I was recently playing tennis with a friend when an instructor named Pierre walked onto the court. He watched for a few minutes as my half century-old limbs attempted to replicate the spin, power and accuracy of my glory days. During a water break Pierre introduced himself and proclaimed, “your shots look like they’ve been preserved in a time capsule from the 1990s.”

While a Wimbledon trophy does not reside on my mantelpiece, I thought I was a respectable player at one time. Mildly offended, I asked Pierre to clarify his comments. “The game has changed. It’s taught differently now.” Pierre went on to show me that with current racket technology top players hit off their back foot to generate pace rather than stepping into the court. He also stated that my one-handed backhand was a bona fide dinosaur. “Why would anyone have a one-hander today? You’re at such a disadvantage!”

After challenging my confidence, Pierre’s parting words were, “I still wouldn’t bet against you when playing my students. They know how to hit the ball, but you know how to compete.”

There is some wisdom in Pierre’s words. My strokes represent a poor attempt at emulating Agassi and Sampras, I have a hip made of titanium and plastic and I look like I’ve been through the war after an hour of competition. Yet, some unwritten rules of the game are evergreen. If you play to your own strengths and aim well inside the lines, you’re going to win a lot.

There are some distinct parallels between tennis and investing. Technology supporting each endeavor has improved dramatically in recent years, as has the information a player/investor has at his/her fingertips. Styles change as well. In February, for the first time in 50 years a one-handed backhand couldn’t be found among the top ten ranked men’s tennis players. Within investing, writ large have been the trends associated with passive versus active.

In order to compete effectively against the benchmarks that reside on the other side of the net, our research team is able to play to its strengths and aim well inside the lines by investing in quality companies, maintaining a multi-year time horizon, and constructing concentrated portfolios that only contain our highest conviction ideas. All the while, it is essential to carry an awareness of the macro, as it establishes the conditions in which we compete. After all, I might adjust my strategy against Pierre’s hard-hitting students depending on wind direction, sun placement, and surface.

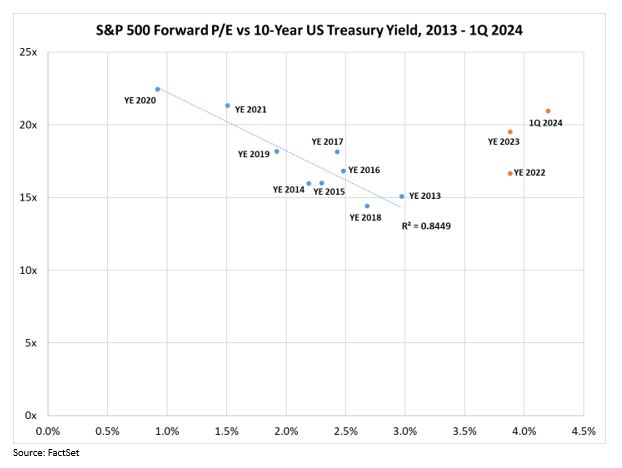

The broader market has remained a formidable opponent, with the S&P 500® Index now trading close to 21x forward earnings as of the end of March, seemingly decoupled from its historically strong relationship with the 10-year US Treasury yield. For many years (at least the past ten), there has been a strong relationship (negative correlation) between the 10-year yield and the market P/E multiple. The 10-year yield has long been utilized as the “risk free rate” in calculating the cost of equity, thus it is rational that the higher the yield, the more sharply future cash flows are discounted to determine fair value – producing lower P/E ratios. As shown below, from YE 2013 to YE 2021 the relationship between equity market valuation and the 10-year yield was extremely strong.

However, something structurally changed by YE 2022 – the market multiple was above 16.5x, a similar level to YE 2016, yet the 10-year yield was about 150 bps higher. By YE 2023, the 10-year yield was the same as it had been 12 months prior, yet the market multiple increased by three times to more than 19.5x. By the end of 1q 2024 the Index fell even further from the historically defined relationship.

Is the US equity market therefore overvalued? Not necessarily. Beyond the discount rate, one should consider both return on equity (ROE) and the expected earnings per share (EPS) growth rate of the S&P 500 Index, factors that are positively correlated with P/E. If ROE and EPS growth are accelerating they can offset the higher discount rate, supporting a higher market valuation.

