As of the end of 2015, $1 out of every $5 under professional management was invested in accordance with some sort of social, environmental and governance (ESG) consideration, according to the Forum for Sustainable and Responsible Investment (US SIF). Every year, we see more and more of our clients looking for ways they can use ESG investment principles to potentially boost returns, align their investments and values and make an impact on the world.

Tom Graff, the portfolio manager of the Brown Advisory Sustainable Core Fixed Income Strategy, has seen a tremendous evolution in the tools available to ESG-oriented investors since he began helping clients with ESG mandates in the 1990s. During the early part of his career, ESG investing was generally limited to basic portfolio screening, but today, he and his team use a far more comprehensive approach. “We think about sustainable investing very broadly in this strategy,” notes Amy Hauter, the strategy’s ESG research analyst. “It’s not just about steering clear of polluters. We are looking for companies whose credit profiles are enhanced by the way they manage environmental risk; we also look for bonds whose proceeds are being used to generate positive, measurable impact on society. We leverage ESG information in many different ways.”

Brown Advisory has managed its Sustainable Core Fixed Income strategy for several years. Tom and Amy recently shared some insights about their approach to sustainable investing in an internal question-and-answer session about the strategy; this transcript has been lightly edited.

Q: Why is this the right time for sustainable bonds?

Tom Graff (Portfolio Manager): Historically, ESG investors generally seemed more focused on their equities than on their fixed income holdings. But to address big challenges like climate change, governments and companies will need to fund massive infrastructure projects—retrofitting buildings, factories and power plants; building new renewable power generation capacity; and the like. Those kinds of projects are typically funded in the debt market—some by governments, some by companies.

The reason it’s an exciting moment for the market is that the supply and demand are both accelerating. The development of the green bond market has been the key—issuers can clearly signal the environmental benefits of a bond offering, and the growing body of investors who care about sustainability are flocking to these bonds that offer analogous performance to other bonds. We believe that there are more positive impact bonds available to us now, so we can help our clients accomplish a broader set of ESG-related goals.

Other than the advent of green bonds, what other big changes have you seen in the last decade?

Amy Hauter (ESG Research Analyst): As sustainable investing becomes more mainstream, corporate issuers and municipal issuers are becoming a lot more transparent about their initiatives and efforts. They’re getting a lot more pressure from their investors. Some of the biggest rating agencies, such as Moody’s and S&P, are coming out with their own ESG metrics. It’s gradual, but ESG criteria are becoming more accepted as components of financial research.

Tom: When I think about the early years of my career, it definitely felt like environmentalists and corporate America were definitively lined up against each other. That feeling is fading—certainly there are still tensions between the two, but there is also better alignment. When President Trump announced the decision to pull out of the Paris climate accord, you had a broad range of companies protesting what they viewed as a poor decision— including the unlikely voices of companies whose core businesses exclude them from most sustainable investing portfolios. Now, there may be a gap between what those companies said and what they really want, but the point is that we never would have heard a public corporate response against climate change like that back in the 1990s. It’s not because of altruism. Companies know that their customers care, they are realizing that these issues do in fact affect their businesses, and more and more of them—not all, but some—believe that we are better off facing these issues now rather than later.

How do you define “sustainable”?

Amy: We’re by no means trying to dictate what sustainable investing means for our clients. That’s why we don’t apply any hard-and-fast screens in our process (we do offer customized screens for our separate account clients that request them). Take energy, for example. We don’t currently hold energy names in the portfolio, but it’s not because of a screen—we simply don’t see great opportunities in that space that fit our investment criteria right now. We would certainly consider a green bond issued by an energy company, if the company had good ESG characteristics and the bond was funding, say, a renewables project.

We use a holistic approach—we think about a broad set of ESG factors and how they may impact the credit profile of a potential investment—and we try to cover a broad set of themes—renewables, water, clean transportation and many others—when it comes to the green bonds in our portfolio.

What is the demand for sustainable fixed income?

