Late September announcements by the Federal Reserve and the Bank of Japan (BOJ) underscore that today’s extraordinarily low interest rates are likely to persist for some time to come. The Fed’s decision to leave rates unchanged means that its quarter-point hike in December 2015 stands as the only increase in more than 10 years despite significant economic progress over the period. The BOJ indicated that it will continue its aggressive program of buying bonds and keep the yield on its sovereign 10-year bond at approximately zero.

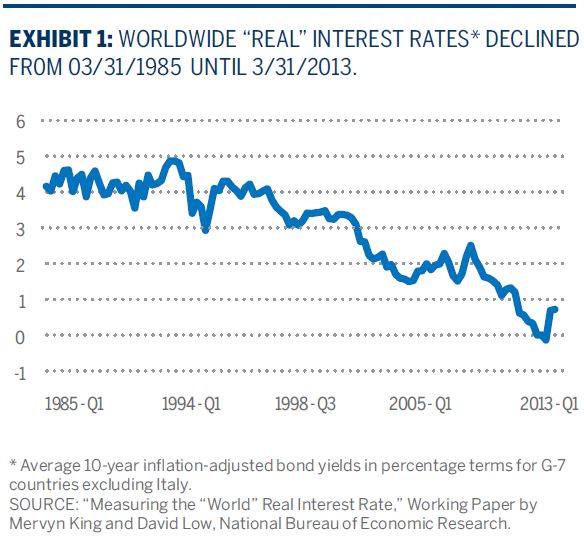

When market pundits invoke the term “uncharted territory” to describe why the outlook may be clouded, they often exaggerate for effect. In the case of interest rates, however, the word uncharted can be taken literally. According to a 2015 study by Bank of America Merrill Lynch, interest rates today are lower than they’ve been at any time since the First Dynasty of Egypt—virtually the dawn of civilization. And we doubt that rates were “charted” in 3100 BC.

Central bank policies that push the world’s largest economies into unexplored terrain prompt some fundamental questions. What are the goals of extreme monetary easing? What are the limitations and risks of the policies? Also, during an extended period of record low interest rates, what opportunities are available to investors who depend on a steady cash flow from their portfolios?

Negative Rates

Currently, interest rates in many parts of the world are negative, meaning that a person or entity with excess cash must pay an institution to hold it. In Denmark, for example, the rate on certificates of deposit is minus 0.65%, and in Switzerland, the rate on deposits is minus 0.75%. Meanwhile, the European Central Bank has set a base interest rate of zero. In the capital markets, two European companies, Sanofi and Henkel, have issued euro-denominated bonds with negative yields.

In the U.S., rates remain positive but at historically low levels, as Fed policymakers voted in late September to maintain the target for federal funds at 0.25% to 0.50%. Despite continued improvements in the economy and the labor markets, rates are only a quarter of a point above where they were in the depths of the financial crisis of 2008-09, when banks and various other companies had to be bailed out by the government. The 10-year Treasury bond currently yields about 1.7% (seemingly a bargain among developed markets). This too is about a quarter point above its low point.

Viewed in inflation-adjusted terms, it’s not unusual for interest rates to be negative. Real interest rates turn negative whenever inflation exceeds the rate of interest—an occurrence from time to time in emerging and developed markets alike. It usually doesn’t last long because central banks typically try to reduce inflation by tightening (raising) interest rates aggressively. What’s unusual about today’s interest rate environment is that nominal rates are negative in much of Europe and Japan, and they have been so for several years in some cases. This is truly uncharted territory.

Aggressive Easing

Whether in nominal or real terms, today’s interest rates are extraordinarily low, as central banks around the world aggressively ease in order to serve several purposes:

- Stimulate economic growth: Lower borrowing costs should in theory prompt corporations to spend more on capital equipment and consumers to purchase goods and services on credit, thereby expanding economic activity.

- Encourage risk-taking: Since low interest rates result in minimal returns on “safe” investments like government bonds, investors will tend to seek higher returns by allocating capital to riskier, longer-dated assets. Again, the result should be an incremental increase in economic activity.

- Accelerate inflation: If borrowing picks up and new investments are tilted toward higher-risk assets, the resulting growth should spur inflation. Traditional economic theory, embraced by most central bankers, holds that stable inflation of around 2% is conducive to demand growth, but in the developed world, it has languished near zero since growth has been so slow in recent years.

- Manage currency values: As international capital gravitates to countries with high interest rates (particularly in real terms), such countries normally see the value of their currencies rise. The U.S. dollar, for example, has been relatively strong over the past five years. Similarly, countries with low interest rates often find their currencies depressed, making the effective price of their goods on international markets a relative bargain. Keeping interest rates at historic lows is thus one of the tools used to manage currency values and promote positive trade balances. At a time when domestic demand may be sluggish, exports can be a key factor in maintaining overall economic health.

