Navigating a Decade of Change: The Enduring Legacy of our Flexible Equity Approach

The UCITS Fund marks its 10th anniversary this year, while the U.S. Flexible Equity Strategy has been in existence for almost 40 years. My involvement with managing the strategy also approaches a decade.

Reflecting on the past 10 years, it is impossible not to acknowledge the profound change we have witnessed both in the U.S. and the global economy that created tremendous uncertainty. Rapidly shifting economic conditions, a volatile geopolitical environment, disruptions like the pandemic and rapid innovations, such as generative AI, have contributed to this volatility. For example, interest rates, which were near zero a decade ago, have reached levels not seen in 20 years. The same holds true for inflation. The prevailing belief was that severe inflation was a relic of the past, primarily a concern for developing countries. For much of this time, Western central banks struggled to stimulate low inflation and growth, hesitating to raise the ultra-low rates or to halt quantitative easing. The tables have turned rather quickly, and now the Fed has its foot on the brakes in a big way as it tries to soak up excess liquidity from the system.

Amidst this whirlwind of change, our steadfast approach that seeks to make investments in good and well-managed businesses – at bargain prices – that will grow in value well into the future has remained unshaken. Our willingness to look at various types of opportunities regardless of “growth” or “value”, which we refer to as a “flexible” approach to investing, has served our clients well. Our investment philosophy and its execution continue to be firmly anchored in the principles that have been laid out since the foundation of our strategy. These principles have not only guided us through tumultuous times but have also illuminated the path forward, reinforcing their timeless value and allowing us to navigate the complexities of the financial world with generally favorable outcomes.

Long-Term Orientation—a Business Owner’s Mindset

Our long-term approach to investing has allowed us to ride out market fluctuations, and the portfolio has benefited from compounding returns. This enduring principle is elegantly encapsulated in Warren Buffett's famous saying, “Our favourite holding period is forever.” Similarly, Charlie Munger, highlighting the virtues of patience and commitment, aptly stated, “The big money is not in the buying and selling but in the waiting.”

Over the last 10 years, our portfolio turnover has averaged 13.8%1, a figure notably lower than industry peers. This perspective of staying invested over time to capture the full potential of a company's growth has served us well in numerous instances.

It will come as no surprise to our long-term clients that, among the top five holdings in the Flexible Equity portfolio a decade ago, three names—Mastercard, Visa and Berkshire Hathaway—still rank among the top five today. These companies have been outstanding performers over the past 10 years. In this period, Mastercard's value has increased by 517%, Visa's by 412% significantly outpacing the S&P 500 Index, which is up by 231.1%2 while Berkshire Hathaway was just behind with 228%. Mastercard and Visa, in particular, are wonderful businesses with exceptional profit margins, high returns on invested capital and high barriers to entry. They have capitalized on their global presence and the secular shift from cash to electronic payments, contributing substantially to our returns over this extended timeframe, though not consistently every year. There have been times when these stocks significantly underperformed, impacting our overall performance. The landscape for these companies has been quite dynamic, with various risk factors emerging periodically. Concerns such as regulatory changes affecting revenue, economic slowdowns (e.g., due to Covid-19) and the potential erosion of their competitive moats by emerging fintech innovations (e.g., cryptocurrency and Buy Now, Pay Later schemes) have arisen frequently during our holding period. Each time, we have revisited our investment thesis. So far, our decision to maintain our holdings has been based on a favorable risk/reward assessment.

Value Philosophy—a Flexible Approach

One aspect of our industry that has long puzzled us is the extraordinary emphasis on "growth" versus "value" and the tendency to prioritize one at the expense of the other. Anyone well versed in securities valuation, as we expect all thorough investors to be, would acknowledge that both "growth" (prospects of growth) and "value" (more precisely, valuation) are essential components of the same equation in fundamental investing. Yet, investors and asset allocators often lean toward one, neglecting the other. Growth investors sometimes dismiss investment opportunities that may not be growing at a rate above a certain arbitrary threshold, regardless of how attractively the stock is priced and its return potential. Similarly, value investors might intentionally overlook companies experiencing rapid growth because their stock prices are trading at a multiple exceeding a self-imposed limit, ignoring the possibility that these companies could become significantly more valuable in the future.

What is surprising is that some institutions, such as Morningstar, oversimplify by categorizing strategies like ours under basic labels such as “growth,” “blend” or “value.” These classifications are supposedly supported by “scientific” mathematics to justify their categorization. Over the last decade, Morningstar has predominantly labelled our Flexible Equity strategy as a “growth style” strategy, a characterization we find too reductive. For instance, our largest holding, Microsoft, was acquired post-GFC more than a decade ago at a low-double-digit earnings multiple—a decision anyone today would recognize as a quintessential value investment. Back then, growth investors were not interested in Microsoft, but now they are, as it has significantly increased its earnings growth rate compared to a decade ago. So, should we sell our position just to fit back into their “blend” category, to the detriment of our clients? Another example is Netflix, which was favored by growth investors until 2022 when growth stocks fell out of favor, and its stock plummeted from over $700 to less than $2003. We did not waste time debating whether it was a growth or a value stock; instead, we recognized a significant value in the stock and became shareholders. Since then, the stock has experienced significant appreciation. This raises the question: Does this investment approach classify us as growth investors or value investors?