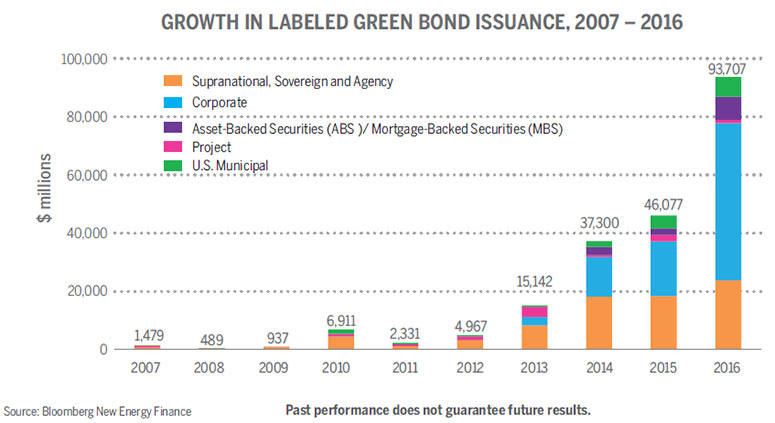

Amy: The green bond market launched in 2007, and in 2013 we started to see an explosion of growth—record issuance year after year. In the first six months of 2017, we again saw record issuance of $68 billion, which surpassed the total for the first half of 2016. And many of these issues are heavily oversubscribed. So, demand for bonds with sustainable attributes is definitely strong. At the same time, investors are becoming more discerning in this space. They are eager for transparency with regard to impact, and they want to see impact reports using new and innovative frameworks from issuers and bond managers.

Tom: We should reinforce that point. What’s so unique about green bonds is that they provide reporting on the environmental impact of a project. What are the proceeds being used for specifically? By how much are environmentally focused projects reducing carbon output or saving water? And issuers are following similar guidelines to report impact on socially oriented projects that they fund—details on how investor capital is helping to improve health outcomes, make affordable housing more available, bring jobs to inner cities and so forth. Because of these reports, we can aggregate the impact of the bonds in our portfolio and tell our clients that for every dollar they put into this strategy, here’s what happened with that dollar, and here’s what happened to the world because you invested that dollar. For investors who care about impact, that is an extremely powerful and valuable benefit that would not have been possible to deliver just a few years ago.

How do you find your investment ideas?

Tom: We scan a broad universe for our ideas. A number of large government issuers offer a steady flow of green bonds, and we can use those as our high-quality, high-liquidity base. We don’t limit ourselves to certified green bonds; other bonds in which we invest are also funding positive-impact projects, but they haven’t gone through the process to get the green bond label.

We find attractive corporate bonds across the quality spectrum. Many are investment-grade (bonds with credit ratings of BBB- or higher), and there are also high-yield ideas in the portfolio. And then we own a number of municipal bonds—both taxable and tax-exempt—as well as mortgage-backed securities. Once we put all of that together, our portfolio—by design—looks very much like a typical core bond strategy. A primary goal for us is to show that we can use ESG principles broadly in fixed income, and we believe doing so can actually help us compete effectively with any other strategy in our peer group.

What are some examples of holdings in the strategy?

Amy: On the corporate side, we own a green bond issued by MidAmerican Energy, a large utility and a subsidiary of Berkshire Hathaway. MidAmerican owns more wind-powered generation capacity than any other U.S. regulated utility. The proceeds from this bond are funding two wind projects in Iowa. This is a good example of how we focus on both the impact of a bond’s proceeds and the attributes of the issuer when we evaluate bonds. The fact that MidAmerican has such a big renewables portfolio is meaningful—as a positive ESG attribute, and also as evidence of management’s long-term focus on diversification and risk mitigation.

An example that offers social impact is Becton Dickinson, an industry leader in addressing access to health care for underserved populations. It has partnered with a variety of organizations to develop affordable pricing models in developing countries, where its prices are discounted as much as 75% versus its prices in developed markets.

Tom: Outside of corporate bonds, we hold a variety of municipals that are certified green bonds and fund environmentally beneficial projects. And we hold mortgage-backed securities that generate positive social outcomes; for example when we invest in agency MBS pools, we are looking for a focus on low- and moderate-income borrowers, rural neighborhoods, homes located in federally declared disaster areas and other factors that support affordable and accessible housing. As we mentioned earlier, we invest in a diverse, core fixed income portfolio, but the bonds we hold in many asset classes are generating impact as well.

And do you also marry those concepts in the strategy?

Tom: We seek to deliver a yield that is similar to other core mandates.We believe that investors are not giving anything up in yield by investing with their values in mind. In our experience, investors may care tremendously about social or environmental investing, but it’s very rare that they are willing to sacrifice returns. This is particularly tricky for some of our clients, who serve on endowment or foundation boards that have a fiduciary duty to balance mission alignment with performance expectations. We really think that the future of sustainable investing has to balance performance, values and impact in a way that doesn’t trade off one for the other. ![]()

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views should not be construed as investment research. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.