To date, extreme central bank measures have seemingly encouraged risk-taking in certain sectors, and economic growth has probably been higher than it otherwise would have been. But inflation in most parts of the world is almost non-existent, and the spread remains narrow between U.S. Treasuries and other debt with the same maturity. On balance, central bank policies aren’t working effectively.

As potent as low or negative interest rates may be in theory, they lack precision in practice and may even have unintended consequences. For starters, interest rates affect different kinds of institutions in somewhat different ways. Banks tend to keep the interest on retail deposits positive, partly because smaller depositors may hoard cash rather than pay a bank to hold it when rates are negative. Thus, banks with large retail customer bases pay more for their funds and have difficulty matching the lending rates of institutions with wholesale customer profiles. Further, not all demographic groups react in the same manner. For example, consumers are less inclined to take on new debt as they get older since they are no longer drawing a paycheck, raising children or buying larger homes. Finally, low rates mean less spendable income for those who rely on savings in retirement. Thus, the impact of low rates is uneven.

Uphill Battle

More broadly, recent central bank strategies are unlikely to be effective over the long term. While low rates are intended to stimulate consumer borrowing, it’s questionable whether demographics will support further increases in already-high levels of debt. Over recent decades, the ratio of total public and private debt to gross domestic product (GDP) has risen steadily in many developed countries, and it has been sustained in recent years by the moderating effect of low rates on the cost of servicing debt. Aging populations, however, pose a threat to this pattern. To assess these trends, the German bank Berenberg recently released a report tracing the “dependency ratio” (the ratio of non-workers—mostly children and the elderly—to workers) since about 1950. Historical data suggests that private sector debt rises about three times as fast relative to GDP when the dependency ratio falls as when the ratio rises. The combination of low birth rates and longer life expectancies, resulting in a long-term rise in the dependency ratio, suggests that central banks’ attempts to stimulate borrowing may be an uphill battle.

Another factor limiting the effectiveness of highly stimulative monetary policy is that it doesn’t affect the underlying capacity for growth. In the long term, the growth of a nation’s economy is a function of population expansion (specifically, the workforce) and productivity. Central bank actions serve to accelerate or decelerate activity in the short run but cannot change the basic equation of growth. That is, an interest rate reduction may encourage some people to borrow and to invest or spend the money, thereby accelerating growth beyond what it would have been for a period of time. Conversely, tighter monetary policy will cause a temporary contraction in activity. But unless the level of debt relative to GDP keeps growing indefinitely—clearly an unsustainable trend—the economy will track its underlying capacity for growth (labor times productivity).

Finally, as many observers have made clear, today’s low rates leave no room for easing if a future recession or slowdown should call for monetary stimulus. To be sure, central banks can—and do—directly purchase debt securities to put more money into circulation (a practice called Quantitative Easing). But it’s uncertain how long such a strategy can be carried out. In the previous three recessions, the Federal Reserve cut interest rates by 6.75, 5.50 and 5.12 percentage points, respectively. From the current 0.50% in the U.S., there is not much room to cut.

Risks

In addition to their limitations, negative rates pose risks to the financial system that should not be taken lightly:

- Profit pressure: At a time of tremendous political and regulatory pressure to improve the health of the financial system in Europe and the U.S., negative rates are having the opposite effect. In reality, they behave as a kind of tax on banks. When central banks charge their member banks for leaving funds on deposit, it increases the banks’ cost of funding and squeezes net interest margins because of low lending rates. Also, as bonds and loan portfolios mature, banks and other financial institutions are not able to replace the income they generated because today’s rates are so low. In the insurance industry, most obligations are fixed by contract, yet the money earned by insurance companies on their bond portfolios has shrunk, hurting profits. It hasn’t helped that tighter regulatory standards have forced financial institutions to own a larger proportion of bonds in their investment portfolios.

- Hoarding cash: If consumers have to pay rather than be compensated for parking their cash in a bank, there is some risk that they will choose to hoard it. While a few small would-be depositors won’t make a meaningful difference to banks generally, it would matter if such a practice became more widespread. In iMFdirect, an International Monetary Fund blog, the writers estimate that the tipping point for decisions to move into cash is somewhere around minus 0.75% to minus 2.00%. At such a cost, they posit, large numbers of consumers would begin to treat cash as a store of value and even a primary means of processing transactions.

- Asset bubbles: As returns on the safest assets (deposits, short-term government securities, etc.) drift lower or become negative, investors have tended to seek better returns elsewhere. This inevitably means taking on more risk. Some would argue that there are already signs of excess speculation in various asset classes, particularly those with meaningful current yield. Real estate investment trusts, utilities and other moderate-to-high dividend payers, for example, have been among the best performers in the stock market during the past four years and are trading at unusually high valuations.