Despite industry pressure, we have consciously chosen to reject this simplistic classification. Our strategy is not to restrict our investment universe but to maintain an open mind toward all investment opportunities. We are willing to invest in high-growth companies as long as we are confident in their long-term prospects, and the stock is trading below our estimation of its intrinsic value. Similarly, we are open to investing in stocks considered value according to indexes, provided we see potential for the company to grow in value over time.

Margin of Safety

Another quote by Buffett, "Forecasts may tell you a great deal about the forecaster; they reveal nothing about the future," highlights the inherent uncertainty and complexity of predicting market movements. Recognizing the challenge of foreseeing the future, we stress the importance of humility, caution and a focus on long-term over short-term predictions within our equity research team.

It would be misguided to assume that the future of the companies we invest in will unfold precisely as we predict in our financial models. Acknowledging the real possibility of error, we adopt Benjamin Graham's principle of the “margin of safety,”4 a cornerstone of value investing. Therefore, we refrain from overly optimistic assumptions about the future and carefully consider the business attributes that could potentially hinder a company's growth in value.

This disciplined approach proved invaluable when COVID-19 emerged unexpectedly. Thanks to our cautious strategy and the inherent resilience of the businesses in our portfolio, we were not compelled to make extensive adjustments during the peak of the crisis due to fear of the risk of a business failing.

A Balanced Portfolio, Well Positioned for the Future

In our view, this investment strategy has cultivated a well-balanced portfolio that has been rigorously tested across a variety of market conditions. Over just the last four years, we've navigated through several market cycles, including a market crash in 2020, followed by a surge in growth stocks; an irrational exuberance for growth at any cost (e.g., SPACs, cryptocurrency, fintechs) in 2021; a significant shift with a sell-off in growth market leadership with the emergence of generative AI, exemplified by the rise of the “Magnificent Seven.”5

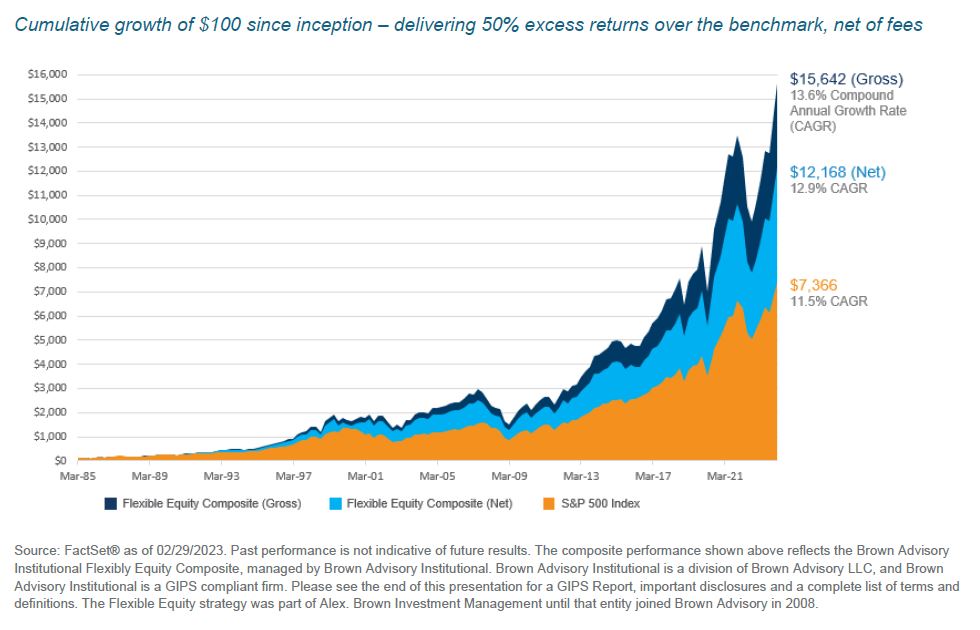

We are pleased to report that the portfolio has successfully navigated these dramatic fluctuations, generally outperforming without necessitating major adjustments. Along the way, we have seized opportunities to invest in exceptional companies (e.g., Adobe and Intuit) at favorable prices during these market movements. We are huge advocates of patience and buy-and-hold investment strategy that benefits from the ‘magical’ power of compounding. As the graph below illustrates, maintaining the US Flexible Equity Strategy over extended periods has led to significant outperformance relative to the S&P 500.

Inflation – How Much Progress?

