pandemic supply chains, apart from the impacts of the war in Iran, have largely normalised. In our view, once the initial inflationary impacts are absorbed, demand destruction – especially in economies already operating below potential – will exert downward pressure on inflation and weigh further on growth. With a few exceptions of near-term rate hikes that could be potential mistakes, this dynamic should ultimately lead to renewed central bank easing cycles or a reduction in expected rate hikes.

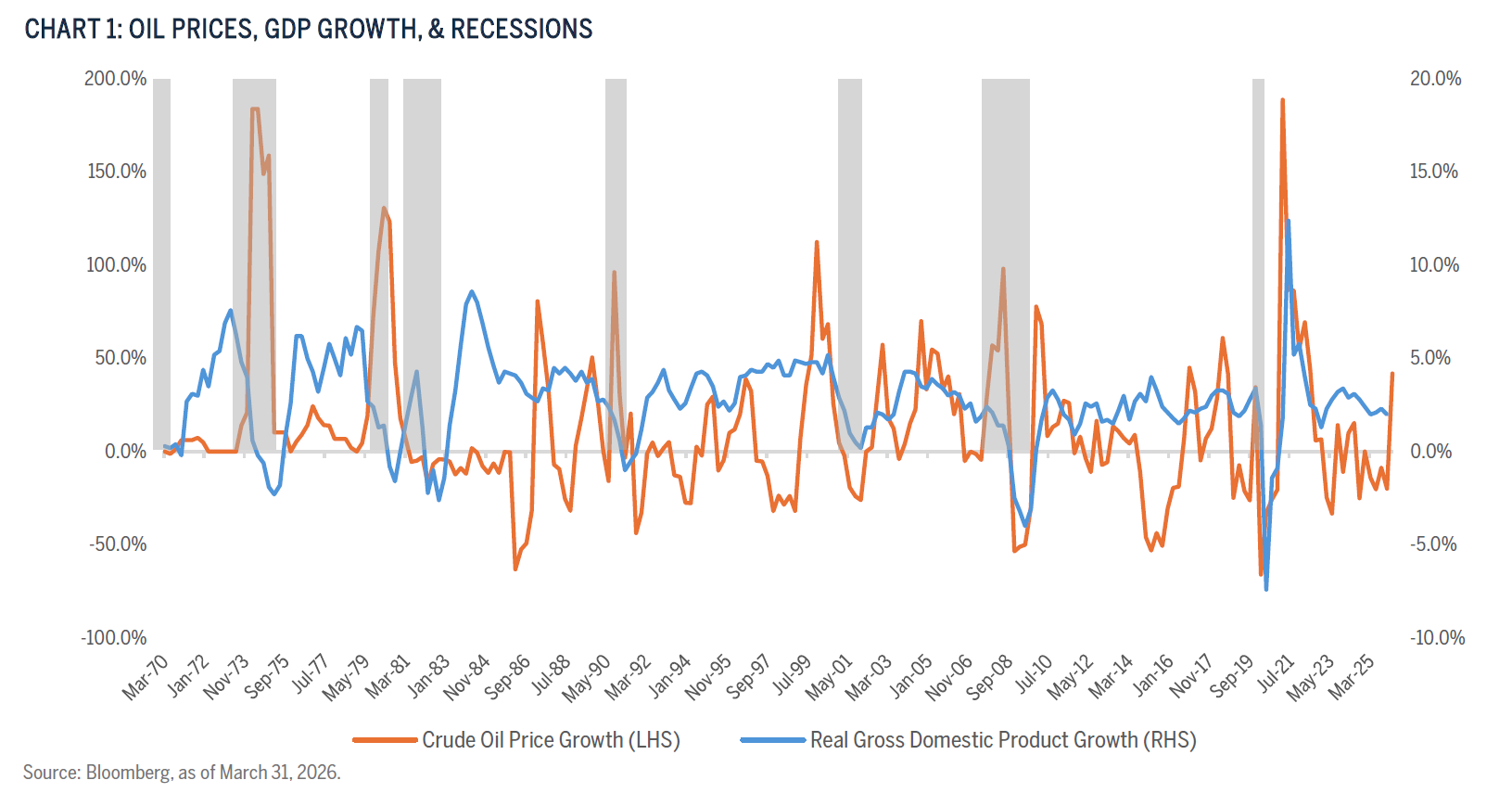

Historical oil price shocks provide useful context, particularly their impact on growth and their frequent association with recessions. In the current environment, we see three broad scenarios for oil prices and interest rates following the war in Iran:

- Near-term resolution: a swift end to the conflict and reopening of the Strait of Hormuz over the coming weeks. In this case, the temporary inflationary pressures and growth headwinds would likely reverse over the coming months with policy expectations migrating toward pre-war levels.