For lots of reasons, it appears that market yields will remain depressed for some time to come, even if central banks gradually raise rates. As we’ve already noted, debt levels remain high by historical standards. Demographic trends suggest that consumers are unlikely to take on large amounts of incremental debt, and corporations see little reason to add to leverage given slack demand growth. On a policy level, central banks must be mindful of the risks of raising rates in light of the still-fragile nature of the global recovery and the potential for budget deficits to balloon if debt service costs rise.

The prospect of continued low rates poses a dilemma for investors who depend on the cash flow from their portfolios or who rely on fixed income securities to provide stability in their asset mix. With regard to bonds, these two objectives are in conflict: longer-dated bonds provide higher yields (the yield curve generally slopes up), but they are more volatile because their prices are particularly sensitive to fluctuations in interest rates. In addition, higher-yielding bonds of similar maturity are subject to greater risk of default. In managing bond portfolios, we seek an appropriate balance of risk and return for each client in light of individual circumstances. Our credit research is designed to identify specific bonds that add to overall portfolio yield but whose risk of default is minimal. Currently, though, the income on quality bond portfolios is modest by historical standards.

As we’ve said, income-producing stocks have been strong performers during the past couple of years. Rather than pay up for equities with above-average yields but little to no growth prospects, we prefer to own stocks with growing dividend streams. But that means accepting lower yields of 2% to 4% on the front end. Similarly, money has flowed heavily into preferred stocks in search of yield, but the opportunity for growth is severely limited because preferreds do not normally participate in a company’s incremental profits. Master limited partnerships (MLPs) can offer attractive yields but are directly exposed to the risks of the underlying business, as their payouts rely on the enterprise’s cash flow. The collapse in energy MLPs has been a painful reminder of this risk. Most of these income vehicles have evidenced sensitivity to rising rates, falling whenever talk of Fed tightening heats up.

Diversifying Income Streams

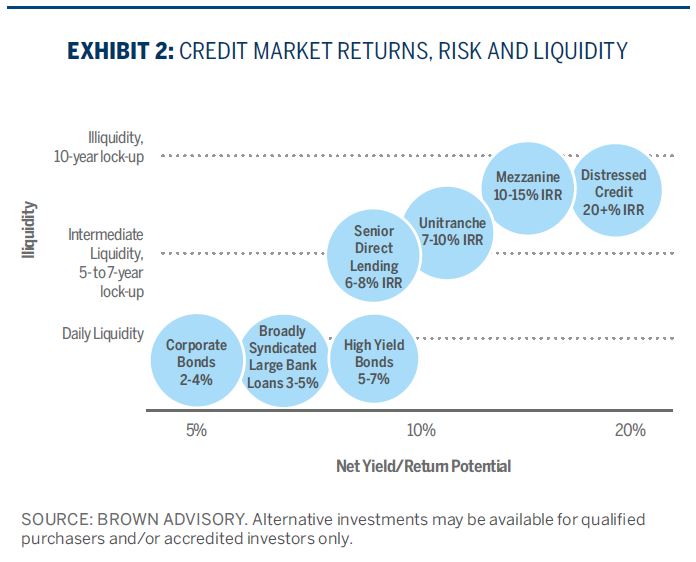

One approach to increasing portfolio income is to diversify into a variety of higher-yielding assets, thereby reducing the reliance on any single one. While quality bonds have historically been the primary source of income for most portfolios, today’s markets offer multiple ways to find yield. High-yield bonds are readily available in the form of mutual funds with daily liquidity or separately managed accounts, and we have introduced them into client portfolios where appropriate. We have also used income-producing real estate partnerships* as a means for qualified investors to add to income. Some partnerships pay out a portion of cash flow (producing a partially tax-sheltered yield of 3% to 5%) currently while reinvesting the remainder for growth. For investors able to accept low liquidity, these partnerships can make sense.

Also in the realm of illiquid investments are partnerships focused on various forms of private credit*. After the financial crisis, it became challenging for less creditworthy companies to find sources of financing. At the same time, regulatory changes caused banks to tighten lending practices in order to conserve capital. Sensing an opportunity to fill this gap, some private debt* funds have been formed. Drawing on capital provided by institutional and high-net-worth investors, these funds have carved out specific niches lending directly to corporate borrowers, particularly small- to mid-sized ones with limited access to capital. Depending on the creditworthiness of the borrower and the type of security, these partnerships range from senior direct lending with yields of 6% to 8% to distressed credit with much higher potential internal rates of return. These vehicles are not for everyone, but as part of a larger, diversified portfolio, they can serve a purpose.

The likelihood of low interest rates for the foreseeable future requires investors to adjust their strategies as well as their expectations for current income. Considering a range of possible approaches should be an integral part of this process.

* May only be available for qualified purchasers or accredited investors.

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

IRR is the aggregate, compound annual internal rate of return on an investment based on partnership inflows and outflows and the estimated value of unreaslized investments at a specific date. Net IRR accounts for management fees and other fees, including expenses and carried interest, owed to the partnership manager.