Although inflation remains a top focus for central bankers, today’s elevated environment warrants additional scrutiny. The two most commonly followed measures of inflation in the U.S. are the Consumer Price Index (CPI) and the Personal Consumption Expenditure Index (PCE). Both the Federal Reserve and market participants alike tend to focus on the core measures of both data sets that exclude the more volatile food and energy components. For choice, the Federal Reserve considers the PCE to be the superior measure since it is a broader measure, accounts for substitution effects and more accurately reflects consumer spending patterns, among other reasons. Due to these differences, core PCE has had an average reading that has been 0.33% lower than core CPI over the last 25 years . Yet today, that difference sits at the extreme end of its observed range over the past quarter century (shown in Figure 2). At the time of writing, core PCE is 1.1% lower than core CPI and moving much closer to the Federal Reserve’s inflation target. It may be a challenge for Fed officials to communicate this phenomenon to the general public, as CPI is the much more closely followed and understood gauge. That said, even with potential communication difficulties ahead, we expect the committee to continue to place more weight on PCE rather than CPI when formulating monetary policy.

Upon review of our holdings, it becomes clear that this isn't your grandfather's portfolio; the companies within are at the forefront of change and innovation and are well positioned to thrive in the future.

We thank you for your support and interest in the strategy.

Maneesh

Sources:

1 Source: FactSet.

2 Source: FactSet & Brown Advisory Analysis, cumulative performance from 03/07/2014 to 03/07/2024

3 Source: FactSet & Brown Advisory Analysis, 2024

4 Source: Columbia Business School. "Value Investing History."

5 Source: The “Magnificent Seven” is a collection of Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia & Tesla attributed to Michael Hartnett of Bank of America

Disclosures

Past performance may not be a reliable guide to future performance and investors may not get back the amount invested. All investments involve risk. The value of the investment and the income from it will vary. There is no guarantee that the initial investment will be returned.

Performance data herein relates to the Brown Advisory U.S. Flexible Equity Fund (the “Fund”). The performance is net of management fees and operating expenses. This communication is intended only for investment professionals and those with professional experience of investing in collective investment schemes. Those without such professional experience should not rely on it. Any entity responsible for forwarding this material to other parties takes responsibility for ensuring compliance with applicable financial promotion rules. Changes in exchange rates may have an adverse effect on the value price or income of the product. The difference at any one time between the sale and repurchase price of units in the Fund means that the investment should be viewed as medium to long term. This factsheet is issued by Brown Advisory Ltd, authorised and regulated by the Financial Conduct Authority in the U.K. This is a marketing communication. This is not an offer or an invitation to subscribe in the Fund and is by way of information only. Cancellation rights do not apply and U.K. regulatory complaints and compensation arrangements may not apply. This is not intended as investment or financial advice. Investment decisions should not be made on the basis of this factsheet. A Prospectus is available for Brown Advisory Funds plc (the “Company”) as well as a Supplement for the Fund and a Key Investor Information Document (“KIID”) for each share class of the Fund. The Fund’s Prospectus can be obtained by calling +44 (0)20 3301 8130 or visiting https://www.brownadvisory.com/intl/ucits-legal-document-library and is available in English.

The Fund is an Article 8 financial product for the purposes of Regulation (EU) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on sustainability related disclosures in the financial services sector (SFDR). Sustainable investment considerations are one of multiple informational inputs into the investment process, alongside data on traditional financial factors, and so are not the sole driver of decision-making. Sustainable investment analysis may not be performed for every holding in the Fund. Sustainable investment considerations that are material will vary by investment style, sector/industry, market trends and client objectives. The Fund seeks to identify companies that it believes may be desirable based on our analysis of sustainable investment related risks and opportunities, but investors may differ in their views. As a result, the Fund may invest in companies that do not reflect the beliefs and values of any particular investor. The Fund may also invest in companies that would otherwise be excluded from other funds that focus on sustainable investment risks. Security selection will be impacted by the combined focus on sustainable investment research assessments and fundamental research assessments including the return forecasts. The Fund incorporates data from third parties in its research process but does not make investment decisions based on third-party data alone.

Brown Advisory relies on third parties to provide data and screening tools. There is no assurance that this information will be accurate or complete or that it will properly exclude all applicable securities. Investments selected using these tools may perform differently than as forecasted due to the factors incorporated into the screening process, changes from historical trends, and issues in the construction and implementation of the screens (including, but not limited to, software issues and other technological issues). There is no guarantee that Brown Advisory’s use of these tools will result in effective investment decisions. The decision to invest in the Fund should take into account all the characteristics and objectives of the Fund as described in the Prospectus. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client. For further information, please visit https://www. brownadvisory.com/intl.

The Fund uses the S&P 500 Net Index as a comparator benchmark to compare performance. The Fund is actively managed and is not constrained by any benchmark. The S&P 500 Index represents the large-cap segment of the U.S. equity markets and consists of approximately 500 leading companies in leading industries of the U.S. economy. Criteria evaluated include market capitalization, financial viability, liquidity, public float, sector representation and corporate structure. An index constituent must also be considered a U.S. company. An investor cannot invest directly into an index.

Brown Advisory is the marketing name for Brown Advisory, LLC, Brown Investment Advisory & Trust Company, Brown Advisory Securities, LLC, Brown Advisory Ltd., Brown Advisory Trust Company of Delaware LLC, Brown Advisory Investment Solutions Group LLC, Meritage Capital LLC, NextGen Venture Partners, LLC and Signature Financial Management, Inc.