Some Wal-Mart stores sell rifles, some Starbucks coffee shops sell alcohol, and GE builds engines for jet fighters and bombers. Some investors feel strongly about these and other issues, to the extent that they choose to screen out companies that do not agree with their values or societal priorities.

We help many of our clients align their portfolios with their values, and screening is one of the tools we employ to accomplish that alignment. Screening helps investors avoid supporting companies that they believe have an adverse impact on society or the environment, and it helps them gain a richer understanding of what they own in their portfolio. Indeed, many fiduciaries and charities feel a duty to use screening to identify and track any potentially controversial companies.

But while the concept of screening is rather simple—either you own a security or you do not—it can be a more complex matter to implement a screening program. For example, the companies mentioned above earn a very small fraction of their revenues from the products mentioned. Should an investor set a zero-tolerance policy for owning any company active in arenas they find objectionable? Or is a de minimis amount of revenue from these activities acceptable, in the interest of expanding the investor’s options? Screening can also impact returns over time; the California Public Employees’ Retirement System stated recently that it missed out on as much as $3 billion in gains between 2001 and 2014 as it gradually divested its tobacco holdings. How does one weigh potential losses today vs. long-term views about an industry’s viability or its impact on society?

We believe it is essential for investors to clarify the precise objectives of their screening efforts. Before even beginning to vet companies, investors should recognize the strengths and weaknesses of the data and methods available for screening, and make an informed choice about how to proceed in a way that makes sense for their needs.

Where There's Smoke...

For many years, negative or exclusionary screening was the most widely used sustainable investing strategy but was surpassed in 2016 by environmental, social and governance (ESG) integration (a strategy in which managers consider ESG risks and opportunities as part of their overall analysis of a security). Negative screening is still quite common—the US SIF Foundation reported at least $927 billion in identifiable assets being managed under such screens in 2016.

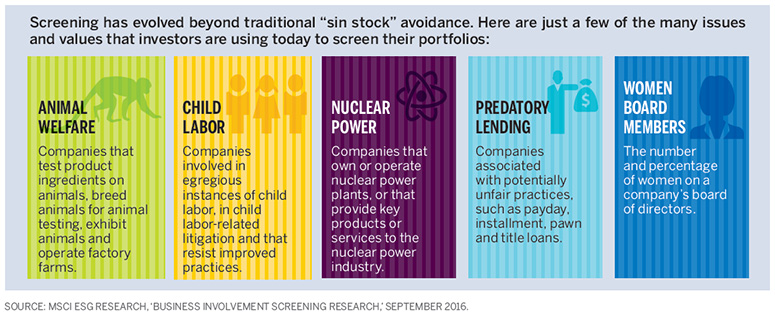

Of course, investors do not all share the same values, and screens are used to exclude a wide variety of businesses, activities and behaviors from their portfolios. We list a short selection of screens below that some of our clients have requested in recent years, but this is just a sample.

The most common criterion used to exclude a company from a portfolio is the amount of revenue that company generates from a particular line of business. A cut-and-dried approach of zero tolerance is the simplest application of this method, but screening becomes more complex when investors are open to some percentage of revenue up to a predetermined threshold or begin to consider the business activities through a company’s supply chain.

For example, investors opposed to owning tobacco stocks can easily determine whether they own, directly or through mutual funds, firms like Altria or British American Tobacco. They might not think to exclude a company like Core-Mark Holdings, which distributes merchandise to convenience stores in the U.S., and earns the majority of its revenue distributing cigarettes and other tobacco products, according to ESG data provider MSCI. The choice to exclude such a firm, which distributes but does not manufacture tobacco, may not be as clear-cut.

The same holds true with fossil fuel considerations. Investors can easily screen out oil, coal and other companies in the energy sector. But chemical companies that own fossil fuel reserves, for example, may not be caught by a standard fossil fuel screen, and investors may have different preferences about establishing broader or more narrow definitions of what qualifies as a fossil fuel stock.

Investors also use “off-balance sheet” criteria, such as the existence of outstanding litigation or a threshold for diversity on a company’s board of directors, to exclude companies from their portfolios. In recent years, more investors have begun to screen out companies based on their level of carbon emissions, in an effort to steer their capital toward more climate-friendly businesses. Emissions-oriented screening is one example of many where it is extremely important to understand the quality of available data because one’s desire to screen on a particular factor may be thwarted by the simple fact that the data is suspect. With regard to carbon data, investors should be aware that as of July 2016, only 53 companies worldwide were publicly disclosing data on 100% of their carbon emissions, according to Bloomberg. Many others report carbon emissions but only on a partial basis, and there is no regulatory standard to ensure that reported data from company to company is comparable or even accurate. In many cases, emissions are roughly estimated by third parties, with those estimates sometimes based on little more than a company’s industry and size. Such measures do not reflect the fact that companies within the same peer group can have very different emissions profiles based on business mix, past investment in efficiency technologies and many other factors.

High Stakes

Faith-based investors have been practicing portfolio screening for centuries, and the existential issues such investors consider demonstrate just how hard it can be to translate universal beliefs into specific portfolio critiera.

For example, many faith-based investors seek to screen out investments that infringe on their views about the sanctity of life. The filtering of companies involved in stem cell research and human cloning illustrates the nuance and ethical stakes that can come into play when building one’s portfolio. The United States Conference of Catholic Bishops (USCCB) does not condone investment in companies engaged in human cloning and stem cell research in ways that “violate the dignity of a developing person,” while stating that new forms of research “will be evaluated on a case-by-case basis.”

Some screening methods can be precise enough to capture the nuance and intent of this specific principle of the USCCB guidelines by excluding the use of stem cells from embryonic or fetal tissue but allowing investment in companies engaged in research using adult stem cells. MSCI and other data providers can help clients implement such a screen, while also screening out businesses that produce technology that could be used in research involving human embryonic stem cells, fetal tissue or fetal cell lines. To date, MSCI has not identified any publicly traded companies engaged in human cloning. That specific issue may not be a factor for investors today, but for some, it is not far-fetched to imagine human cloning technology within our lifetimes and the need to factor the ethics of such technology in one’s investments.

Knowledge is Power

Screening is typically used to take action in portfolios, but we find that our clients often value having increased knowledge about the companies they own, even if they have no definitive plan to act on that knowledge.

Such knowledge can be particularly valuable for charities and foundations that want to ensure their holdings do not conflict with their mission. One family that we advise asked us to help them analyze their foundation’s holdings through a mission-based lens. We discovered from a screening exercise that 3.1% of the foundation’s portfolio was associated with fossil fuels, weapons, tobacco and stem cell research—all of which contradicted the foundation’s objectives. The family determined that the small percentage did not warrant immediate action but greatly appreciated the deeper understanding of their holdings.

Screening is one of several tools investors can use to align their portfolios with their beliefs, but screens are only as helpful as the data and thinking used to develop them. Once they are properly empowered by knowledge, investors can confidently push forward with a customized, long-term plan to screen their investments and direct their capital in an optimal manner.

The views expressed are those of the authors and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. In addition, these views may not be relied upon as investment advice. The information provided in this material should not be considered a recommendation to buy or sell any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients or other clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients and is for informational purposes only. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication.

Bloomberg is a trademark of Bloomberg Finance L.P.