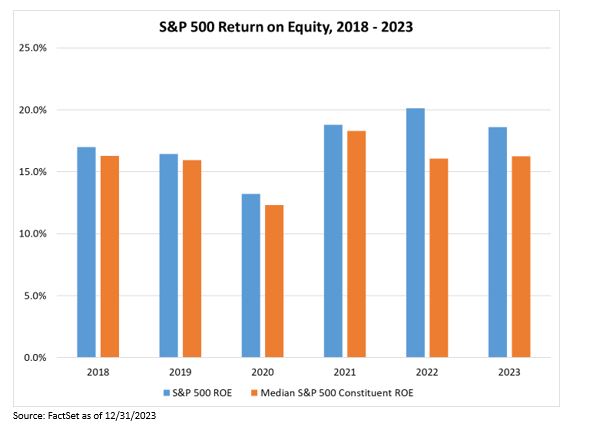

According to FactSet, there has been a step-change improvement in the S&P 500® Index’s ROE in recent years relative to levels pre-pandemic. However, when taking the median ROE of all of the Index’s constituents over these years it is inconclusive whether ROE has actually improved for the underlying set of companies. The explanation for the difference likely lies in the increased weighting of the largest companies in the index – such as Apple (AAPL), Microsoft (MSFT), NVIDIA (NVDA), Alphabet (GOOG) and META Platforms (META) – all of which carry above-median ROEs.

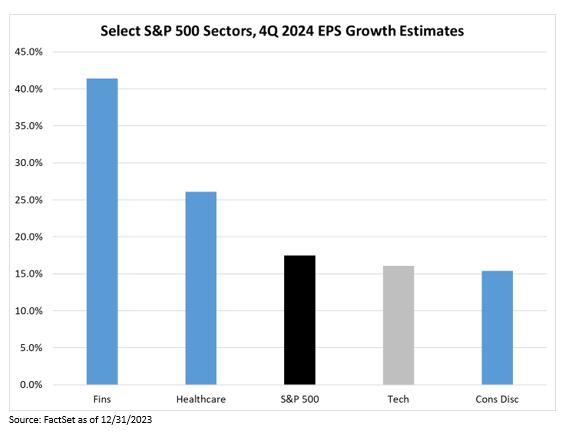

The expected EPS growth rate has also risen for the S&P 500® Index. According to FactSet, from 2012-2023 the Index’s EPS CAGR was a modest 6.9%. For 2024 and 2025, consensus estimates are calling for EPS growth of 10.7% and 13.3% respectively. An acceleration in growth is expected to occur later this year; 1q 2024 EPS growth is anticipated at below 3%, the middle two quarters are expected to show 8-9% growth, while by 4q, the growth rate is expected to explode to 17.5%! By the final quarter of the year, all major economic sectors are expected to show very strong year-over-year EPS growth, suggesting a broad recovery in fundamentals.

The biggest question to be answered as we enter yet another earnings season is whether current expectations for massive EPS growth acceleration for the next several quarters can hold. Our research team will continue to observe these broader trends while focusing on long-term high-quality company fundamentals in an effort to play to our strengths and aim well inside the lines. As for my tennis game, my goals are somewhat less ambitious – if I make it through the upcoming season without injury, it’s a win!

Thanks for reading, and remember to never skip a Beat Eric

All financial statistics and ratios are calculated using information from FactSet as of the report date unless otherwise noted. FactSet® is a registered trademark of FactSet Research Systems, Inc

The PHLX Semiconductor Sector IndexSM (SOXSM) is a modified market capitalization-weighted index composed of companies primarily involved in the design, distribution, manufacture, and sale of semiconductors.

The S&P 500 Index, an unmanaged index, consists of 500 stocks chosen for market size, liquidity, and industry group representation. It is a market-value weighted index (stock price times number of shares outstanding), with each stock's weight in the Index proportionate to its market value.

Standard & Poor’s, S&P®, and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a subsidiary of S&P Global Inc.

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

Terms and Definitions:

Forward P/E Ratio: The Forward P/E Ratio is determined by dividing the price of the stock by the company's forecasted earnings per share.

Return on equity (ROE) is a measure of financial performance calculated by dividing net income by shareholders' equity.

Earnings per share (EPS) is a measure of a company's profitability, calculated by dividing quarterly or annual income (minus dividends) by the number of outstanding stock shares. The higher a company's EPS, the greater the profit and value perceived by investors.

Earnings per share (EPS) is a measure of a company's profitability, calculated by dividing quarterly or annual income (minus dividends) by the number of outstanding stock shares. The higher a company's EPS, the greater the profit and value perceived by investors.

compound annual growth rate (CAGR) measures an investment's annual growth rate over a period of time.