- Prolonged but contained conflict: a drawn-out war with intermittent ceasefires and limited traffic through the Strait of Hormuz over the coming weeks and months. Here, supply-demand imbalances would likely weigh on growth. We think this generally prompts central banks to prioritise economic stability over inflation concerns, leading to lower expected policy rates and expectations over the coming months.

- Escalation: a broader and more destructive conflict that damages infrastructure beyond the limited traffic through the Strait of Hormuz, with lasting global economic effects. In this scenario, the probability of a global recession rises significantly, and central banks would likely respond with aggressive easing, driving interest rates lower – particularly at the front end of curves.

We remain concerned about the fiscal constraints facing many developed-market sovereigns with increasingly risky leverage profiles, reinforcing our preference for short- and intermediate-duration interest rate exposure. While some central banks – particularly those that are near or below neutral rates – may initially tighten policy, we believe hikes beyond current market expectations are unlikely.

The month of March proved challenging for our investment positioning; however, we leaned into the volatility, adding to interest rate risk based on our conviction that near-term dislocations are creating long-term opportunities for yield and capital gains. We have increased exposure in the U.K., New Zealand, and Canada – economies characterised by relatively weak growth, rising unemployment, and declining inflationary trends. As of this writing, market expectations are for a minimum of 2 hikes in each market before year end. However, over a 6-12-month horizon, we expect these central banks to shift focus toward demand destruction and begin easing policy. We anticipate further additions to these positions as geopolitical uncertainties persist and volatility creates additional opportunities.

Are We Doing What We Say We Do? (Where Are We In The Cycle)?

- Consistent with our cycle philosophy, we remain positioned for a slowdown phase.

- Duration is focused on the 2-5-year maturity bucket, primarily in the developed world.

- Spread duration remains limited and we have only been adding credit opportunistically

How We Are Monitoring The Thesis And Why We May Be Wrong:

- Inflation Expectations – aggregating survey, forecaster, and market-based measures of inflation expectations for all countries covered; significant unanchoring from long-term trends could affect the medium-term outlook for inflation.

- Central bank intentions – we believe that our job is to invest based on what we think central banks “will” do, not “should” do. Monitoring speeches, interviews, and other forms of communication will be vital.

- Cost shock broadening – monitoring for evidence that price increases are broadening to other areas/categories; this includes wages, other goods, and services.

We believe active management in fixed income enjoys structural advantages because managers can (1) manage concentration risk that is driven by issuance rather than value creation, (2) use fundamental research to allocate credit risk where compensation is attractive, and (3) manage duration deliberately, independent of issuer behaviour and benchmark mechanics.

Returning to the opening metaphor: if the war in Iran represents the release of Pandora’s box, leaving only hope behind, it serves as a reminder that hope is not an investment strategy, nor should it be ours. Any resolution to the conflict is likely to be complex, given the competing interests and uncertainties involved. While global bond markets – particularly in the U.S. – may act as guardrails for policy responses, we expect the economic burden from elevated energy costs to persist longer than markets currently anticipate.

Ultimately, we believe the growth implications of an energy supply shock will outweigh the inflation effects in shaping central bank behaviour. As such, we remain committed to an investment process grounded in conviction, discipline, and patience – positioning portfolios to take advantage of short-term volatility and to capture long-term opportunities for our clients.

Disclosures

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results.

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results.

Past performance is not a guarantee of future performance, and you may not get back the amount invested.

The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell or hold any of the securities or funds mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent that specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. This material is intended solely for our clients and prospective clients, is for informational purposes only and is not individually tailored for or directed to any particular client or prospective client.

The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy and is not a complete summary or statement of all available data. The information in this document has not been independently reviewed or audited by outside certified public accountants. The information provided is not intended to be a forecast of future events or a guarantee of future results. Past performance is not indicative of future performance.

Terms and Definitions:

Credit risk is the risk that an issuer fails to make scheduled interest or principal payments in full and on time, potentially resulting in loss of value for bondholders. It increases as issuer fundamentals deteriorate (for example, rising leverage or weakening cash flows) and is embedded in broad bond benchmarks that include issuers regardless of changes in credit quality.

Duration is calculated as one over the portfolio turnover rate for the last 12 months, which shows on average the time in years that a manager holds a typical investment in the portfolio.

Total return is the overall return of an investment, combining both price movement and income received (such as coupon or dividend payments) over a given period. It reflects the sum of all sources of return attributable to the security or portfolio, assuming the reinvestment of income.

The yield curve is a line that plots yields, or interest rates, of bonds that have equal credit quality but differing maturity dates. The slope of the yield curve can predict future interest rate changes and economic activity.

Bloomberg is a trademark and service mark of Bloomberg Finance L.P., a Delaware limited partnership, or its subsidiaries. All rights reserved.